Emerging Europe Macro Daily(Beta Mode)

Forint Rallies on Tisza Win

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| BIST 100 | 14,587.90 | +2.72% |

| iShares Poland | 40.64 | +1.78% |

| EUR/PLN | 4.24 | +0.12% |

| EUR/HUF | 362.00 | -0.64% |

| EUR/CZK | 24.28 | -0.14% |

| USD/TRY | 44.85 | +0.27% |

| Brent Crude | 90.38 | -9.07% |

| Gold | 4,857.60 | +1.51% |

| Bitcoin | 74,231.87 | -1.97% |

| Poland 10Y Govt Yield | 5.58% | +11.82% |

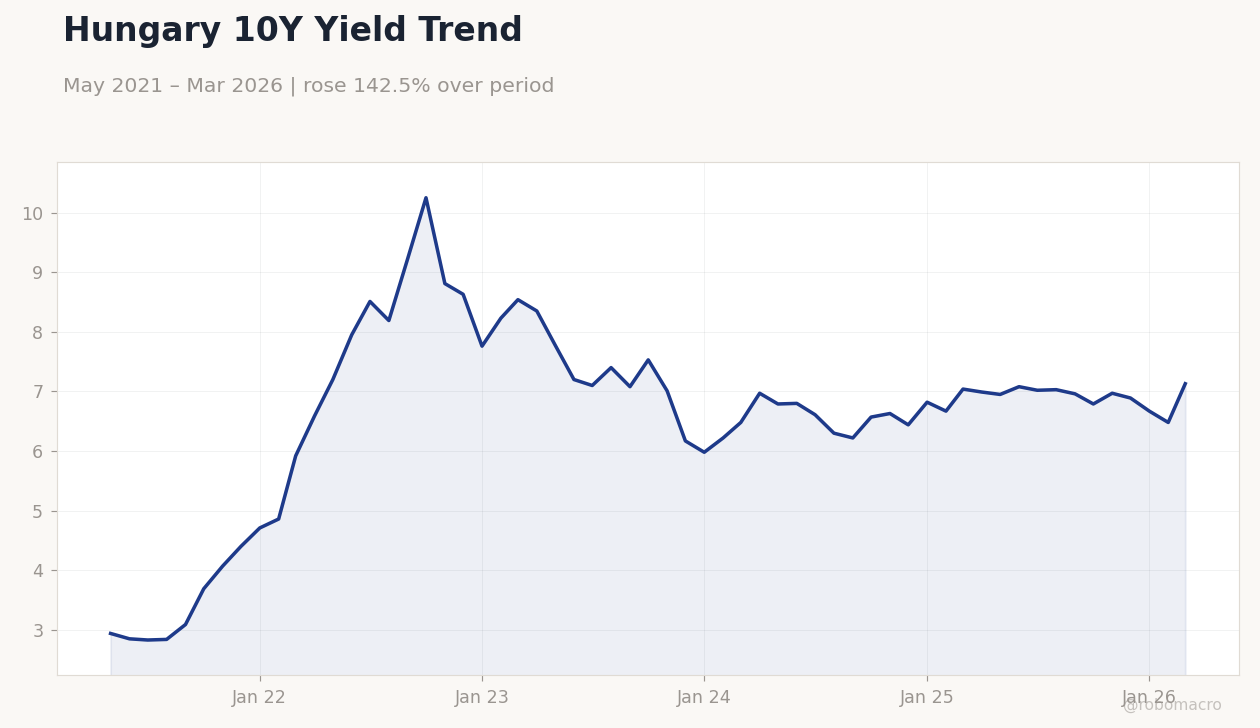

| Hungary 10Y Govt Yield | 7.13% | +10.03% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Hungary 10Y Yield Trend | Type: macro_line | Hungary 10Y Yield: 7.13 (2026-03-01) | Range: 2.83–10.25 | Trend(6pt): 2.94,8.51,7.08,6.63,6.67,7.13

Hungary 10Y Yield Trend | Type: macro_line | Hungary 10Y Yield: 7.13 (2026-03-01) | Range: 2.83–10.25 | Trend(6pt): 2.94,8.51,7.08,6.63,6.67,7.13

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Business Confidence Index | 101 | - | 23:00 |

| Consumer Confidence Index | 85 | - | 23:00 |

| TCMB Interest Rate Decision | 37 | - | 03:00 |

| Headline Unemployment Rate | 6.10 | 6.10 | 23:30 |

- Hungarian forint surges on Tisza party's election victory and euro adoption hints.

- Polish assets gain amid G20 participation and regional trade boosts.

- Turkish markets rise despite lira pressures, CBRT decision ahead.

Yesterday's Recap

Emerging European markets displayed strength despite global headwinds, with Turkey's BIST 100 index climbing 2.72% to 14,587.90, fueled by hopes for policy continuity amid inflation challenges. Hungary's EUR/HUF fell 0.64% to 362.00, driven by the forint's rally after the Tisza party's landslide win and signals of faster euro integration. Poland's iShares ETF advanced 1.78% to 40.64, bolstered by sentiment from NBP's G20 presence and news of arms exports from Norway plus Uzbekistan trade expansion, though EUR/PLN rose 0.12% to 4.24 showing slight zloty weakness.

Czech markets held steady, with EUR/CZK down 0.14% to 24.28 on balanced fundamentals. Bond markets saw yields climb, Poland's 10Y at 5.58% with a 11.82% change and Hungary's at 7.13% up 10.03%, reflecting fiscal caution. Turkey's USD/TRY increased 0.27% to 44.85, underscoring lira fragility.

No significant economic data was released yesterday, but headlines emphasized Poland's global financial role and zloty sensitivity to Middle East developments.

The Day Ahead

Attention turns to Turkey with the Business Confidence Index at 23:00 ET today, previous at 101, gauging business sentiment in a high-inflation environment. The Consumer Confidence Index follows at 23:00 ET tomorrow, prior reading 85, shedding light on consumer resilience. TCMB's interest rate decision arrives April 22 at 03:00 ET, with the rate at 37% under review amid persistent price rises.

Poland's headline unemployment rate is set for April 23 at 23:30 ET, consensus 6.1% matching previous, reinforcing labor market strength. Regional FX may react to Hungary's political shifts, while no key events are scheduled for Czech Republic or Romania, maintaining focus on Turkish data.

Other Economic Notes

Emerging Europe faces ongoing energy vulnerabilities, with Brent crude's 9.07% drop to 90.38 highlighting Middle East tensions' impact on importers like Poland and Hungary, who are diversifying through arms deals and trade pacts with Uzbekistan. Inflation trends vary: Turkey contends with elevated levels, contrasting CEE's cooling, aiding Poland's euro convergence. EU funds are vital for Hungary's new government to address fiscal gaps and support recovery.

Zloty stability persists near six-week lows, awaiting Middle East updates, while forint strength tests sustainability post-Tisza victory.