Emerging Europe Macro Daily(Beta Mode)

Zloty Gains, Hungary Eyes Euro Path

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| BIST 100 | 14,202.20 | +1.02% |

| iShares Poland | 40.24 | +0.98% |

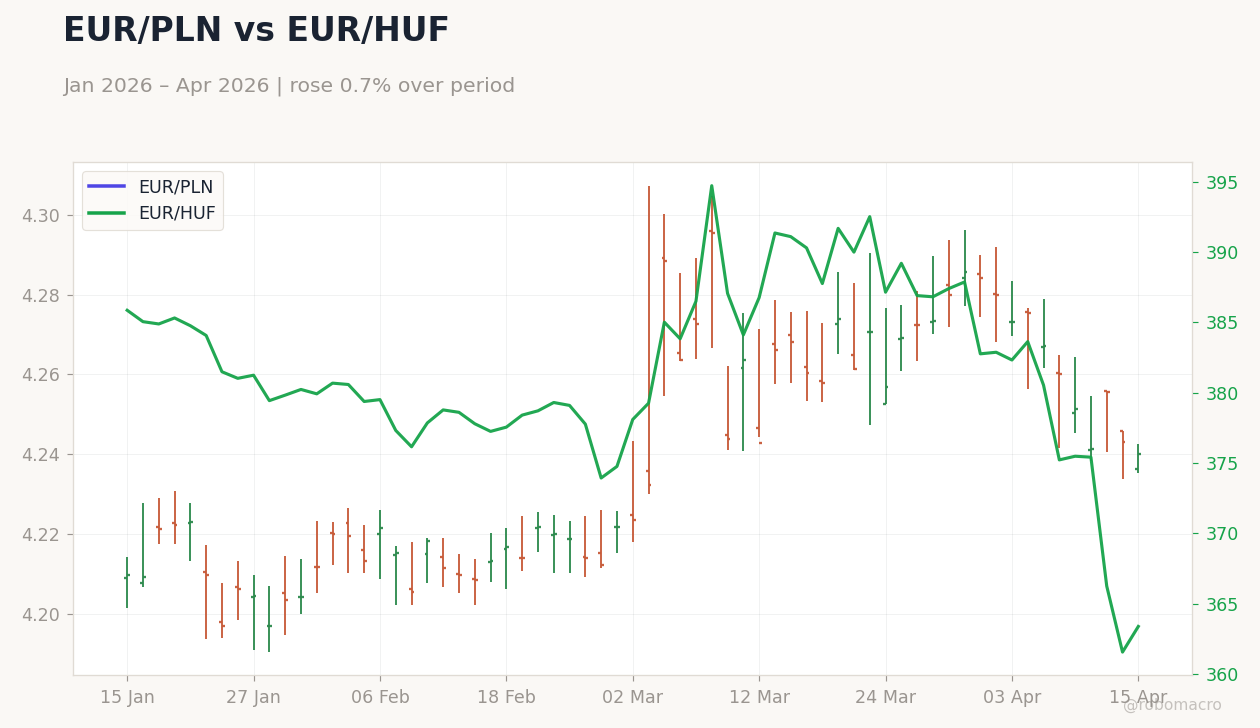

| EUR/PLN | 4.24 | -0.07% |

| EUR/HUF | 363.41 | +0.51% |

| EUR/CZK | 24.33 | -0.06% |

| USD/TRY | 44.74 | +0.07% |

| Brent Crude | 95.68 | +0.94% |

| Gold | 4,849.80 | +0.51% |

| Bitcoin | 74,005.50 | -0.64% |

| Poland 10Y Govt Yield | 4.99% | -2.16% |

| Hungary 10Y Govt Yield | 6.48% | -2.85% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Poland 10Y Govt Yield | Type: macro_line | 10Y Yield (%): 4.99 (2026-02-01) | Range: 1.6–7.82 | Trend(6pt): 1.82,6.37,5.68,5.66,5.1,4.99

Poland 10Y Govt Yield | Type: macro_line | 10Y Yield (%): 4.99 (2026-02-01) | Range: 1.6–7.82 | Trend(6pt): 1.82,6.37,5.68,5.66,5.1,4.99

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Business Confidence Index | 101 | - | 03:00 |

| Consumer Confidence Index | 85 | - | 03:00 |

| TCMB Interest Rate Decision | 37 | - | 07:00 |

- Polish zloty strengthens to multi-week lows versus euro on positive IMF growth outlook, lifting regional sentiment.

- Hungary's post-Orbán pivot signals EU reengagement and potential euro convergence, boosting forint and bonds.

- Turkey awaits CBRT rate decision amid sticky inflation, with confidence indices due next week.

Yesterday's Recap

Emerging Europe markets displayed resilience yesterday, with Turkey's BIST 100 index rising 1.02% to 14,202.20, fueled by optimism before the upcoming CBRT meeting despite lira strains. Poland's iShares ETF advanced 0.98% to 40.24, aided by zloty firmness as EUR/PLN fell 0.07% to 4.24, its lowest since early March per Bankier.pl, aligned with IMF projections of 3.3% GDP growth for 2026. Hungary's EUR/HUF rose 0.51% to 363.41, indicating forint softening, but the 10Y government yield dropped 2.85% to 6.48%, betting on incoming Prime Minister Péter Magyar's EU thaw per Intellinews.

Czech EUR/CZK declined 0.06% to 24.33 amid quiet data, while no key Romanian releases occurred, though zloty spillover supported sentiment. Bond rallies persisted, with Poland's 10Y yield falling 2.16% to 4.99%. Turkey's USD/TRY edged up 0.07% to 44.74, vulnerable to energy imports.

No major macro data released regionally, shifting attention to Hungary's political shifts and Poland's EU fund progress.

The Day Ahead

No events are scheduled for today or tomorrow per the calendar, with focus turning to next week's Turkey data. Upcoming releases include the Business Confidence Index on April 21 at 03:00 ET, following a previous 101 reading to gauge manufacturing mood. The Consumer Confidence Index follows on April 22 at 03:00 ET, assessing household sentiment after last month's 85 print amid elevated inflation.

The key CBRT interest rate decision arrives on April 22 at 07:00 ET, with the prior rate at 37% and no consensus, potentially holding steady given price pressures. Poland, Czech Republic, Hungary, and Romania have no slated events, directing eyes to global ECB cues and Hungary's cabinet developments under Magyar, which may influence forint moves.

Other Economic Notes

IMF forecasts highlight Poland's steady path with 3.3% GDP growth in 2026 slowing to 2.4% in 2027, supported by EU funds but constrained by energy shocks per Bankier.pl. Hungary's Russian energy links cap post-Orbán changes, as Magyar plans to maintain oil and gas imports for now despite EU aims, per Intellinews. Migratory flows from Belarus have shifted to Latvia and Lithuania, with Poland achieving 100% border effectiveness per Bankier.pl, aiding stability.

(cont...)