Emerging Europe Macro Daily(Beta Mode)

NBP Holds, Turkey GDP Growth Slows

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| BIST 100 | 13,838.46 | -0.24% |

| iShares Poland | 40.36 | +0.98% |

| EUR/PLN | 4.23 | -0.20% |

| EUR/HUF | 353.67 | -0.32% |

| EUR/CZK | 24.20 | +0.09% |

| USD/TRY | 46.08 | +0.23% |

| Brent Crude | 94.59 | -0.46% |

| Gold | 4,487.10 | +0.25% |

| Bitcoin | 62,805.79 | -1.56% |

| Poland 10Y Govt Yield | 5.58% | +0.00% |

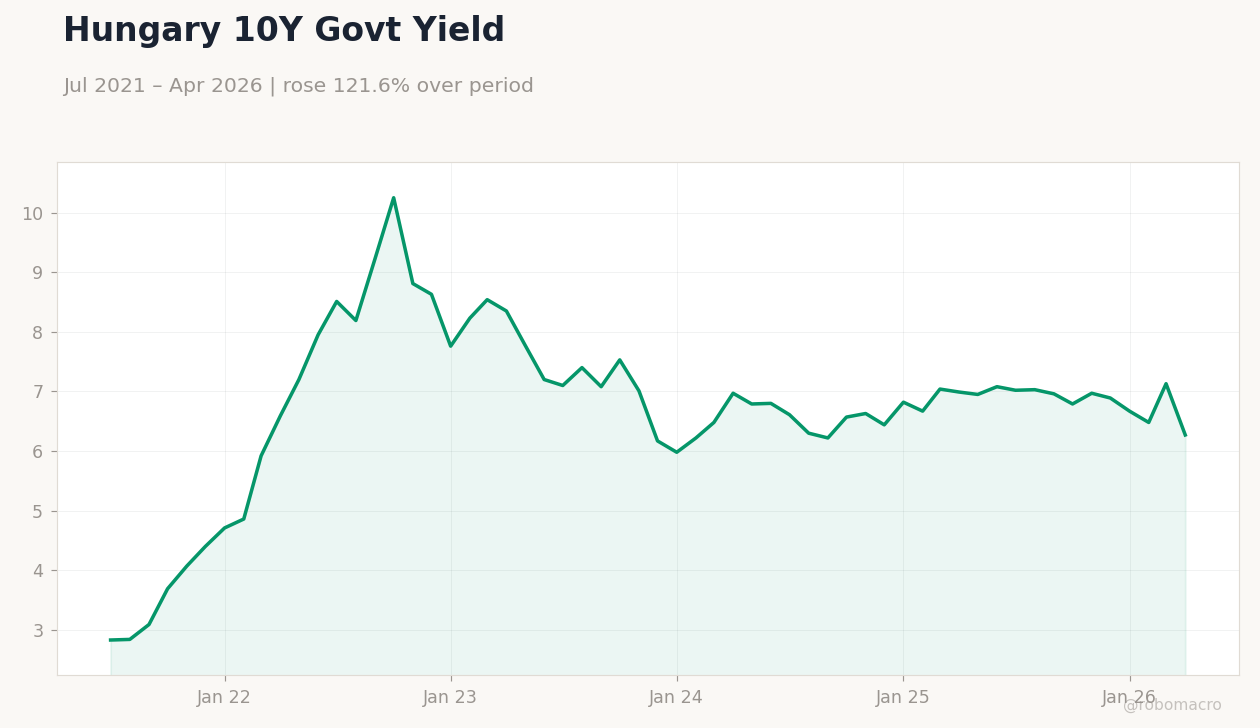

| Hungary 10Y Govt Yield | 6.27% | -12.06% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| GDP Growth Quarter-over-Quarter | 0.40 | - | 0.10 |

| GDP Growth Year-over-Year | 3.40 | 2.70 | 2.50 |

| Central Bank Interest Rate Decision | 3.75 | 3.75 | 3.75 |

| Headline Unemployment Rate | 8.10 | - | 8.20 |

| Balance of Trade Prel | -8,500m | - | -5,600m |

| Inflation Rate Month-over-Month | 4.18 | 1.60 | - |

| Inflation Rate Year-over-Year | 32.37 | 32.50 | - |

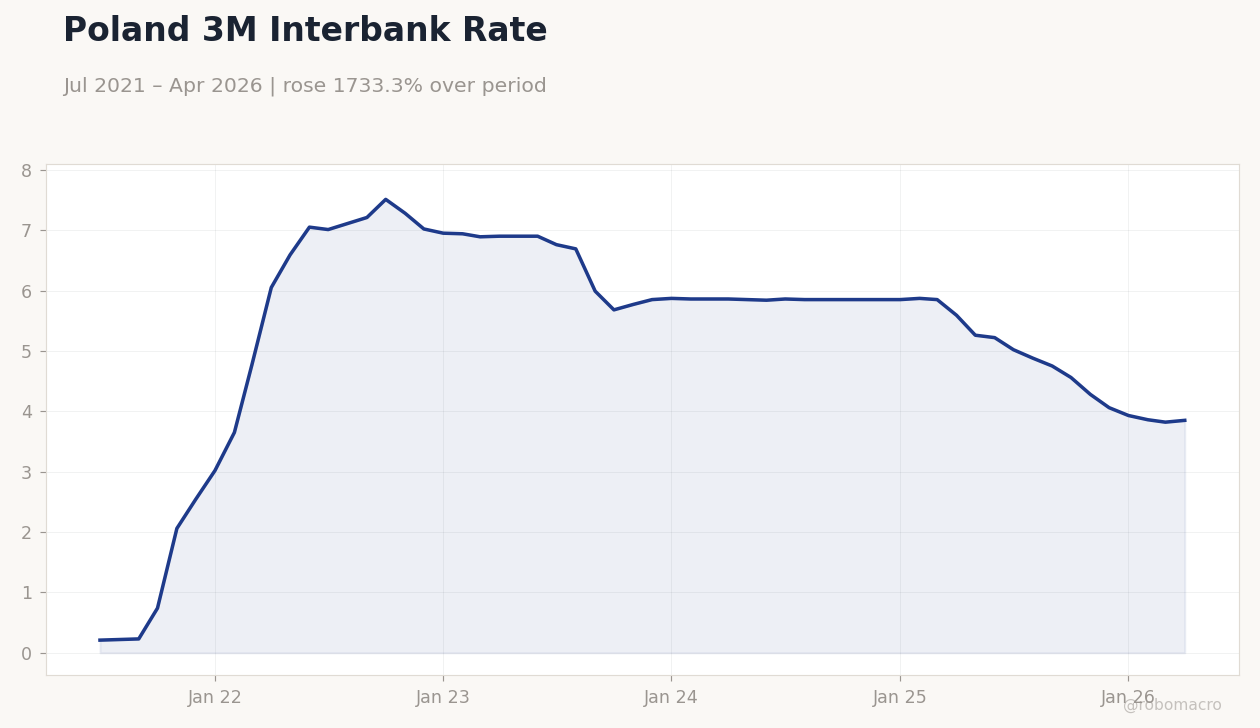

Poland 3M Interbank Rate | Type: macro_line | Percent: 3.85 (2026-04-01) | Range: 0.21–7.51 | Trend(6pt): 0.21,7.21,5.77,5.85,3.82,3.85

Poland 3M Interbank Rate | Type: macro_line | Percent: 3.85 (2026-04-01) | Range: 0.21–7.51 | Trend(6pt): 0.21,7.21,5.77,5.85,3.82,3.85

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- NBP kept its key rate at 3.75% as expected, with the committee voting to hold.

- Turkey’s Q1 GDP rose 2.5% y/y, below the 2.7% consensus, while the trade deficit narrowed to $5.6 bn.

- Polish equities outperformed, with iShares Poland gaining 0.98% as EUR/PLN eased 0.20% to 4.23.

Yesterday's Recap

Poland’s central bank left rates unchanged at 3.75%, citing stable inflation dynamics and external risks. Turkey reported weaker-than-expected Q1 GDP growth of 2.5% y/y and 0.1% q/q, confirming a slowdown from prior quarters. The Turkish unemployment rate edged up to 8.2% while the preliminary trade balance improved to -$5.6 bn.

Equity markets diverged, with Polish shares rising and BIST 100 slipping 0.24%. EUR/HUF fell 0.32% to 353.67 and Hungary’s 10-year yield dropped 12.06% to 6.27%. The EBRD maintained its 3.5% growth forecast for Poland in 2026 despite global uncertainties.

Pending Turkish inflation data for May kept markets focused on CBRT policy durability.

The Day Ahead

No major data releases are scheduled for Emerging Europe today or tomorrow. Attention will turn to any follow-up comments from NBP Governor Glapiński and regional inflation prints later in the week. Markets will also monitor ECB signals for spillover effects on the CNB and MNB.

Turkish inflation figures, now due shortly, remain the key domestic catalyst. External drivers such as Brent crude at $94.59 and gold at $4,487 will influence TRY and HUF flows.

Other Economic Notes

Poland’s large trade deficit with China exceeded €54 bn last year, underscoring structural import dependence. EBRD projections highlight Poland’s resilience relative to peers amid rising global risks. Energy security concerns persist across the region given continued Russian oil flows via the Druzhba pipeline to Hungary and Slovakia.

EU cohesion fund disbursements remain conditional on rule-of-law progress in Hungary, limiting fiscal space. Romania’s euro-adoption timeline continues to face delays from fiscal slippage.

Global Macro News

The ECB deposit rate stands at 2.00%, providing a stable anchor for regional policy divergence. Eurozone unemployment at 6.70% supports a gradual easing bias that CNB and MNB are likely to track. IMF assessments of Saudi non-oil growth at 2% in 2026 offer indirect context for global demand affecting Turkish exports.

<i>↓ p.2</i>