Emerging Europe Macro Daily(Beta Mode)

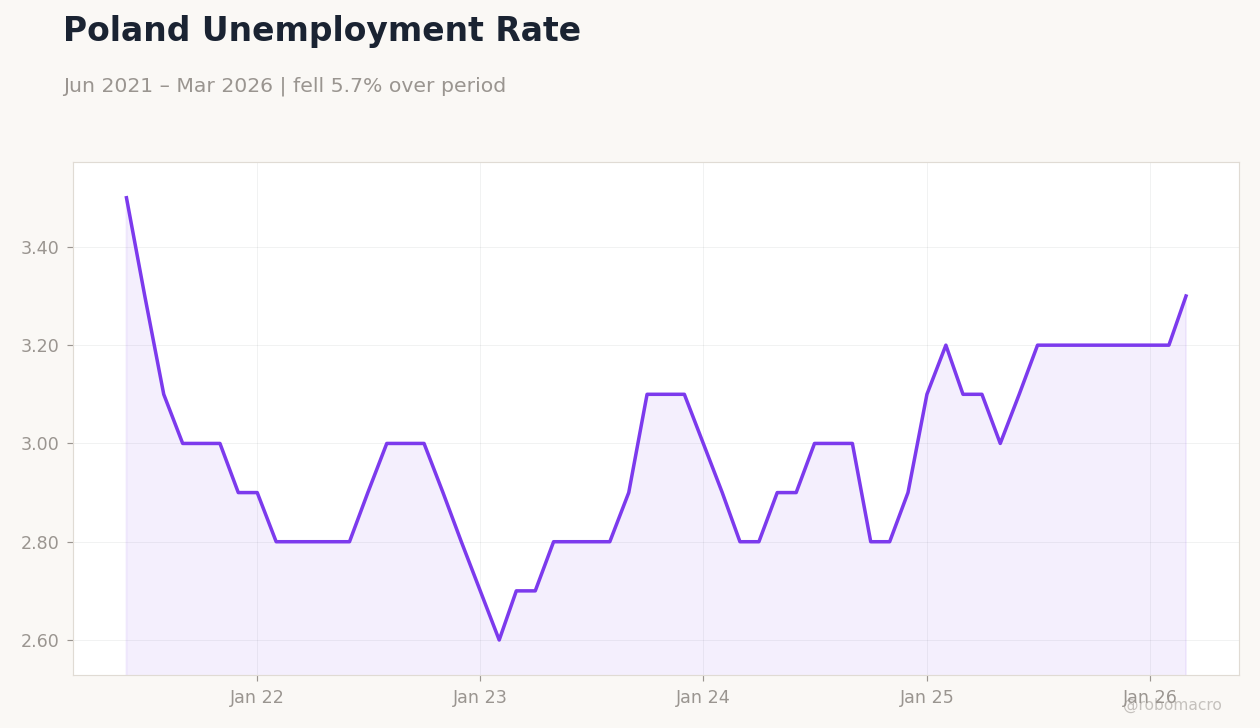

Poland Jobless Rate Hits 6% as CPI Looms

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| BIST 100 | 13,662.80 | -1.64% |

| iShares Poland | 40.60 | +0.42% |

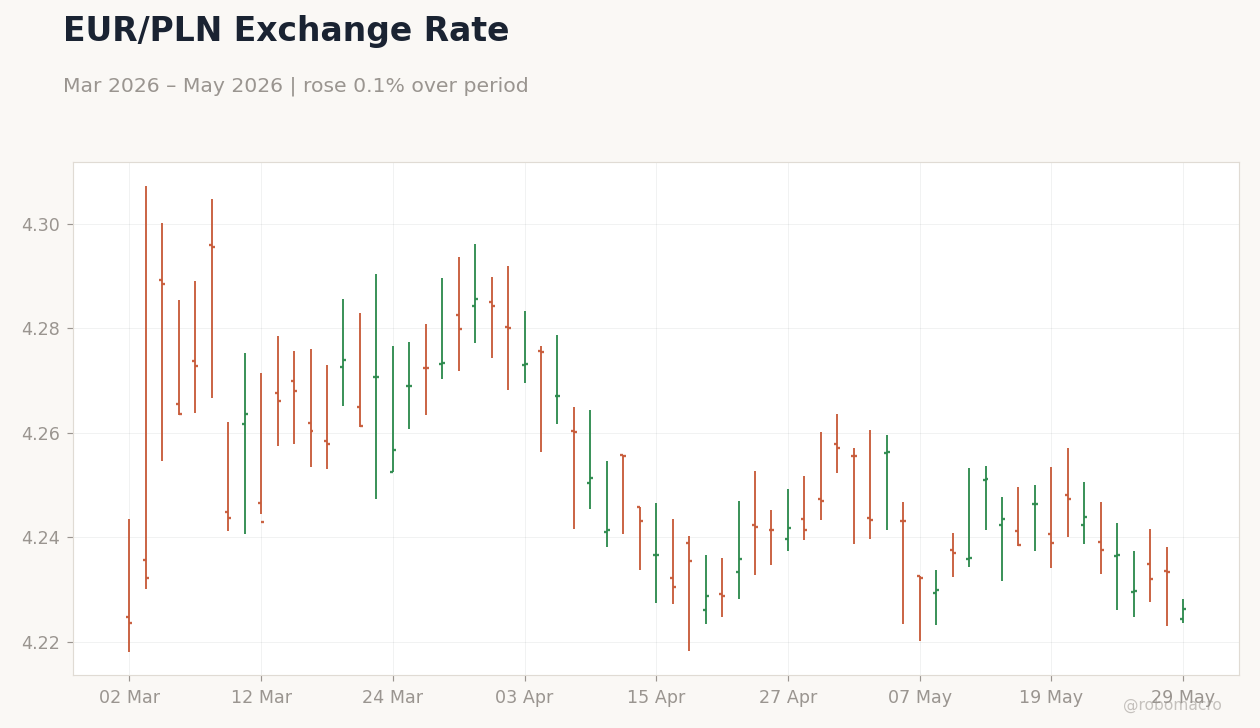

| EUR/PLN | 4.23 | -0.17% |

| EUR/HUF | 354.49 | +0.33% |

| EUR/CZK | 24.28 | -0.01% |

| USD/TRY | 45.89 | -0.01% |

| Brent Crude | 91.52 | -2.34% |

| Gold | 4,549.20 | +1.11% |

| Bitcoin | 73,684.00 | +0.20% |

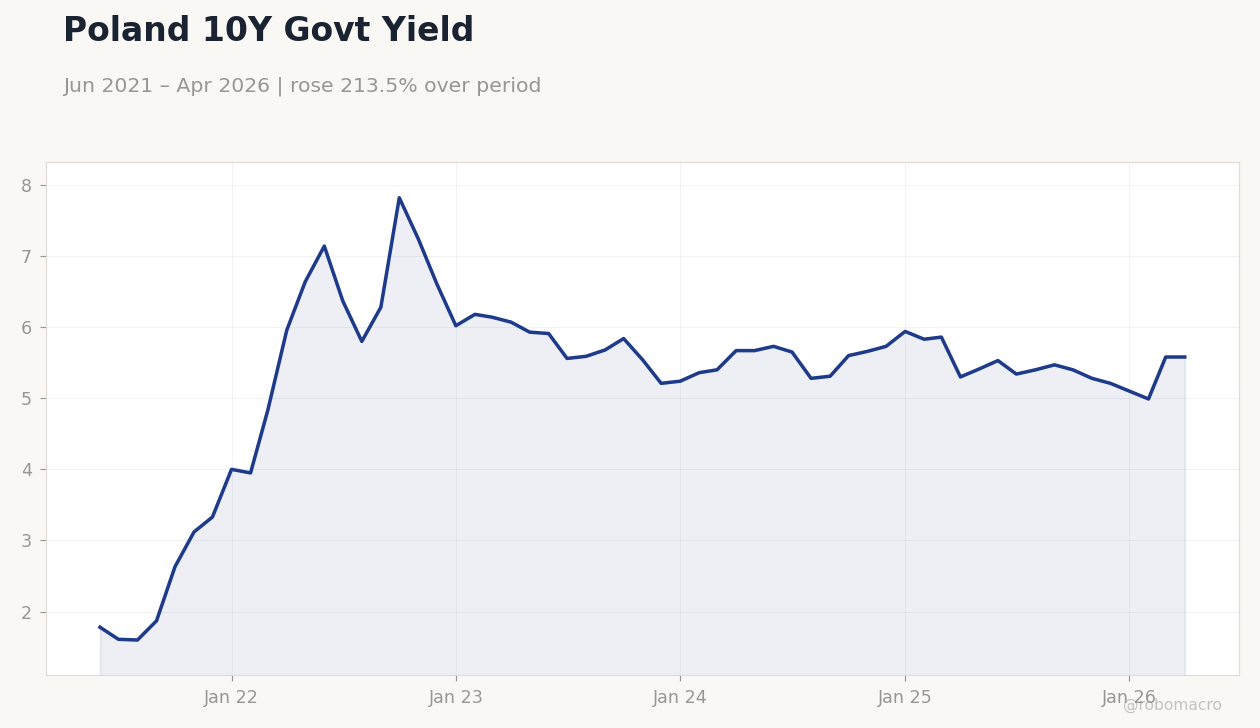

| Poland 10Y Govt Yield | 5.58% | +0.00% |

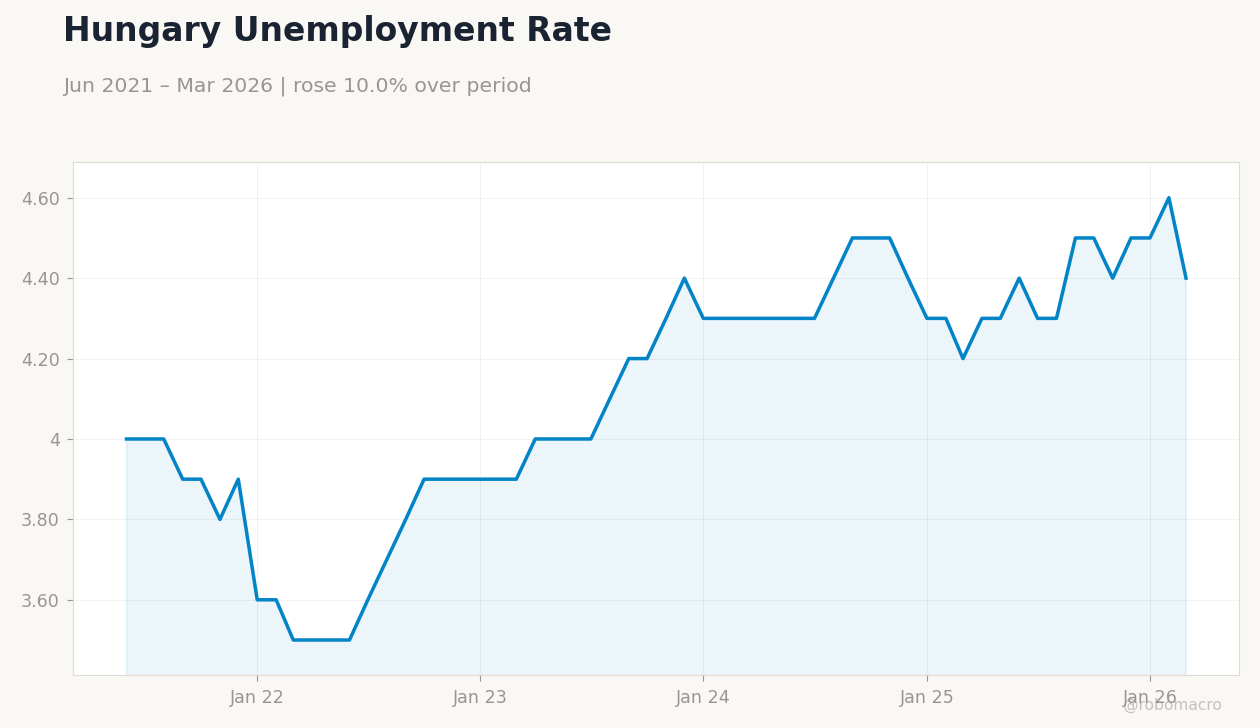

| Hungary 10Y Govt Yield | 6.27% | -12.06% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Headline Unemployment Rate | 6.10 | 6 | 6 |

Poland 10Y Govt Yield | Type: macro_line | Yield %: 5.58 (2026-04-01) | Range: 1.6–7.82 | Trend(6pt): 1.78,5.8,5.84,5.73,4.99,5.58

Poland 10Y Govt Yield | Type: macro_line | Yield %: 5.58 (2026-04-01) | Range: 1.6–7.82 | Trend(6pt): 1.78,5.8,5.84,5.73,4.99,5.58

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Inflation Rate Year-over-Year Preliminary | 3.20 | - | 23:30 |

- Poland’s headline unemployment rate declined to 6% in April, beating consensus and signaling labor market resilience ahead of today’s flash CPI release.

- Hungarian 10-year yields plunged 12% to 6.27% while the forint weakened modestly against the euro, reflecting divergent local bond dynamics.

- BIST 100 fell 1.64% to 13,662.80 amid broader risk-off sentiment, with EUR/PLN easing 0.17% to 4.23 on Polish zloty strength.

Yesterday's Recap

Poland’s unemployment rate printed at 6%, down from 6.1% previously and in line with the 6% consensus, underscoring steady employment conditions in the region’s largest EU economy. Equity markets showed modest gains for Polish assets, with iShares Poland rising 0.42% to 40.60 while the zloty firmed against the euro to 4.23. Hungary’s 10-year government yield dropped sharply by 12.06% to 6.27%, suggesting localized demand for Hungarian bonds despite forint softening of 0.33% versus the euro.

Turkish equities underperformed, with the BIST 100 declining 1.64% to close at 13,662.80 as USD/TRY held steady near 45.89. Brent crude fell 2.34% to 91.52, easing imported energy costs for the five-country region, while gold advanced 1.11% to 4,549.20. Czech and Romanian markets remained quiet with negligible moves in EUR/CZK and local yields.

Overall, activity concentrated on Poland’s labor data and selective Hungarian fixed-income buying.

The Day Ahead

Poland’s May inflation rate year-over-year preliminary is scheduled for release at 23:30 ET, providing the first read on price trends after April’s 3.2% print. No major data releases are listed for the Czech Republic, Hungary, Romania or Turkey tomorrow. Markets will monitor any follow-through from today’s Polish CPI for NBP policy signals.

Regional FX desks are likely to focus on EUR/PLN and EUR/HUF reactions to the inflation figure. Energy price moves in Brent will continue to influence import-dependent economies across Emerging Europe.

Other Economic Notes

Poland’s improving labor market supports household consumption while keeping wage pressures contained ahead of euro-area convergence discussions. Hungary’s sharp yield compression highlights selective investor appetite for local duration despite ongoing EU fund disbursement delays. Shared energy import dependence across Poland, Hungary, Czech Republic and Romania leaves the region exposed to Brent volatility, even as prices eased yesterday.

Romania and the Czech Republic saw limited market reaction, consistent with their lower news flow relative to Poland and Turkey.