Emerging Europe Macro Daily(Beta Mode)

Poland Booms Amid Deficit Woes

Market Snapshot

| Asset | Level | Change |

|---|---|---|

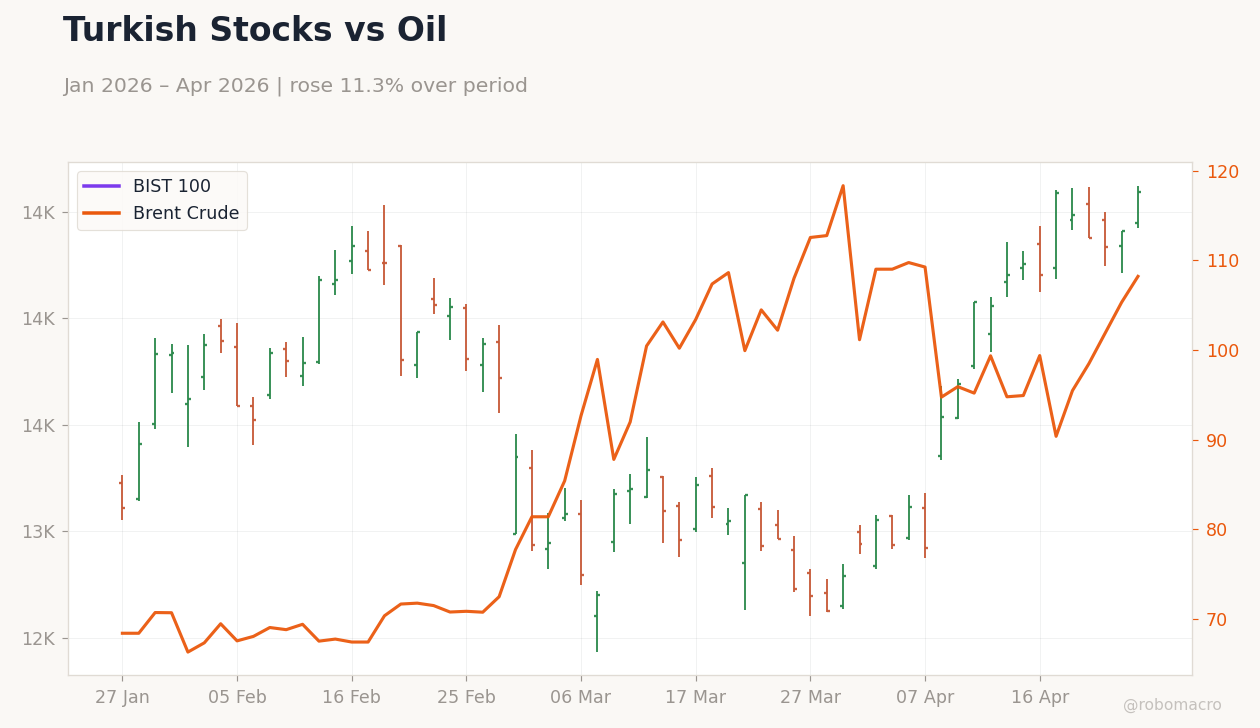

| BIST 100 | 14,594.00 | +1.28% |

| iShares Poland | 38.50 | -1.13% |

| EUR/PLN | 4.25 | +0.21% |

| EUR/HUF | 364.23 | -0.21% |

| EUR/CZK | 24.35 | +0.04% |

| USD/TRY | 45.03 | +0.04% |

| Brent Crude | 103.25 | -4.60% |

| Gold | 4,663.10 | -0.26% |

| Bitcoin | 76,820.88 | -2.34% |

| Poland 10Y Govt Yield | 5.58% | +11.82% |

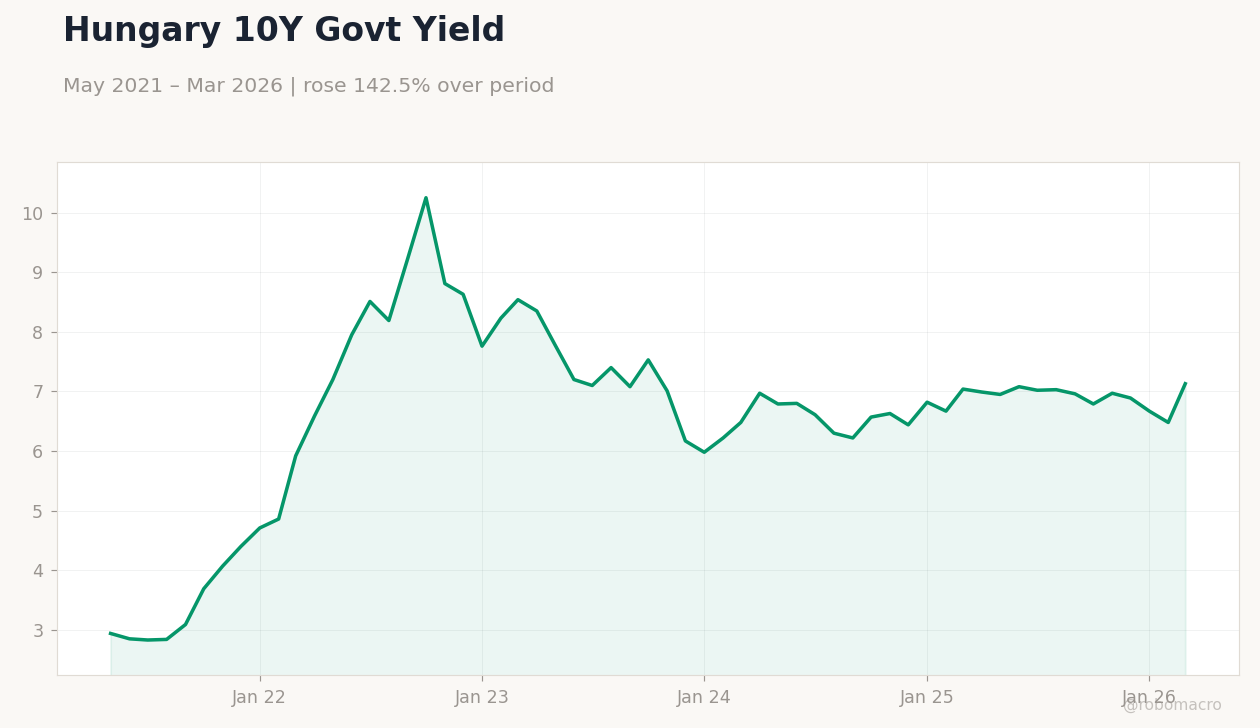

| Hungary 10Y Govt Yield | 7.13% | +10.03% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Poland vs Hungary Yields | Type: macro_line | Poland 10Y (%): 5.58 (2026-03-01) | Range: 1.6–7.82 | Trend(6pt): 1.82,6.37,5.68,5.66,5.1,5.58 | Hungary 10Y (%): 7.13 (2026-03-01) | Range: 2.83–10.25 | Trend(6pt): 2.94,8.51,7.08,6.63,6.67,7.13

Poland vs Hungary Yields | Type: macro_line | Poland 10Y (%): 5.58 (2026-03-01) | Range: 1.6–7.82 | Trend(6pt): 1.82,6.37,5.68,5.66,5.1,5.58 | Hungary 10Y (%): 7.13 (2026-03-01) | Range: 2.83–10.25 | Trend(6pt): 2.94,8.51,7.08,6.63,6.67,7.13

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Headline Unemployment Rate | 8.50 | - | 23:00 |

| Balance of Trade Final | -9,000m | - | 23:00 |

| Inflation Rate Year-over-Year Preliminary | 3 | - | 23:30 |

- Poland's economy thrives on Ukrainian labor and exports, but high deficits drive yield surges.

- Turkish stocks rally despite global commodity dips; CEE FX shows mixed moves.

- Stagflation fears and ECB stability shape regional macro outlook.

Yesterday's Recap

Emerging European markets showed mixed results amid global risk-off tones from commodity declines and regional headlines. Turkey's BIST 100 index rose 1.28% to 14,594.00, supported by domestic sentiment despite Brent crude's 4.60% fall to 103.25, highlighting energy import risks. In Poland, the iShares Poland ETF dropped 1.13% to 38.50, contrasting with positive news on economic growth driven by Ukrainian workers and Ukraine becoming Poland's 7th largest export partner.

Polish 10-year government yields jumped 11.82% to 5.58%, strained by reports of Poland's second-highest EU fiscal deficit at 7.3% of GDP in 2025, behind only Romania's 7.9%. Hungary's 10-year yields increased 10.03% to 7.13%, with EUR/HUF falling 0.21% to 364.23 on fiscal jitters, while EUR/PLN rose 0.21% to 4.25. Czech EUR/CZK inched up 0.04% to 24.35, indicating resilience, and USD/TRY edged higher by 0.04% to 45.03.

No significant data releases happened, but narratives emphasized Poland's expansion tempered by fiscal pressures and Turkey's resilience in a high-inflation setting.

The Day Ahead

Focus shifts to Turkey's headline unemployment rate at 23:00 ET, with previous at 8.5%, shedding light on labor strength amid ongoing inflation. Turkey's final balance of trade follows at 23:00 ET on April 29, prior at -9 billion, which may reveal export patterns in a softening global backdrop. Poland's preliminary year-over-year inflation rate arrives at 23:30 ET on April 29, previous at 3%, key for NBP decisions amid disinflation expectations.

These could sway FX like USD/TRY and EUR/PLN, particularly on surprises. Wider monitoring includes ECB spillover effects, given CEE ties, with potential bond volatility if data diverges from eurozone norms.

Other Economic Notes

Poland's growth, boosted by Ukrainian immigrants and exports to Ukraine, highlights regional ties but prompts concerns over long-term viability with elevated deficits. Turkey's distinct position continues, with energy reliance worsening trade balances, while CEE nations like Czech Republic and Hungary pursue EU funds for alignment. Themes also cover Russia's economic strains paralleling global slowdowns, which might reduce energy costs for reliant Poland and Hungary.

Romania's top EU deficit underscores hurdles to euro adoption, emphasizing fiscal discipline needs across the region.