Emerging Europe Macro Daily(Beta Mode)

Hungary PM Shift, CEE Yields Surge

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| BIST 100 | 15,062.70 | +0.15% |

| iShares Poland | 39.03 | -0.28% |

| EUR/PLN | 4.24 | +0.19% |

| EUR/HUF | 355.00 | -0.26% |

| EUR/CZK | 24.31 | +0.08% |

| USD/TRY | 45.38 | +0.33% |

| Brent Crude | 105.81 | +4.46% |

| Gold | 4,683.30 | -0.79% |

| Bitcoin | 80,846.73 | +0.23% |

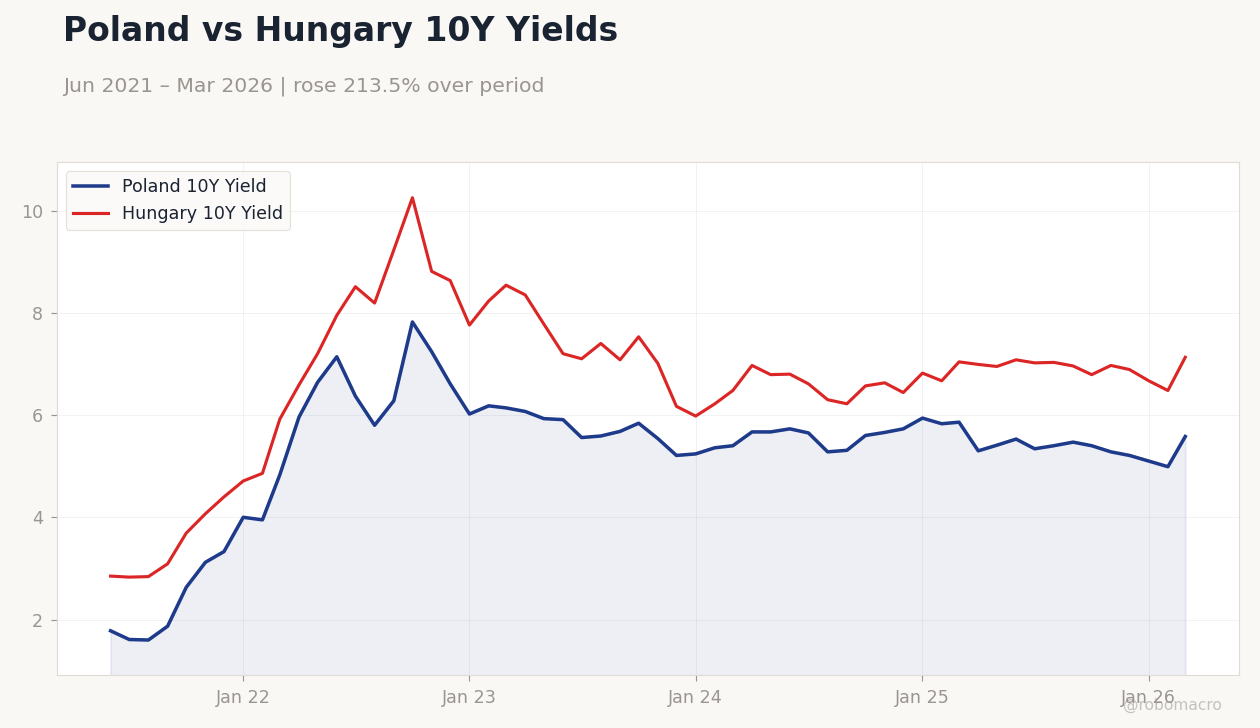

| Poland 10Y Govt Yield | 5.58% | +11.82% |

| Hungary 10Y Govt Yield | 7.13% | +10.03% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Poland vs Hungary 10Y Yields | Type: macro_line | Poland 10Y Yield: 5.58 (2026-03-01) | Range: 1.6–7.82 | Trend(6pt): 1.78,5.8,5.84,5.73,4.99,5.58 | Hungary 10Y Yield: 7.13 (2026-03-01) | Range: 2.83–10.25 | Trend(6pt): 2.85,8.19,7.53,6.44,6.48,7.13

Poland vs Hungary 10Y Yields | Type: macro_line | Poland 10Y Yield: 5.58 (2026-03-01) | Range: 1.6–7.82 | Trend(6pt): 1.78,5.8,5.84,5.73,4.99,5.58 | Hungary 10Y Yield: 7.13 (2026-03-01) | Range: 2.83–10.25 | Trend(6pt): 2.85,8.19,7.53,6.44,6.48,7.13

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| GDP Growth Quarter-over-Quarter Preliminary | 1 | - | 03:30 |

| GDP Growth Year-over-Year Preliminary | 4 | - | 03:30 |

| Consumer Confidence Index | 85.50 | - | 03:00 |

- Hungary inaugurates new PM Peter Magyar, ending Orban's 16-year rule, potentially easing EU fund flows and boosting investor sentiment in the region.

- Polish and Hungarian 10Y government yields jumped over 10 basis points, reflecting heightened risk premiums amid global geopolitical tensions and mixed equity performance.

- Turkish equities edged higher while Polish assets dipped, with currencies showing modest fluctuations against the euro.

Yesterday's Recap

Emerging Europe markets displayed mixed performances with no major data releases on May 10. Turkey's BIST 100 index rose 0.15% to 15,062.70, buoyed by lira stability despite a 0.33% weakening in USD/TRY to 45.38. In Poland, the iShares Poland ETF fell 0.28% to 39.03, while EUR/PLN appreciated 0.19% to 4.24, signaling mild zloty pressure.

Hungarian assets saw EUR/HUF decline 0.26% to 355.00, but the 10Y government yield surged 10.03 basis points to 7.13%, indicating investor caution. Czech EUR/CZK edged up 0.08% to 24.31 amid quiet trading. Poland's 10Y yield spiked 11.82 basis points to 5.58%, the sharpest move among peers, possibly linked to broader EM risk aversion.

No notable updates from Romania, where markets remained subdued without fresh catalysts.

The Day Ahead

Attention turns to Poland's preliminary Q1 GDP figures on May 14, with quarter-over-quarter growth previously at 1% and year-over-year at 4%, offering insights into the largest CEE economy's resilience amid eurozone linkages. Consensus estimates are unavailable, but a softer print could pressure the NBP's stance. Turkey's consumer confidence index is due on May 18, following a previous reading of 85.5, potentially highlighting sentiment amid high inflation and political dynamics.

No immediate releases for Czech Republic, Hungary, or Romania tomorrow, allowing markets to digest global news. Investors will monitor any spillover from Hungary's political transition under new PM Peter Magyar. Overall, the light calendar may keep focus on FX volatility and yield curves.

Other Economic Notes

Broader themes in Emerging Europe emphasize energy import vulnerabilities, particularly from Russian gas, though diversification efforts like Azeri supplies to Turkey and Romania provide some buffer. EU fund disbursements remain critical for Poland and Hungary, with the recent leadership change in Budapest potentially accelerating cohesion fund releases. Inflation divergence persists, with Turkey's elevated levels contrasting CEE peers' progress toward euro convergence criteria.