Emerging Europe Macro Daily(Beta Mode)

Polish Unemployment Falls, Hungarian Yields Slide

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| BIST 100 | 13,662.80 | -1.64% |

| iShares Poland | 40.45 | +1.25% |

| EUR/PLN | 4.23 | +0.12% |

| EUR/HUF | 355.44 | +0.05% |

| EUR/CZK | 24.26 | +0.07% |

| USD/TRY | 45.89 | -0.01% |

| Brent Crude | 95.10 | -4.50% |

| Gold | 4,510.00 | +0.21% |

| Bitcoin | 75,489.58 | -2.32% |

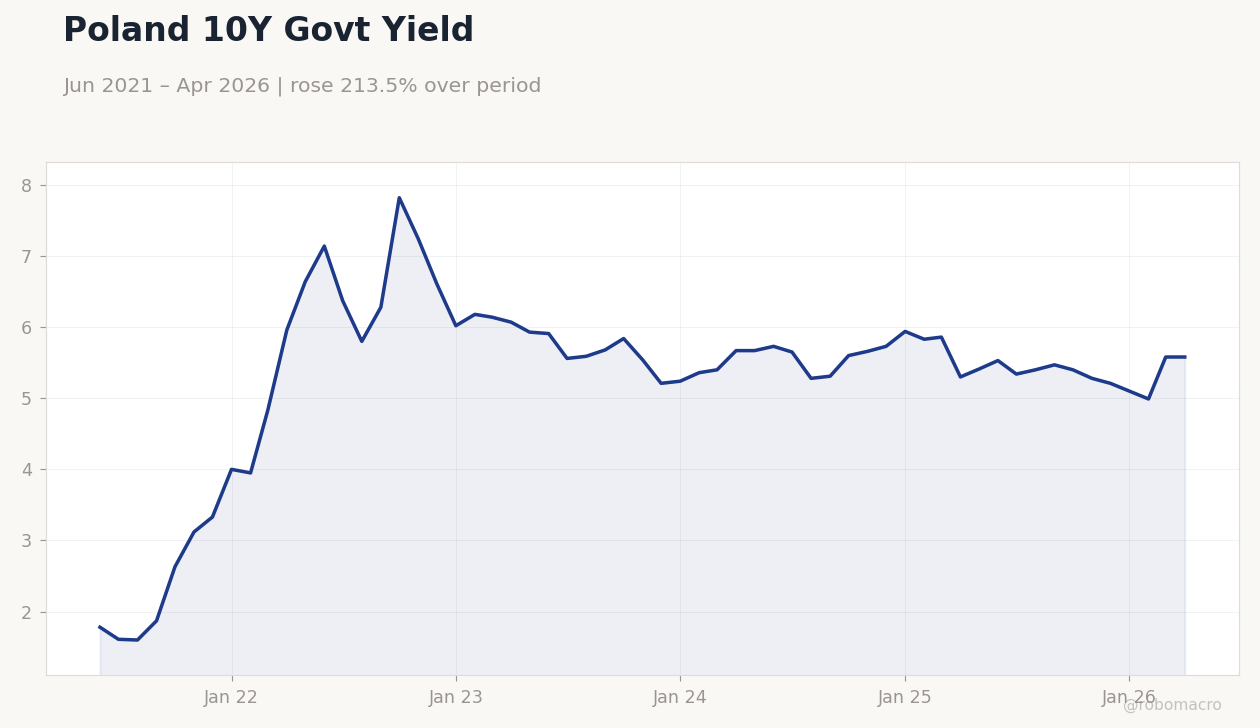

| Poland 10Y Govt Yield | 5.58% | +0.00% |

| Hungary 10Y Govt Yield | 6.27% | -12.06% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Headline Unemployment Rate | 6.10 | 6 | 6 |

Poland 10Y Govt Yield | Type: macro_line | Yield %: 5.58 (2026-04-01) | Range: 1.6–7.82 | Trend(6pt): 1.78,5.8,5.84,5.73,4.99,5.58

Poland 10Y Govt Yield | Type: macro_line | Yield %: 5.58 (2026-04-01) | Range: 1.6–7.82 | Trend(6pt): 1.78,5.8,5.84,5.73,4.99,5.58

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Inflation Rate Year-over-Year Preliminary | 3.20 | - | 23:30 |

- Poland unemployment rate declined to 6.0% from 6.1%, matching consensus.

- MNB holds base rate at 6.25% with June cut now in view after forint strength.

- BIST 100 drops 1.64% while Polish equities gain 1.25% and Hungary 10Y yields fall 12.06%.

Yesterday's Recap

Poland reported its headline unemployment rate at 6.0% for the reference period, down from 6.1% and in line with market expectations. Hungarian 10-year government bond yields plunged 12.06% to 6.27% on improved sentiment after the forint rally. The BIST 100 index fell 1.64% to close at 13,662.80.

iShares Poland ETF advanced 1.25% to 40.45. EUR/PLN rose 0.12% to 4.23 while EUR/HUF and EUR/CZK posted modest gains of 0.05% and 0.07%. Brent crude declined 4.50% to 95.10, pressuring Turkish assets.

Poland 10Y yields held steady at 5.58%. The MNB kept its base rate unchanged at 6.25% as expected, citing forint improvement and leaving the door open for a possible June move. No other CEE central banks held policy meetings.

The Day Ahead

Poland will release its preliminary inflation rate year-over-year on 28 May at 23:30 ET, with markets watching for any deviation from the prior 3.2% print. MNB Governor Mihály Varga is scheduled to hold a press conference following yesterday’s decision. No other high-impact data are due from Czechia, Romania or Turkey.

Regional FX desks will monitor ECB signals for spillover effects on CEE currencies. Equity flows may remain sensitive to global energy price swings. The ECB deposit rate remains at 2.00%, anchoring expectations for steady euro-area policy.

Other Economic Notes

Poland faces an approaching demographic low that threatens long-term labor supply and growth potential. The mObywatel digital government app has surpassed 12 million users, positioning Poland as Europe’s leader in public-sector digital services. EUR/PLN traded near 4.23 on 27 May, little changed from the prior session.

Broader CEE economies continue to benefit from EU single-market access despite persistent energy import dependence. Hungary’s new guest-worker rules could reduce GDP by up to 2,000 billion forints and tax revenue by 300 billion forints according to local estimates.

Global Macro News

ECB President Lagarde reiterated that the central bank will do what is necessary to tame inflation, with the deposit rate fixed at 2.00%. Eurozone unemployment stood at 6.70% in the latest available reading. <i>↓ p.2</i>