Emerging Europe Macro Daily(Beta Mode)

Turkey Jobless Falls, Poland CPI Ticks Up

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| BIST 100 | 14,442.60 | +0.92% |

| iShares Poland | 38.38 | +1.13% |

| EUR/PLN | 4.26 | -0.05% |

| EUR/HUF | 364.05 | -0.28% |

| EUR/CZK | 24.36 | -0.03% |

| USD/TRY | 45.14 | -0.07% |

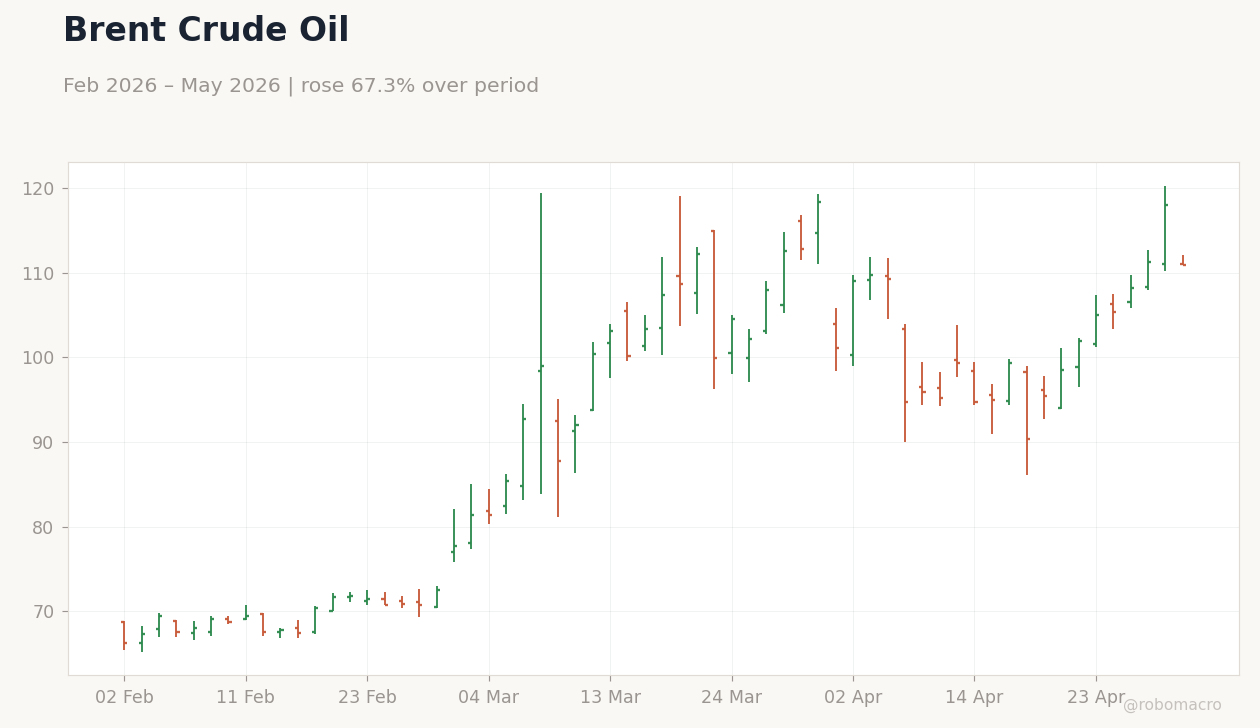

| Brent Crude | 111.04 | -5.92% |

| Gold | 4,620.20 | +0.12% |

| Bitcoin | 77,128.00 | +1.78% |

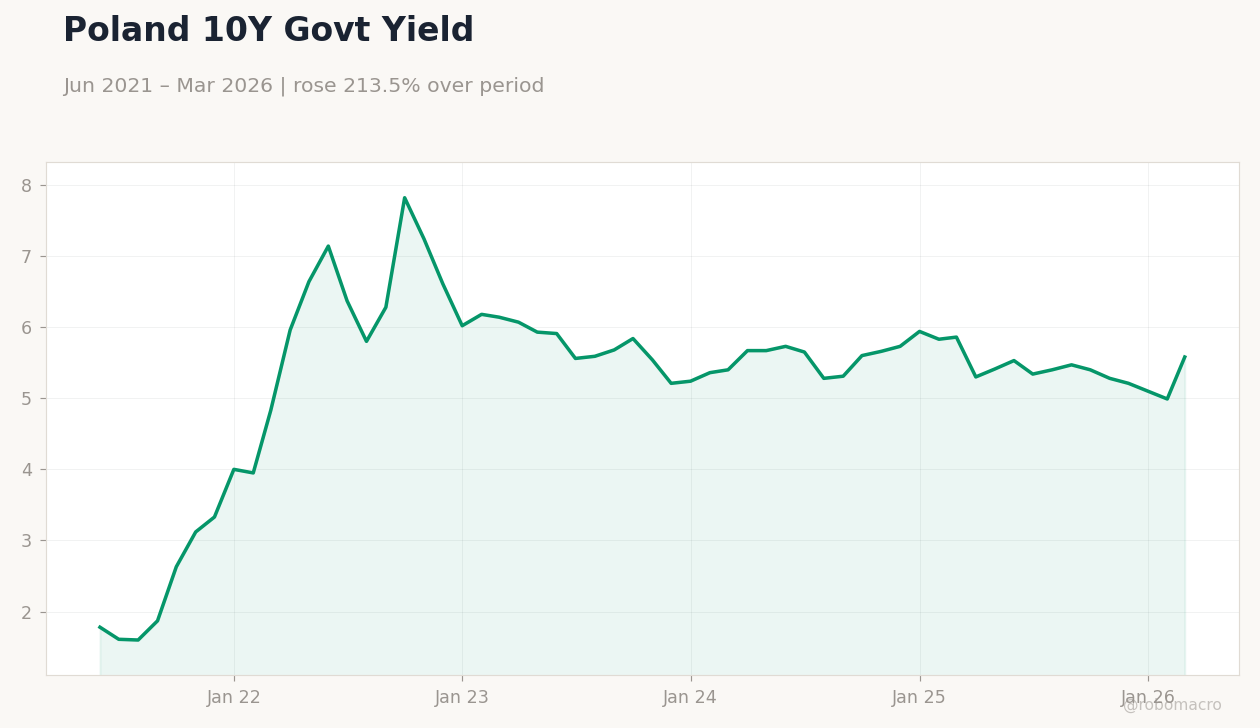

| Poland 10Y Govt Yield | 5.58% | +11.82% |

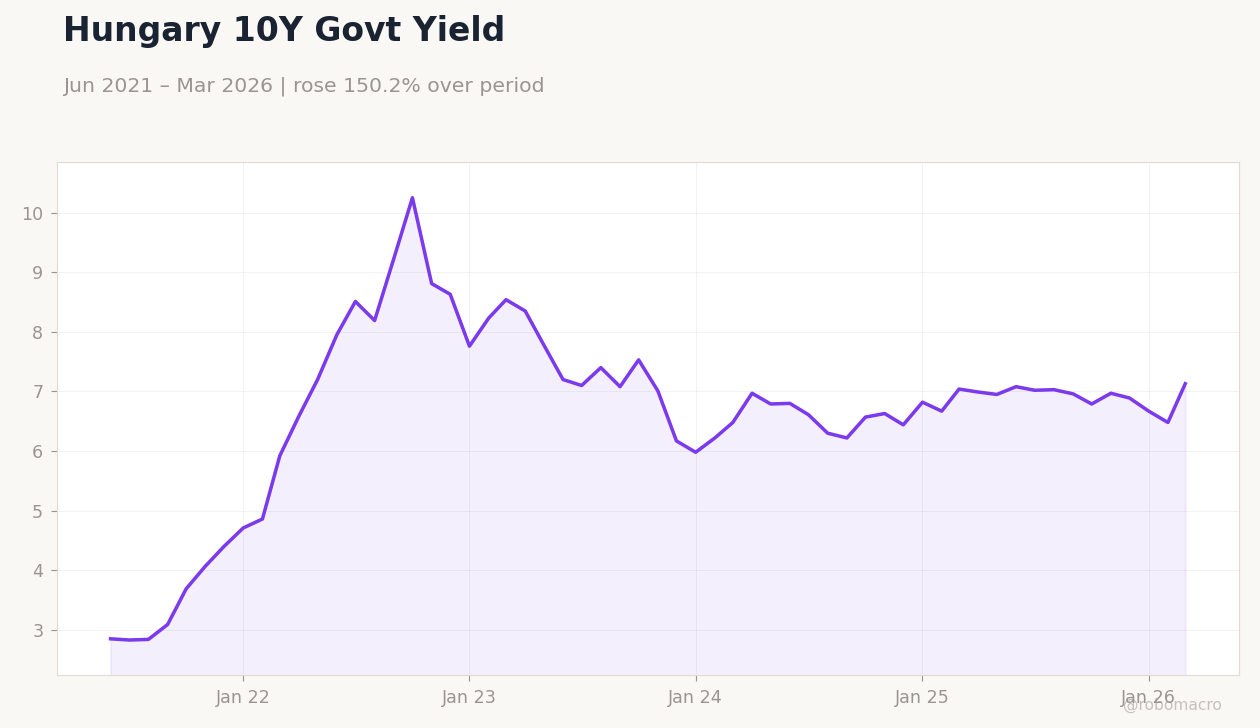

| Hungary 10Y Govt Yield | 7.13% | +10.03% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Headline Unemployment Rate | 8.50 | - | 8.10 |

| Balance of Trade Final | -9,000m | - | -11,200m |

| Inflation Rate Year-over-Year Preliminary | 3 | - | 3.20 |

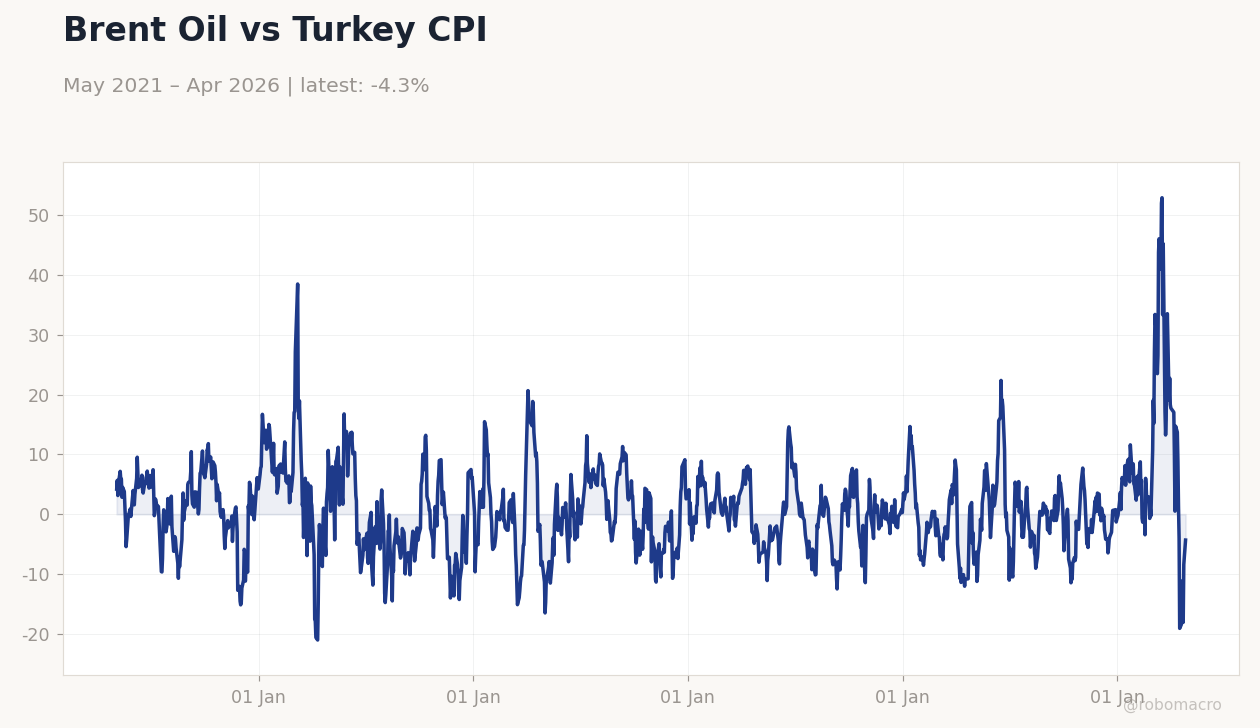

Brent Oil vs Turkey CPI | Type: macro_line | Brent $/bbl: -4.318 (2026-04-27) | Range: -21.02–52.89 | Trend(5pt): 4.204,4.05,2.636,-2.194,-4.318

Brent Oil vs Turkey CPI | Type: macro_line | Brent $/bbl: -4.318 (2026-04-27) | Range: -21.02–52.89 | Trend(5pt): 4.204,4.05,2.636,-2.194,-4.318

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Turkey's unemployment rate declined to 8.1% from 8.5%, while the trade deficit widened to -$11.2 billion from -$9 billion, highlighting mixed labor resilience and external pressures amid inflation.

- Poland's preliminary YoY inflation rose to 3.2% from 3%, influenced by oil prices, with EUR/PLN stable at 4.26 after a 0.05% dip.

- Regional equities advanced modestly, BIST 100 up 0.92% to 14,442.60 and iShares Poland up 1.13% to 38.38, but Poland and Hungary 10Y yields rose sharply to 5.58% (+11.82% change) and 7.13% (+10.03% change).

Yesterday's Recap

Emerging Europe featured key data on April 30, with Turkey's headline unemployment rate dropping to 8.1% from 8.5%, indicating job market strength despite challenges, though the final trade balance worsened to a -$11.2 billion deficit from -$9 billion, driven by energy imports. Poland's preliminary YoY inflation increased to 3.2% from 3%, spurred by oil price rises that briefly pushed the euro above 4.25 PLN, as per local reports. Equities performed well, with Turkey's BIST 100 rising 0.92% to 14,442.60 on banking gains, and iShares Poland climbing 1.13% to 38.38, supported by strong Q1 profits from Bank Pekao (over 1.2 billion PLN) and mBank (953 million PLN).

Hungarian markets softened, with EUR/HUF declining 0.28% to 364.05 amid Bank of America warnings of further forint weakness, and the 10Y yield increasing 10.03% to 7.13% linked to fiscal concerns and an MNB scandal involving misleading decisions for a Kecskemet university foundation. Czech assets remained stable, EUR/CZK down 0.03% to 24.36, bolstered by the acquisition of local cycling app Rouvy by U.S. firm Zwift, with no significant data.

Romania saw no releases, but CEE sentiment lifted from Polish banking results. Turkey's USD/TRY fell 0.07% to 45.14, though volatility persists under CBRT oversight.

The Day Ahead

May 1 offers a subdued calendar for Emerging Europe, with no data releases or events in Poland, Czech Republic, Hungary, Romania, or Turkey, providing time to absorb recent inflation and trade data. Markets may turn to global influences, including ECB signals, given the regional lull. Potential unscheduled developments, such as FX interventions in Hungary or Turkey, could arise amid volatility.

EU energy trends may affect import-heavy CEE economies. May 2 also lacks events, suggesting a consolidation period, especially with May 1 Labor Day holidays in many nations potentially thinning trading.

Other Economic Notes

Emerging Europe shows inflation contrasts, with Turkey facing elevated pressures versus CEE's easing trends, as Poland's 3.2% CPI reflects energy risks tied to EU links. EU funds are vital for fiscal stability in Poland and Hungary, where deficits improve but issues like the MNB scandal undermine trust. (cont...)