Emerging Europe Macro Daily(Beta Mode)

Orban's Defeat Boosts Hungary Sentiment

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| BIST 100 | 14,073.80 | +2.81% |

| iShares Poland | 39.29 | +0.54% |

| EUR/PLN | 4.25 | +0.24% |

| EUR/HUF | 367.38 | -2.14% |

| EUR/CZK | 24.36 | +0.02% |

| USD/TRY | 44.70 | +0.13% |

| Brent Crude | 102.27 | +7.43% |

| Gold | 4,741.30 | -0.43% |

| Bitcoin | 70,747.37 | -3.16% |

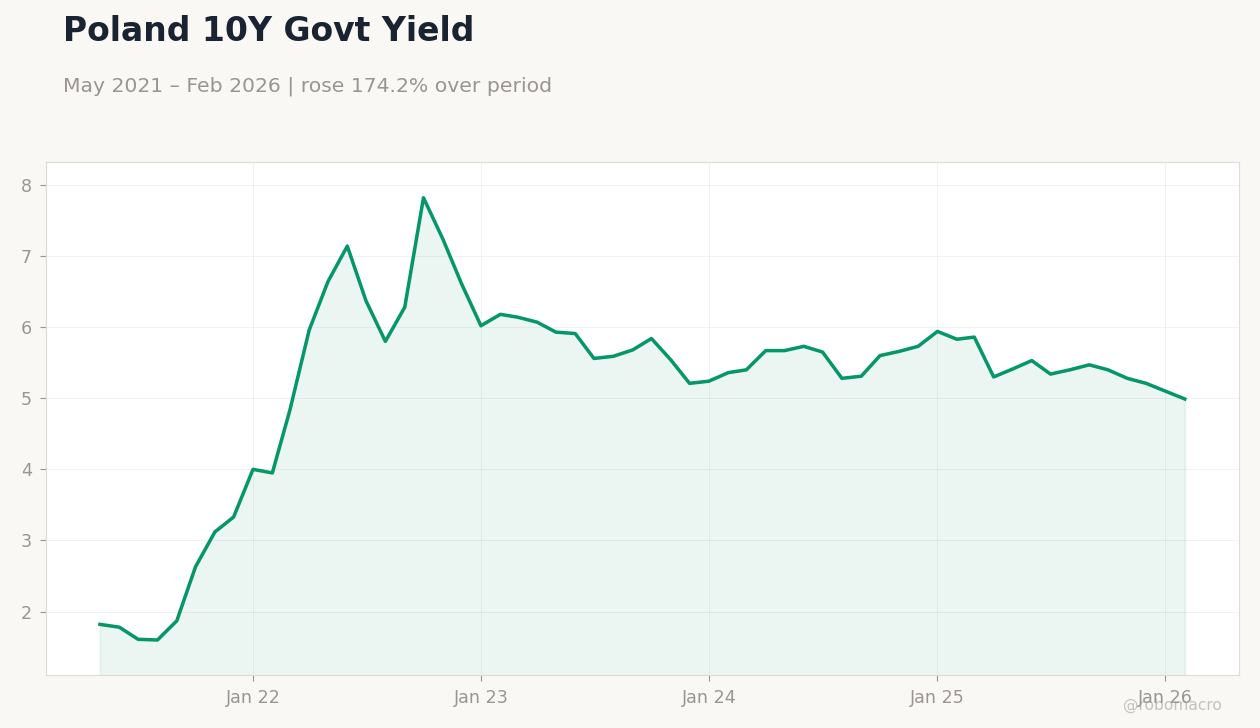

| Poland 10Y Govt Yield | 4.99% | -2.16% |

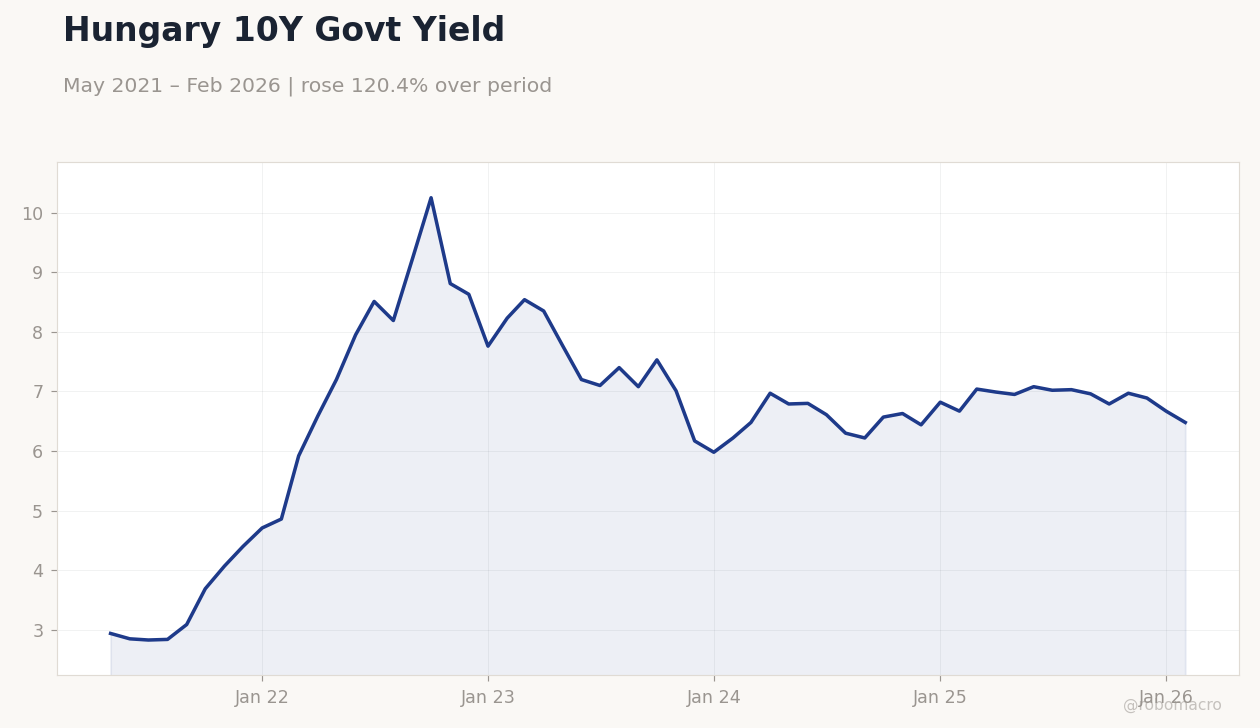

| Hungary 10Y Govt Yield | 6.48% | -2.85% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Hungary 10Y Govt Yield | Type: macro_line | Yield %: 6.48 (2026-02-01) | Range: 2.83–10.25 | Trend(6pt): 2.94,8.51,7.08,6.63,6.67,6.48

Hungary 10Y Govt Yield | Type: macro_line | Yield %: 6.48 (2026-02-01) | Range: 2.83–10.25 | Trend(6pt): 2.94,8.51,7.08,6.63,6.67,6.48

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Opposition win ends Orban's 16-year rule in Hungary, lifting assets on EU fund hopes and policy shifts.

- Poland highlights strong EU-era growth, outpacing Hungary, though Santander cuts 2026 GDP forecast to 3.8%.

- Oil surge drives Turkish equity gains, while CEE currencies and bonds show mixed risk dynamics.

Yesterday's Recap

Emerging European markets displayed mixed but mostly upbeat performance amid oil price jumps and Hungary's political change. The EUR/HUF fell 2.14% to 367.38, signaling better sentiment from the opposition victory potentially unlocking EU funds. Turkey's BIST 100 climbed 2.81% to 14,073.80, fueled by Brent crude's 7.43% increase to 102.27, supporting energy sectors despite USD/TRY rising 0.13% to 44.70.

Poland's iShares Poland rose 0.54% to 39.29, backed by reports of GDP nearly 3.6 times higher since 2004 EU accession, with the 10Y yield dropping 2.16% to 4.99%. Hungary's 10Y yield declined 2.85% to 6.48%, reflecting lower risk premiums after Orban's defeat. Czech assets stayed steady, with EUR/CZK up 0.02% to 24.36.

EUR/PLN edged 0.24% higher to 4.25. Gold dipped 0.43% to 4,741.30, while Bitcoin fell 3.16% to 70,747.37. No key macro data emerged, but NBP countered disinformation on gold, noting 169 billion zł in paper profits.

The Day Ahead

No major economic releases are slated for Emerging Europe tomorrow, shifting attention to Hungary's post-election fallout, including possible Tisza party cabinet updates from Péter Magyar. Markets may react to EU feedback on the vote, which could speed up frozen fund disbursements over rule-of-law issues. Turkey's assets could sway with oil market swings affecting inflation views.

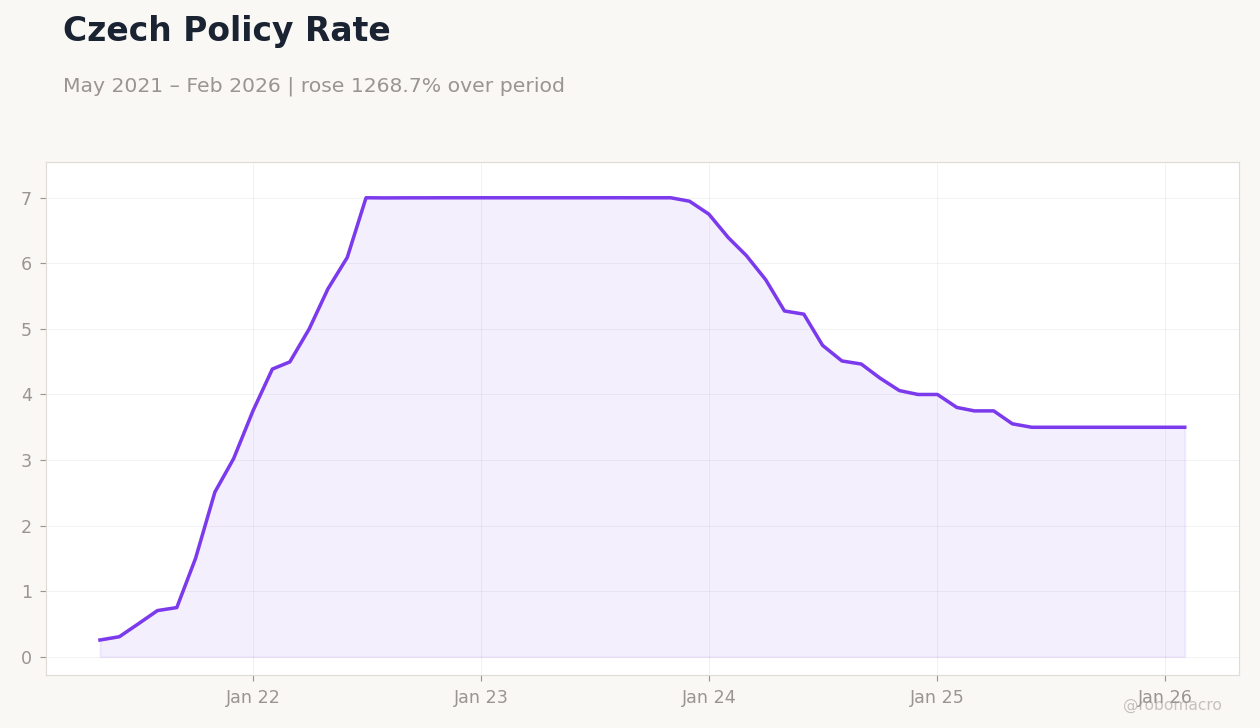

CEE trends may follow ECB cues, influencing CNB and MNB stances. Poland and Romania likely face subdued trading without fresh drivers, though NBP's gold clarifications might aid zloty steadiness.

Other Economic Notes

Poland's post-EU accession success underscores regional edge, with GDP expanding nearly 3.6 times since 2004 versus Hungary's slower pace, thanks to EU inflows and exports. Central and Eastern Europe's commercial real estate saw 11.8 billion euros in deals last year, with Poland leading amid investment surges. Santander trimmed its 2026 Polish GDP outlook to 3.8% from 3.9%, citing softer global demand, yet this highlights relative strength against Hungary's budget strains.

Morocco and Poland discussed migration and security ties, potentially boosting bilateral economic links. MNB reserves dipped slightly in March from February highs, per fresh data.