Emerging Europe Macro Daily(Beta Mode)

Polish Stocks Drop as Hungarian Yields Plunge

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| BIST 100 | 13,704.72 | +0.08% |

| iShares Poland | 38.90 | -3.62% |

| EUR/PLN | 4.24 | +0.17% |

| EUR/HUF | 355.69 | +0.59% |

| EUR/CZK | 24.16 | -0.12% |

| USD/TRY | 46.10 | +0.07% |

| Brent Crude | 97.25 | +4.47% |

| Gold | 4,331.60 | -0.13% |

| Bitcoin | 63,163.39 | -0.12% |

| Poland 10Y Govt Yield | 5.58% | +0.00% |

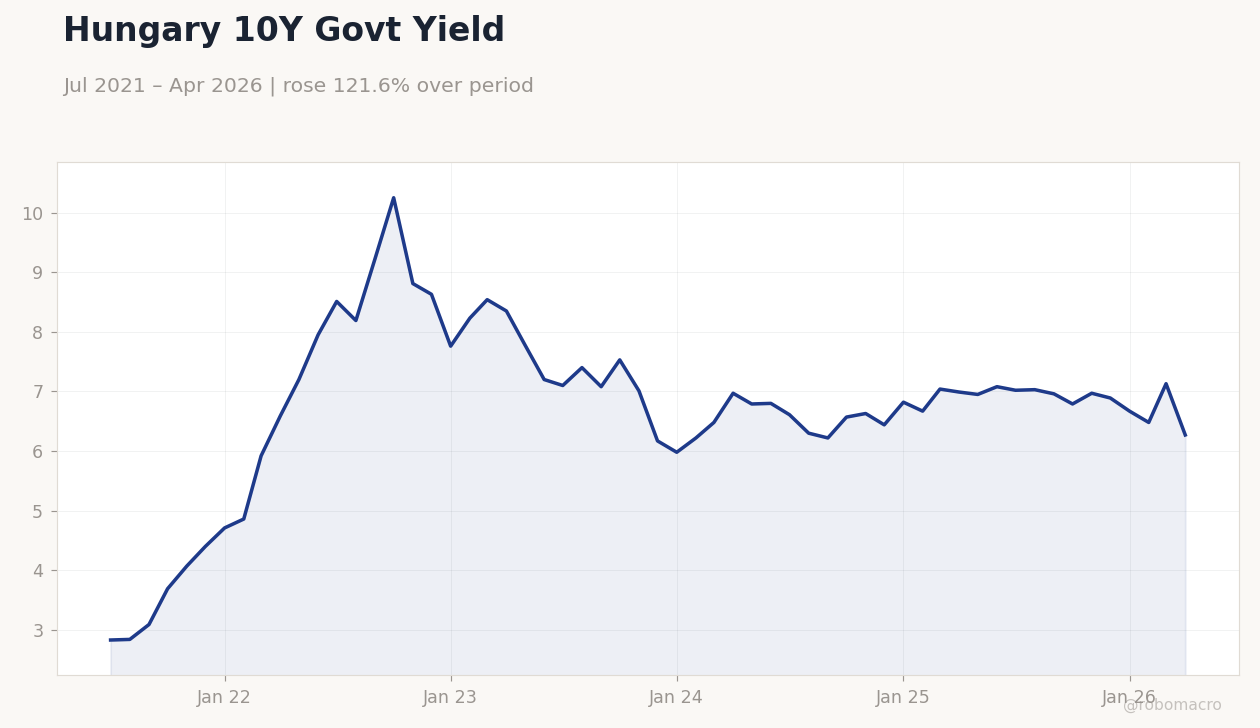

| Hungary 10Y Govt Yield | 6.27% | -12.06% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Hungary 10Y Govt Yield | Type: macro_line | Yield %: 6.27 (2026-04-01) | Range: 2.83–10.25 | Trend(6pt): 2.83,9.23,7.01,6.82,7.13,6.27

Hungary 10Y Govt Yield | Type: macro_line | Yield %: 6.27 (2026-04-01) | Range: 2.83–10.25 | Trend(6pt): 2.83,9.23,7.01,6.82,7.13,6.27

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Industrial Production Year-over-Year | -1.10 | - | 23:00 |

| TCMB Interest Rate Decision | 37 | - | 03:00 |

- Poland equities fell sharply while Hungary 10Y yields declined 12% amid limited data flow.

- EUR/PLN rose to 4.24 and EUR/HUF climbed to 355.69 on regional FX moves.

- Turkey's TCMB rate decision and May industrial production loom as key near-term events.

Yesterday's Recap

Emerging Europe markets showed mixed performance with no major data releases across Poland, Czech Republic, Hungary, Romania or Turkey. iShares Poland dropped 3.62% to 38.90 while BIST 100 edged up 0.08% to 13,704.72. EUR/PLN advanced 0.17% to 4.24 and EUR/HUF gained 0.59% to 355.69, whereas EUR/CZK eased 0.12% to 24.16.

Hungary 10Y yields fell sharply 12.06% to 6.27% while Poland 10Y yields held steady at 5.58%. USD/TRY rose 0.07% to 46.10. News highlighted Romania's Q1 GDP contraction of 1.2% y/y and Hungary's upcoming May inflation print that may support further MNB easing.

Poland continued gold purchases with nearly 17 tons added in May.

The Day Ahead

Turkey releases May industrial production y/y at 23:00 ET followed by the TCMB interest rate decision on 11 June. Markets expect the committee to hold the policy rate at 37%. No scheduled releases appear for Poland, Czech Republic, Hungary or Romania.

Regional FX and equity trading will likely track ECB signals and Brent crude moves, which rose 4.47% to 97.25. Focus remains on Hungary inflation data due tomorrow that could influence MNB timing.

Other Economic Notes

Romania's economy contracted in Q1 while Hungary slipped in the latest EU GDP ranking. Poland continues to attract EU fund disbursements conditional on rule-of-law benchmarks. Energy import dependence remains a shared vulnerability across the EU members despite LNG diversification progress.

Broader trade linkages with the euro area continue to transmit ECB policy effects directly into NBP, CNB, MNB and BNR decisions.

Global Macro News

ECB Deposit Rate stands at 2.00% with Eurozone unemployment at 6.70%. Hawkish ECB commentary on terminal rates weighed on regional equities and supported modest EUR strength against CEE currencies. Brent crude gains to 97.25 bolstered energy exporters but added to imported inflation pressures in Turkey.

Gold at 4,331.60 and Bitcoin at 63,163.39 showed limited movement. Global risk sentiment remains sensitive to US data and any shifts in terminal rate expectations that could affect capital flows into Poland and Hungary. EU rule-of-law reviews continue to gate further disbursements to Warsaw and Budapest.