Emerging Europe Macro Daily(Beta Mode)

Turkey CPI Beats Forecasts, Yields Rise

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| BIST 100 | 14,369.60 | -0.51% |

| iShares Poland | 38.00 | -0.86% |

| EUR/PLN | 4.26 | +0.32% |

| EUR/HUF | 365.16 | +1.17% |

| EUR/CZK | 24.39 | +0.19% |

| USD/TRY | 45.21 | +0.06% |

| Brent Crude | 113.40 | -0.91% |

| Gold | 4,545.80 | +0.58% |

| Bitcoin | 80,893.45 | +3.00% |

| Poland 10Y Govt Yield | 5.58% | +11.82% |

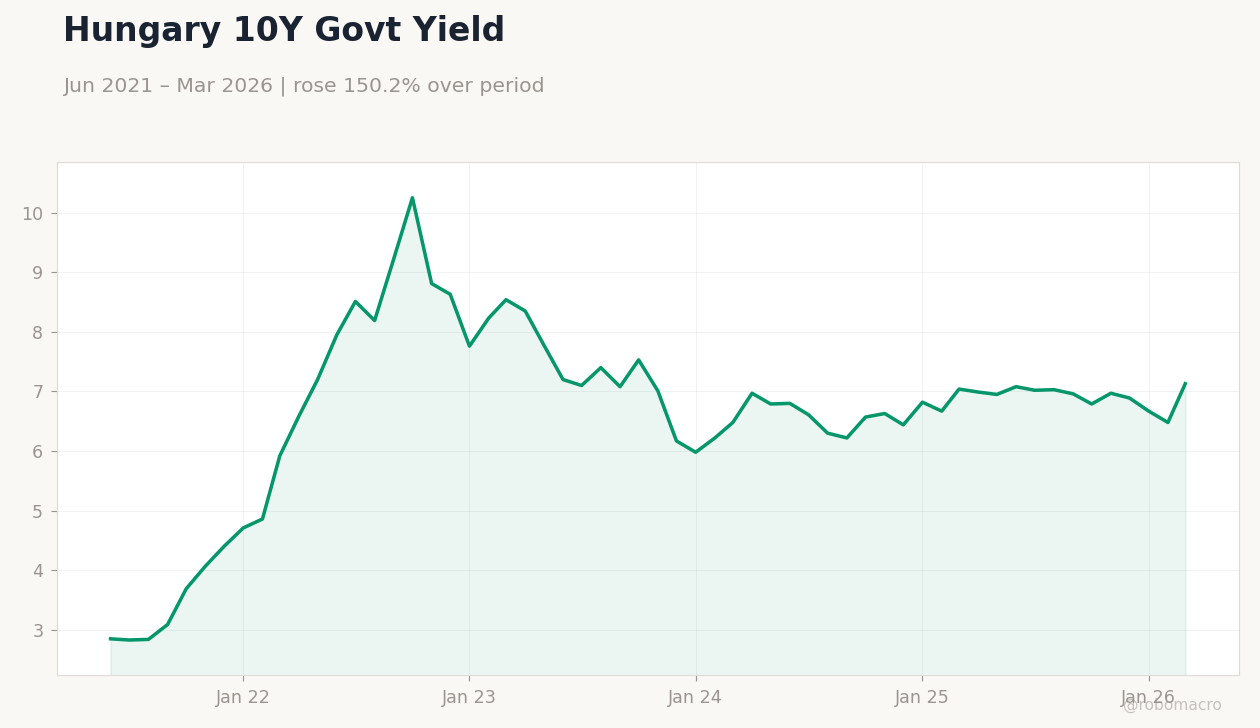

| Hungary 10Y Govt Yield | 7.13% | +10.03% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Inflation Rate Month-over-Month | 1.94 | 3.28 | 4.18 |

| Inflation Rate Year-over-Year | 30.87 | 31.25 | 32.37 |

Poland 10Y Govt Yield | Type: macro_line | Poland 10Y Yield %: 5.58 (2026-03-01) | Range: 1.6–7.82 | Trend(6pt): 1.78,5.8,5.84,5.73,4.99,5.58

Poland 10Y Govt Yield | Type: macro_line | Poland 10Y Yield %: 5.58 (2026-03-01) | Range: 1.6–7.82 | Trend(6pt): 1.78,5.8,5.84,5.73,4.99,5.58

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Central Bank Interest Rate Decision | 3.75 | 3.75 | 04:00 |

| Industrial Production Year-over-Year | 2.20 | - | 23:00 |

| Wednesday (2026-05-06) | |||

| Central Bank Interest Rate Decision | 3.75 | 3.75 | 04:00 |

- Turkey's April inflation rose to 4.18% MoM and 32.37% YoY, beating consensus and highlighting ongoing price pressures amid lira fluctuations.

- Polish exports jumped 7.4% MoM to €32.4bn in March, supported by favorable zloty-dollar exchange rates, as EUR/PLN eased to 4.26.

- Regional yields climbed, with Poland's 10Y at 5.58% (+11.82%) and Hungary's at 7.13% (+10.03%), amid global risk aversion.

Yesterday's Recap

Turkey's inflation release dominated, with April CPI up 4.18% MoM versus consensus 3.28% and prior 1.94%, while YoY hit 32.37% against expected 31.25%, underscoring CBRT challenges in curbing prices under fiscal strains and USD/TRY ticking up 0.06% to 45.21. In Poland, March exports reached €32.443bn, rising 7.4% MoM, fueled by competitive zloty rates and robust demand for autos and goods, though iShares Poland fell 0.86% to 38.00 amid wider EM caution. Hungary's EUR/HUF weakened 1.17% to 365.16, straining the forint as 10Y yields advanced to 7.13%, with regional equities facing pressures.

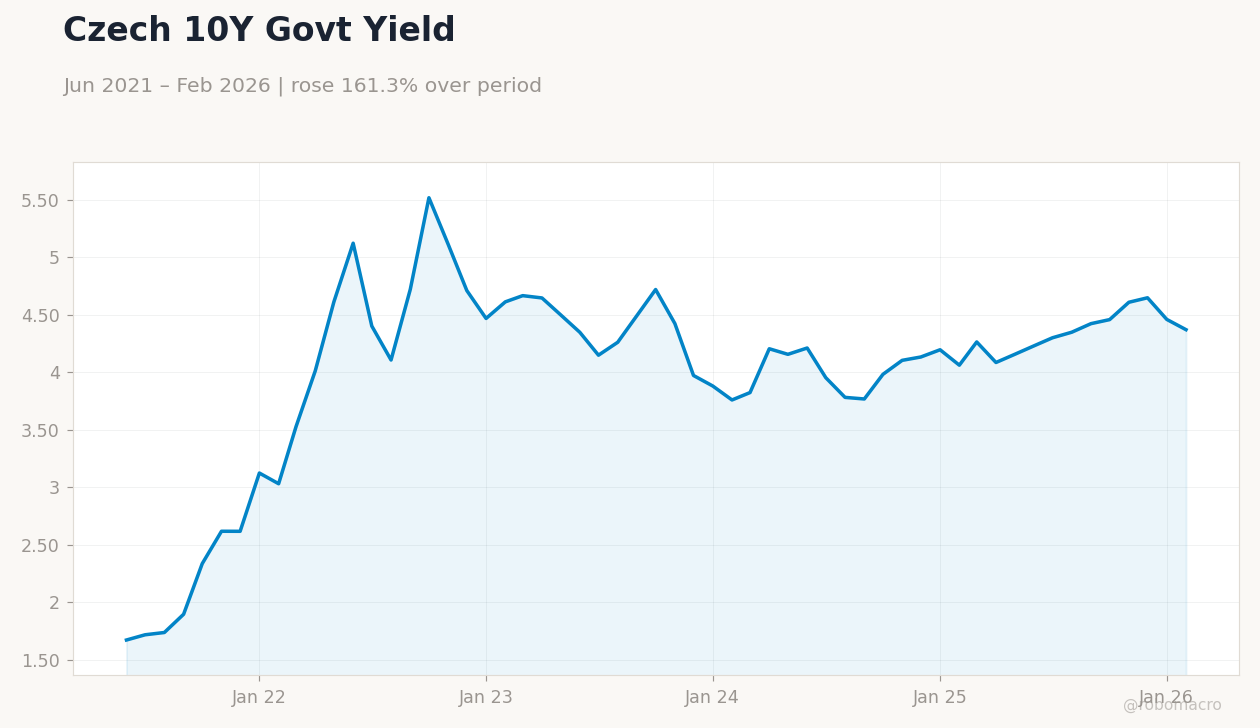

Czech markets had EUR/CZK up 0.19% to 24.39, with sparse data keeping attention on energy import vulnerabilities. Turkey's BIST 100 dropped 0.51% to 14,369.60, impacted by inflation surprises and Brent crude declining 0.91% to 113.40, worsening import expenses. Romania saw no key releases, but EU fund discussions indirectly bolstered sentiment.

Overall, Emerging Europe assets lagged, with gold rising 0.58% to 4,545.80 providing haven appeal.

The Day Ahead

Poland's NBP will announce its interest rate decision on May 6 at 04:00 ET, with consensus for a hold at 3.75% given easing inflation and strong exports. Turkey's March industrial production YoY is due on May 7 at 23:00 ET, lacking consensus but following prior 2.2%, potentially showing manufacturing strength. Focus may include NBP comments on FX moves, with recent zloty softening to 4.26 versus euro.

Broader attention turns to EU SAFE fund progress for Poland, as Prime Minister Tusk noted likely readiness for signing by Friday, possibly releasing billions in aid. No major data from Czech Republic, Hungary, or Romania, directing eyes to global signals like U.S. inflation developments.

Other Economic Notes

Emerging Europe's energy reliance poses risks, with Turkey and Poland grappling with elevated import costs as Brent crude stands at 113.40 despite a daily drop. Poland's export surge to €32.4bn underscores CEE durability via EU trade links, differing from Turkey's inflation isolation from euro paths. Fiscal enhancements, like potential SAFE funds for Poland, may reduce deficits and spur investment, while Hungary's rule-of-law issues hinder similar EU support.