Emerging Europe Macro Daily(Beta Mode)

Poland's Gold Reserves Near 600 Tons, Forint Rallies

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| BIST 100 | 13,163.90 | -6.05% |

| iShares Poland | 39.76 | +0.03% |

| EUR/PLN | 4.24 | -0.04% |

| EUR/HUF | 358.66 | +0.15% |

| EUR/CZK | 24.27 | -0.05% |

| USD/TRY | 45.74 | +0.32% |

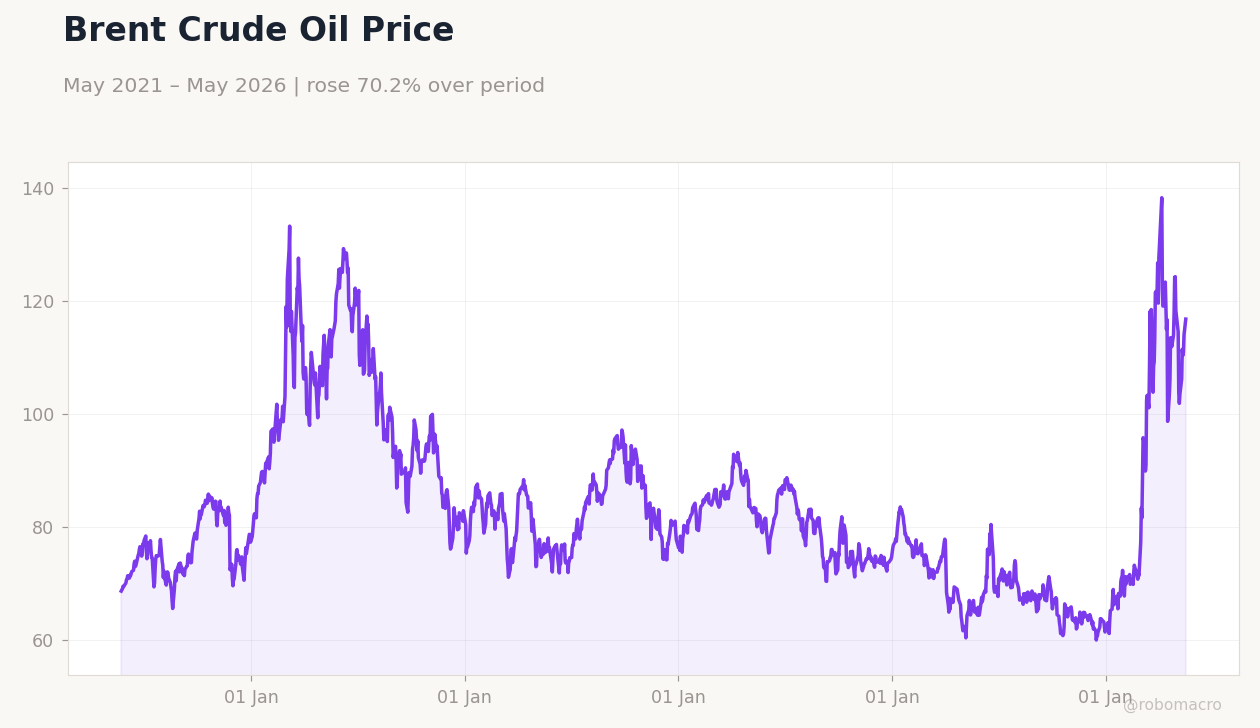

| Brent Crude | 104.21 | +1.59% |

| Gold | 4,527.20 | -0.28% |

| Bitcoin | 77,599.73 | +0.18% |

| Poland 10Y Govt Yield | 5.58% | +0.00% |

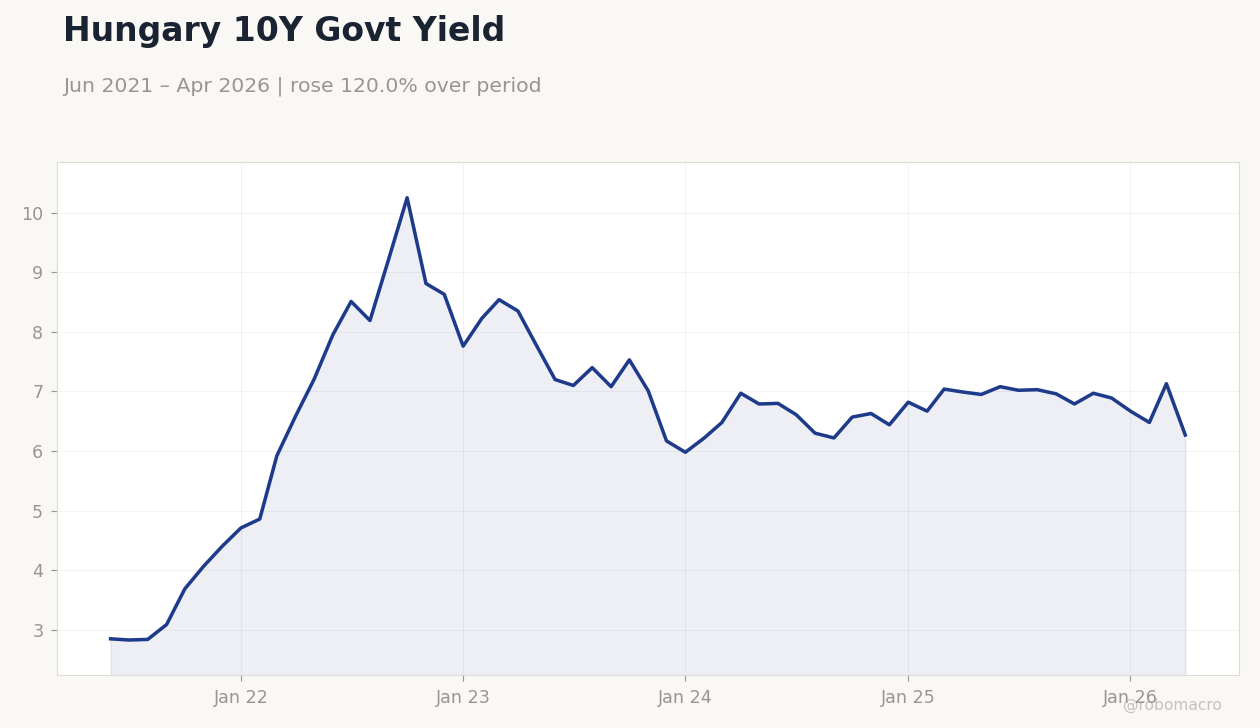

| Hungary 10Y Govt Yield | 6.27% | -12.06% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Hungary 10Y Govt Yield | Type: macro_line | Yield %: 6.27 (2026-04-01) | Range: 2.83–10.25 | Trend(6pt): 2.85,8.19,7.53,6.44,6.48,6.27

Hungary 10Y Govt Yield | Type: macro_line | Yield %: 6.27 (2026-04-01) | Range: 2.83–10.25 | Trend(6pt): 2.85,8.19,7.53,6.44,6.48,6.27

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Balance of Trade Final | -11,200m | -8,510m | 03:00 |

| Business Confidence Index | 100.60 | - | 03:00 |

| Headline Unemployment Rate | 6.10 | 6 | 03:30 |

| Inflation Rate Year-over-Year Preliminary | 3.20 | - | 03:30 |

- Poland's NBP gold holdings approach 600 tons, overtaking Turkey and underscoring sovereignty focus amid geopolitical risks.

- Hungarian forint strengthens sharply after new prime minister's Poland visit restores bilateral ties and eases investor concerns.

- BIST 100 falls 6.05% while Hungary 10Y yields drop 12.06% as regional markets digest mixed equity and bond moves.

Yesterday's Recap

Emerging Europe markets showed divergence on May 21. BIST 100 declined 6.05% to 13,163.90 amid lingering Turkish inflation pressures, while iShares Poland gained 0.03%. EUR/PLN eased 0.04% to 4.24 and EUR/CZK fell 0.05% to 24.27, but EUR/HUF rose 0.15% to 358.66 and USD/TRY climbed 0.32% to 45.74.

Poland 10Y yields held steady at 5.58% while Hungary 10Y yields plunged. News highlighted Poland's gold reserves nearing 600 tons, with NBP continuing purchases as a buffer against global uncertainty. Hungary's new prime minister received a warm welcome in Warsaw during his first official trip, aiming to repair strained Polish-Hungarian relations.

Nigeria and Poland advanced talks on digital economy, defence and agriculture partnerships. Brent crude rose 1.59% to 104.21 while gold slipped 0.28%.

The Day Ahead

Turkey releases final balance of trade and business confidence index at 03:00 ET, with consensus pointing to a narrower deficit than the prior -11.2 billion. Markets will watch for signs of improving external balances ahead of summer tourism. Poland's headline unemployment rate is due May 26 at a consensus 6.0%, followed by preliminary inflation data on May 29.

No major releases are scheduled for Czech Republic, Hungary or Romania in the immediate window. Traders will monitor any follow-through from the Hungary-Poland diplomatic engagement and its potential impact on forint stability.

Other Economic Notes

Poland continues to build gold reserves as a strategic hedge, now exceeding Turkey's holdings and reinforcing NBP's independence narrative. Hungary faces short-term limits to forint gains despite recent political optimism, with analysts expecting consolidation rather than further rapid appreciation. Romania's EU fund disbursements remain on track for June, supporting investment-led growth while euro-adoption convergence stays distant.

Energy import reliance continues to tie regional outlooks to Brent movements, with Polish LNG terminals operating near full capacity.