Emerging Europe Macro Daily(Beta Mode)

CBRT Poised to Hold Rate at 37% After IP Drop

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| BIST 100 | 13,741.90 | -0.86% |

| iShares Poland | 39.38 | -0.43% |

| EUR/PLN | 4.25 | +0.21% |

| EUR/HUF | 356.21 | +0.26% |

| EUR/CZK | 24.14 | -0.10% |

| USD/TRY | 46.15 | +0.07% |

| Brent Crude | 93.45 | +0.38% |

| Gold | 4,106.40 | -0.04% |

| Bitcoin | 62,837.10 | +2.26% |

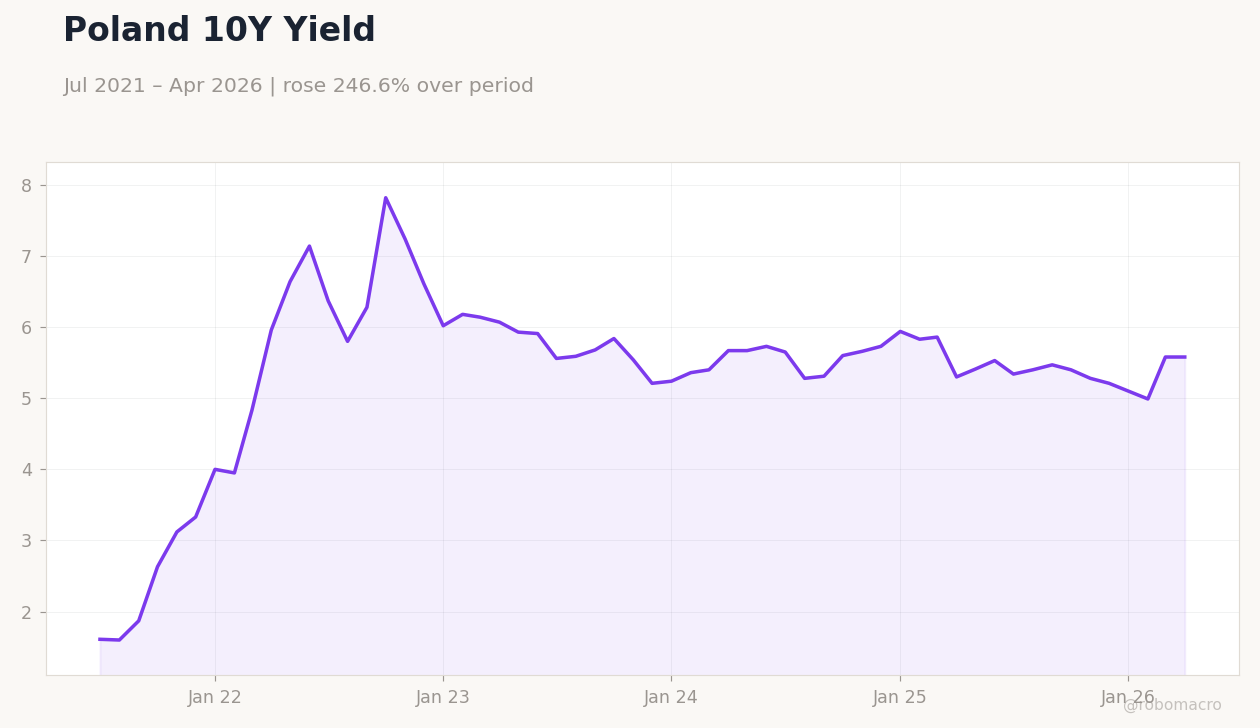

| Poland 10Y Govt Yield | 5.58% | +0.00% |

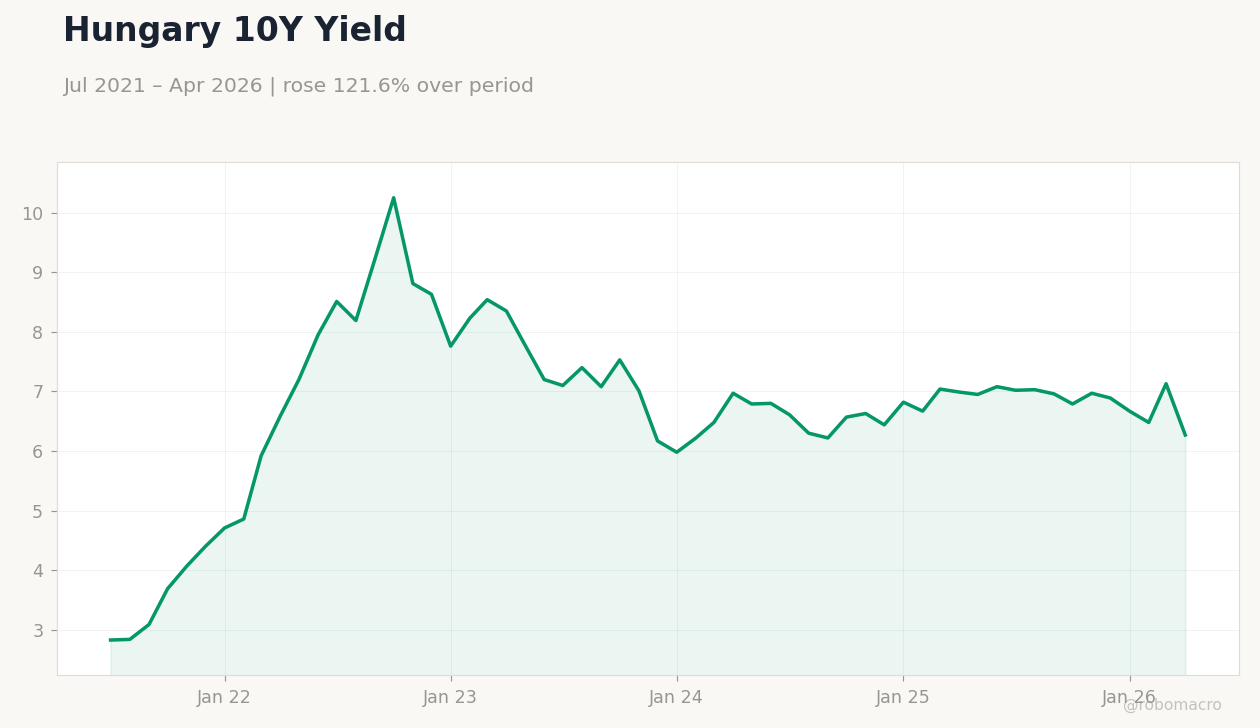

| Hungary 10Y Govt Yield | 6.27% | -12.06% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

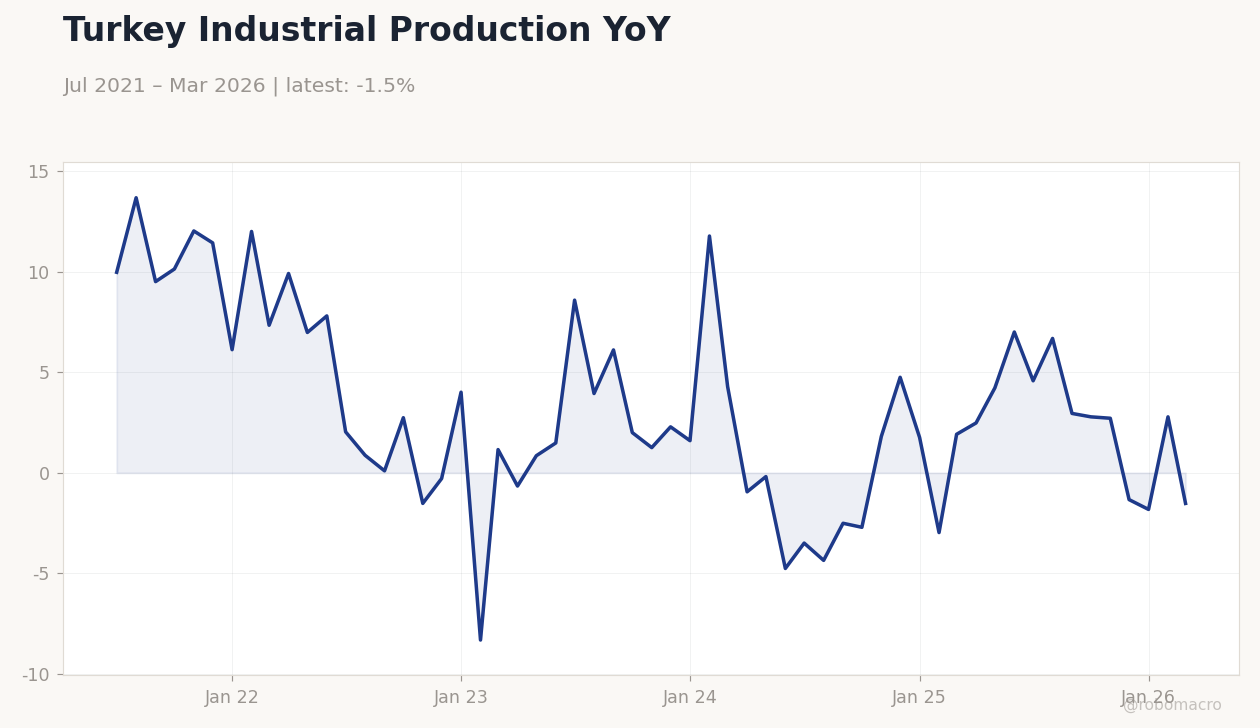

| Industrial Production Year-over-Year | -1.10 | - | - |

Turkey Industrial Production YoY | Type: macro_line | IP YoY %: -1.523 (2026-03-01) | Range: -8.318–13.69 | Trend(5pt): 9.978,0.09872,1.255,1.761,-1.523

Turkey Industrial Production YoY | Type: macro_line | IP YoY %: -1.523 (2026-03-01) | Range: -8.318–13.69 | Trend(5pt): 9.978,0.09872,1.255,1.761,-1.523

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| TCMB Interest Rate Decision | 37 | 37 | 03:00 |

- CBRT expected to hold policy rate at 37% with inflation cooling

- Turkish industrial production contracts further year-over-year

- Hungarian 10Y yields drop sharply on EU fund optimism

Yesterday's Recap

Turkey's industrial production year-over-year data showed ongoing contraction. BIST 100 fell 0.86% to 13,741.90 while iShares Poland declined 0.43% to 39.38 amid limited regional equity momentum. EUR/PLN rose 0.21% to 4.25 as the zloty softened modestly against the euro.

EUR/HUF gained 0.26% to 356.21 and EUR/CZK eased 0.10% to 24.14. Hungary 10Y government yields plunged 12.06% to 6.27% on renewed EU-fund inflows. Brent crude advanced 0.38% to 93.45 while gold held near 4,106.40 and Bitcoin rose 2.26% to 62,837.10.

USD/TRY edged 0.07% higher to 46.15.

The Day Ahead

Markets focus on today's TCMB interest rate decision where consensus expects the committee to hold the policy rate at 37%. Any forward guidance on the pace of future tightening will be scrutinized after recent inflation moderation. Hungarian forint movements will track ECB signals and EU fund developments.

Czech inflation commentary from CNB members may influence koruna pricing ahead of the next meeting. Poland, Romania and Hungary face no major data releases but will monitor broader risk sentiment and energy prices.

Other Economic Notes

Hungary's euro adoption is now seen slipping to 2031-2032 as fiscal and Maastricht criteria convergence lag official targets. Czech National Bank board members flagged persistent inflation risks that could delay further easing. Poland's May budget deficit narrowed more than forecast, bolstering fiscal credibility.

Energy import dependence remains a shared vulnerability across Poland, Hungary and Czechia amid volatile global prices. EU procurement reforms slated for July could alter state spending patterns in Hungary and Romania.

Global Macro News

ECB deposit rate sits at 2.00%, anchoring policy expectations for the four EU-member central banks in the region. Eurozone unemployment at 6.70% supports steady external demand for Polish and Czech exports. Surging US gas prices are rekindling global inflation concerns with direct pass-through to Turkish and Hungarian CPI.

Saudi Arabia's projected 6.8% growth in 2027 offers indirect commodity tailwinds for Turkey. Japan's commitment to defend the yen via economic strengthening highlights potential FX intervention parallels. <i>↓ p.2</i>