Yesterday's Recap

Emerging European markets displayed resilience amid global volatility, with Hungary's forint strengthening sharply as EUR/HUF fell 0.95% to 362.78 following Orban's defeat, signaling optimism for policy changes and EU fund inflows. Poland's iShares ETF rose 1.43% to 39.85, bolstered by news of expanded defense cooperation with South Korea and potential ESA center plans, while Poland's 10Y government yield dropped 2.16% to 4.99%, indicating safe-haven demand in the largest CEE economy. Turkey's BIST 100 index slipped 0.11% to 14,058.50, weighed by a slight 0.03% rise in USD/TRY to 44.71 amid persistent inflation worries, though no key data emerged.

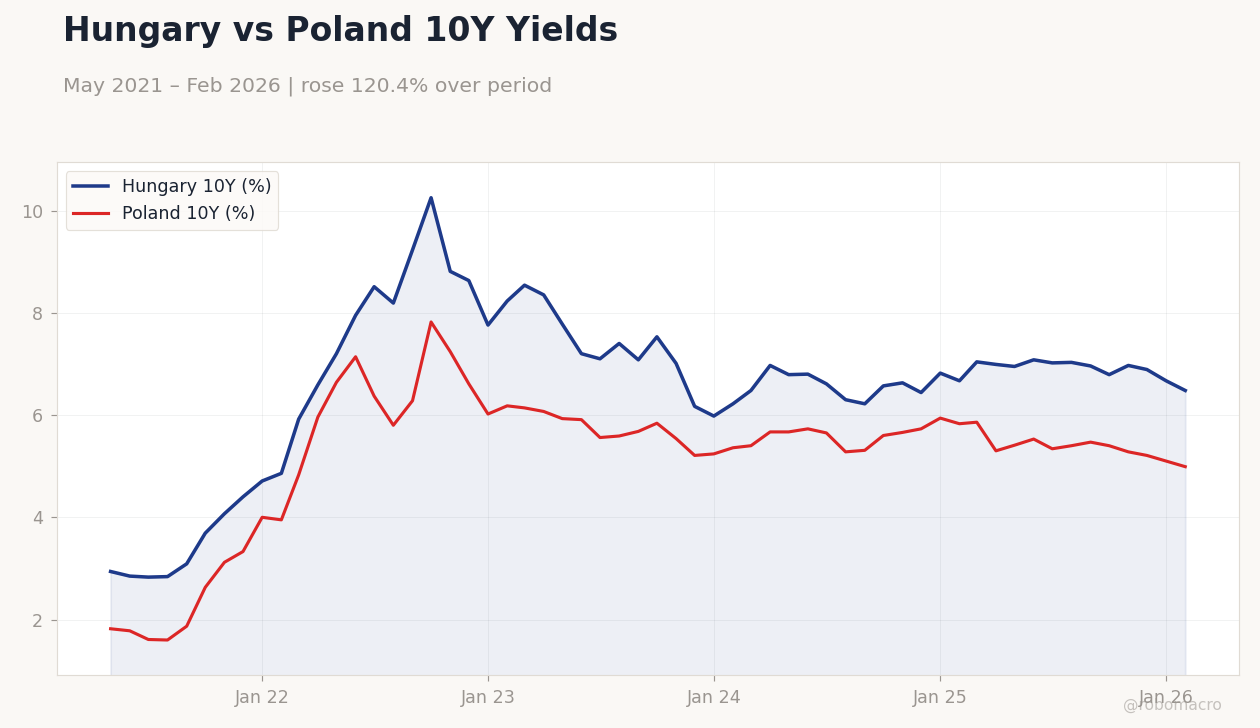

In the Czech Republic, import and export prices declined in February due to crown appreciation, with EUR/CZK edging up 0.01% to 24.36, highlighting vulnerabilities to energy and commodity swings. Hungarian 10Y yields fell 2.85% to 6.48%, consistent with the forint's surge and lower political risk premiums. Broader regional assets gained support from gold's 0.88% advance to 4,783.90, countering Brent crude's 0.84% decline to 98.53.

Bitcoin climbed 5.04% to 74,319.79, adding to mixed equity moves. Overall, Hungary's political developments overshadowed Turkey's macro pressures.

The Day Ahead

No major data releases are scheduled for today or tomorrow across Emerging Europe, providing space to assess Hungary's election fallout and EU ties. Turkey's Business Confidence Index is due on April 21 at 03:00 ET, with medium impact; previous reading was 101, consensus unavailable, but a drop could reflect weakening sentiment from inflation and geopolitics. IMF and World Bank spring meetings continue in Washington through April 18, discussing war impacts, with Turkey's Finance Minister Mehmet Şimşek attending, potentially shaping regional funding.

Poland's ESA center decision, slated by end-May, remains key for investments. Markets will watch forint movements as Péter Magyar details his agenda, alongside any ECB hints influencing CNB and MNB policies.

Hungary vs Poland 10Y Yields | Type: macro_line | Hungary 10Y (%): 6.48 (2026-02-01) | Range: 2.83–10.25 | Trend(6pt): 2.94,8.51,7.08,6.63,6.67,6.48 | Poland 10Y (%): 4.99 (2026-02-01) | Range: 1.6–7.82 | Trend(6pt): 1.82,6.37,5.68,5.66,5.1,4.99

Hungary vs Poland 10Y Yields | Type: macro_line | Hungary 10Y (%): 6.48 (2026-02-01) | Range: 2.83–10.25 | Trend(6pt): 2.94,8.51,7.08,6.63,6.67,6.48 | Poland 10Y (%): 4.99 (2026-02-01) | Range: 1.6–7.82 | Trend(6pt): 1.82,6.37,5.68,5.66,5.1,4.99