Emerging Europe Macro Daily(Beta Mode)

Poland CPI Climbs, CEE Equities Slide

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| BIST 100 | 14,367.60 | -1.89% |

| iShares Poland | 38.66 | -2.64% |

| EUR/PLN | 4.25 | +0.23% |

| EUR/HUF | 361.50 | +1.65% |

| EUR/CZK | 24.32 | +0.11% |

| USD/TRY | 45.56 | +0.05% |

| Brent Crude | 111.13 | +1.71% |

| Gold | 4,542.10 | -0.30% |

| Bitcoin | 76,976.19 | -1.48% |

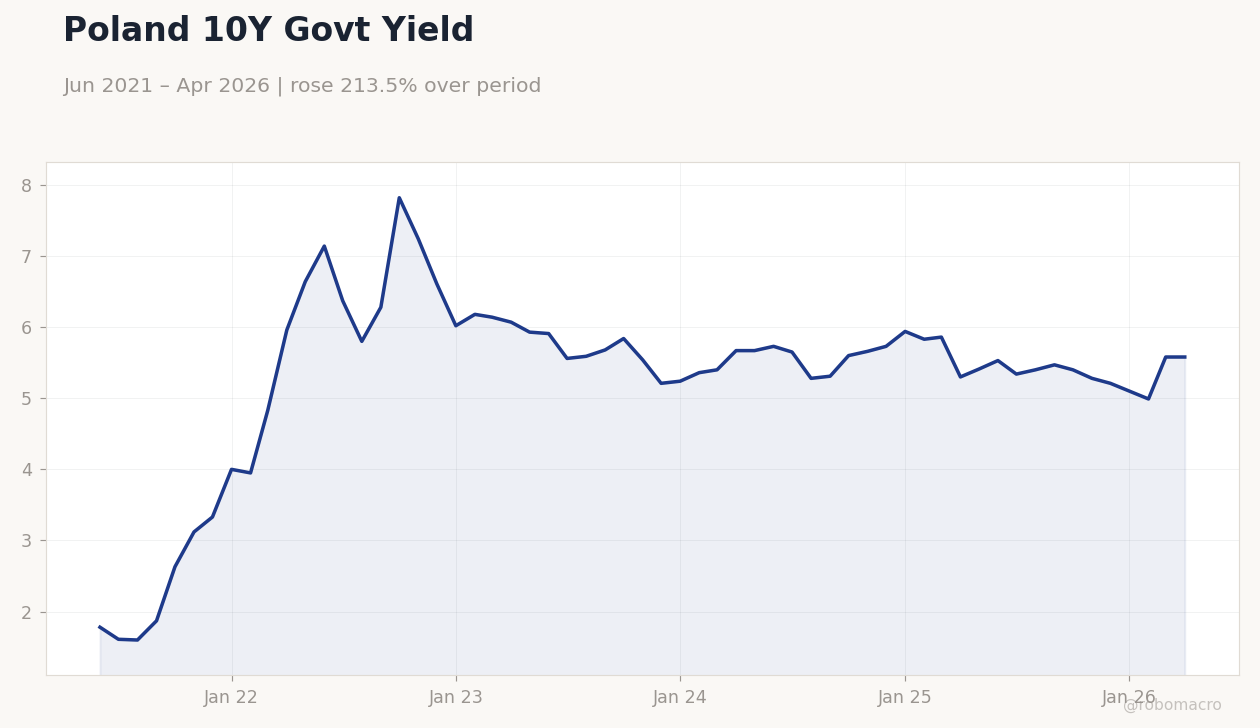

| Poland 10Y Govt Yield | 5.58% | +0.00% |

| Hungary 10Y Govt Yield | 6.27% | -12.06% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Poland 10Y Govt Yield | Type: macro_line | Yield %: 5.58 (2026-04-01) | Range: 1.6–7.82 | Trend(6pt): 1.78,5.8,5.84,5.73,4.99,5.58

Poland 10Y Govt Yield | Type: macro_line | Yield %: 5.58 (2026-04-01) | Range: 1.6–7.82 | Trend(6pt): 1.78,5.8,5.84,5.73,4.99,5.58

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Consumer Confidence Index | 85.50 | - | 03:00 |

| Balance of Trade Final | -11,200m | -8,510m | 03:00 |

| Business Confidence Index | 100.60 | - | 03:00 |

- Polish April CPI rose to 3.2% y/y, with May likely breaching NBP upper tolerance band.

- Regional equities fell sharply, led by 2.64% drop in iShares Poland and 1.89% decline in BIST 100.

- EUR/PLN edged up 0.23% to 4.25 while Hungary 10Y yields fell 12.06% amid thin data flow.

Yesterday's Recap

Polish April CPI printed 3.2% y/y, up from 3.0% in March and keeping the May reading on track to test the NBP’s 3.5% upper tolerance. Market participants priced reduced odds of an NBP cut before September. Regional equities closed lower, with the Polish ETF falling 2.64% and BIST 100 dropping 1.89% as carry-trade appetite in Turkey cooled.

EUR/PLN rose 0.23% to 4.25 while EUR/HUF climbed 1.65% to 361.50. Hungary 10Y yields dropped sharply to 6.27%. Brent crude gained 1.71% to $111.13, adding to imported energy costs for the region.

Romania and Czech data remained quiet, with attention focused on Polish inflation trajectory and Turkish confidence prints due today.

The Day Ahead

Turkey releases its Consumer Confidence Index at 03:00 ET, following the prior 85.5 print. Markets will watch for any further softening that could reinforce CBRT’s current policy stance. No major releases are scheduled for Poland, Czech Republic, Hungary or Romania.

EUR/PLN and EUR/HUF volatility may stay elevated after yesterday’s moves. Traders will also monitor any follow-through from Polish inflation data into local fixed-income curves.

Other Economic Notes

Poland’s rising inflation path narrows the window for NBP easing and supports PLN carry. Hungary’s sharp yield compression suggests domestic demand for duration despite forint weakness. Turkey’s structurally high inflation continues to differentiate its policy cycle from the rest of the region.

Energy price gains add a common headwind for net importers across CEE. EU fund disbursements remain a key swing factor for fiscal and growth outlooks in Poland and Hungary.

Global Macro News

The ECB deposit rate sits at 2.00%, providing a stable anchor for CEE central banks that track euro-area policy closely. Eurozone unemployment at 6.70% signals steady labor-market conditions that support external demand for Polish and Czech exports. Softer US data overnight weighed on global risk sentiment and contributed to the regional equity sell-off.

<i>↓ p.2</i>