Emerging Europe Macro Daily(Beta Mode)

Polish Unemployment Due, Hungarian Yields Slide

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| BIST 100 | 13,808.20 | +4.89% |

| iShares Poland | 39.95 | +0.48% |

| EUR/PLN | 4.23 | -0.08% |

| EUR/HUF | 356.78 | -0.38% |

| EUR/CZK | 24.27 | -0.03% |

| USD/TRY | 45.72 | +0.02% |

| Brent Crude | 100.21 | -3.22% |

| Gold | 4,523.20 | +0.05% |

| Bitcoin | 77,289.99 | +0.80% |

| Poland 10Y Govt Yield | 5.58% | +0.00% |

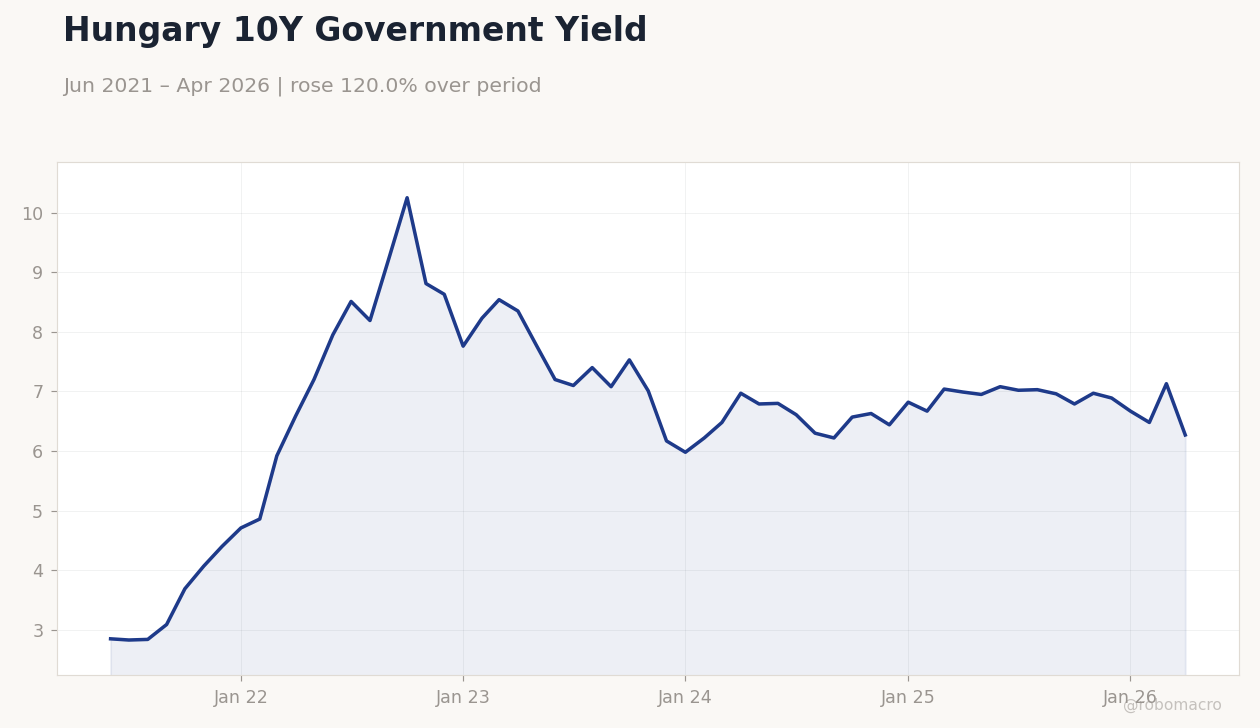

| Hungary 10Y Govt Yield | 6.27% | -12.06% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Hungary 10Y Government Yield | Type: macro_line | Yield %: 6.27 (2026-04-01) | Range: 2.83–10.25 | Trend(6pt): 2.85,8.19,7.53,6.44,6.48,6.27

Hungary 10Y Government Yield | Type: macro_line | Yield %: 6.27 (2026-04-01) | Range: 2.83–10.25 | Trend(6pt): 2.85,8.19,7.53,6.44,6.48,6.27

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Headline Unemployment Rate | 6.10 | 6 | 23:30 |

| Inflation Rate Year-over-Year Preliminary | 3.20 | - | 23:30 |

| Tuesday (2026-05-26) | |||

| Headline Unemployment Rate | 6.10 | 6 | 23:30 |

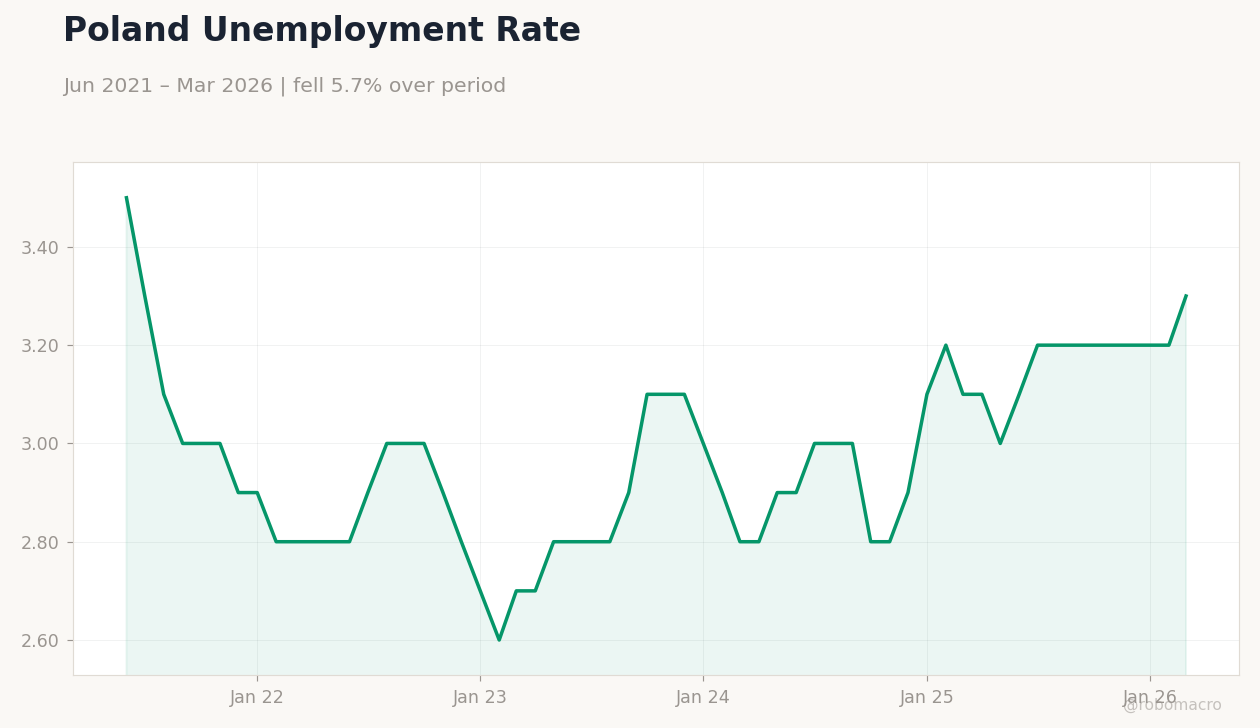

- Poland’s headline unemployment rate is due today with consensus pointing to a 6.0% print from 6.1%.

- Hungarian 10-year government yields fell 12.06% while the forint posted modest gains against the euro.

- BIST 100 rose 4.89% as Turkish equities outperformed amid stable USD/TRY at 45.72.

Yesterday's Recap

No major data releases occurred across Poland, Czech Republic, Hungary, Romania or Turkey on 24 May. Equity markets showed selective strength, with the BIST 100 advancing 4.89% while iShares Poland gained 0.48%. EUR/PLN eased 0.08% to 4.23 and EUR/HUF declined 0.38% to 356.78, reflecting forint resilience.

Hungary’s 10-year yield dropped sharply to 6.27%, signalling reduced local risk premia. EUR/CZK held near 24.27 with minimal movement. Brent crude fell 3.22% to 100.21, easing imported energy costs for the region.

Poland’s aviation fuel reserves were confirmed secure, removing a near-term supply concern.

The Day Ahead

Poland’s headline unemployment rate for April will be released at 23:30 ET, with the market expecting a decline to 6.0%. The print will provide the latest labour-market signal ahead of next week’s preliminary inflation reading. No other high-impact releases are scheduled for Czech Republic, Hungary, Romania or Turkey.

Markets will also monitor any follow-through from Nigeria-Poland bilateral talks on defence and digital economy cooperation. Positioning ahead of the Polish data is likely to keep EUR/PLN in a narrow range near 4.23.

Other Economic Notes

Poland’s labour market remains tight despite the expected modest easing in the unemployment rate. Hungary continues to benefit from forint appreciation that has lowered imported inflation pressures. Regional equity flows remain supported by the sharp decline in Hungarian yields.

Energy price weakness offers relief to net importers Poland, Czech Republic and Hungary. Bilateral economic initiatives between Poland and Nigeria may gradually expand non-EU trade channels for Polish exporters.

Global Macro News

The ECB maintains its deposit rate at 2.00%, anchoring euro-area policy expectations that influence CNB and MNB decisions. Eurozone unemployment stands at 6.70%, providing a stable external benchmark for CEE labour markets. <i>↓ p.2</i>