Emerging Europe Macro Daily(Beta Mode)

CBRT Holds at 37%, Polish Equities Advance

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| BIST 100 | 13,743.50 | -0.01% |

| iShares Poland | 39.61 | +1.80% |

| EUR/PLN | 4.25 | -0.05% |

| EUR/HUF | 353.27 | -0.33% |

| EUR/CZK | 24.15 | -0.13% |

| USD/TRY | 46.25 | +0.21% |

| Brent Crude | 88.56 | -2.01% |

| Gold | 4,208.00 | +2.88% |

| Bitcoin | 63,395.68 | +3.17% |

| Poland 10Y Govt Yield | 5.58% | +0.00% |

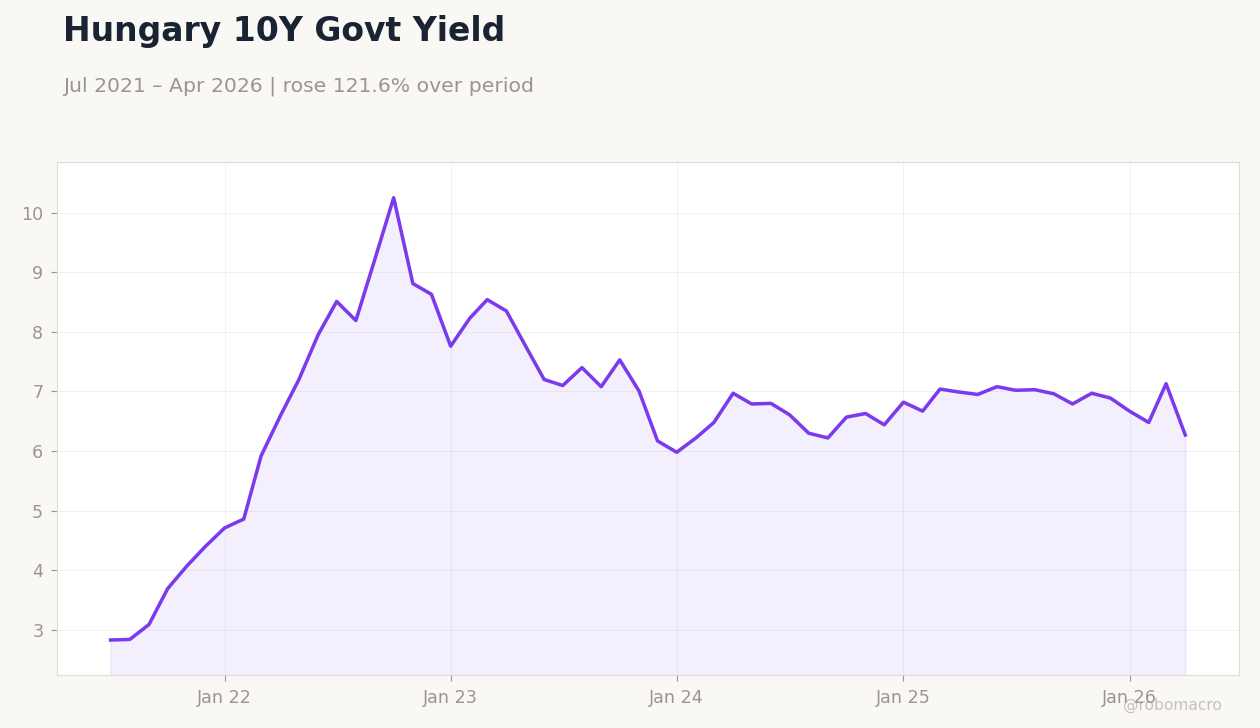

| Hungary 10Y Govt Yield | 6.27% | -12.06% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| TCMB Interest Rate Decision | 37 | 37 | 37 |

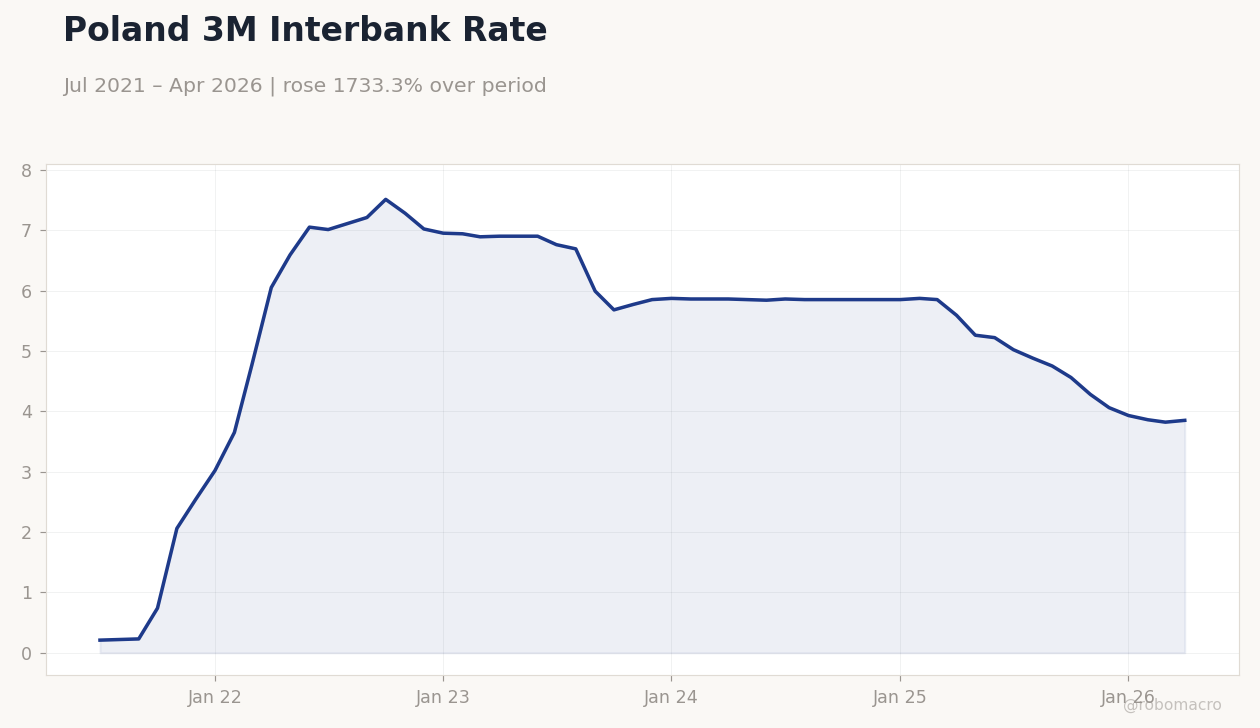

Poland 3M Interbank Rate | Type: macro_line | Rate %: 3.85 (2026-04-01) | Range: 0.21–7.51 | Trend(6pt): 0.21,7.21,5.77,5.85,3.82,3.85

Poland 3M Interbank Rate | Type: macro_line | Rate %: 3.85 (2026-04-01) | Range: 0.21–7.51 | Trend(6pt): 0.21,7.21,5.77,5.85,3.82,3.85

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- CBRT kept the policy rate at 37% as inflation pressures persist in Turkey.

- Polish equities rose 1.80% while regional FX showed modest EUR strength against CEE currencies.

- Hungary 10-year yields fell 12.06% amid thin trading and ECB policy backdrop.

Yesterday's Recap

Turkey’s central bank held the benchmark rate at 37%, matching consensus and leaving the real policy rate deeply negative given elevated inflation. BIST 100 closed virtually unchanged at 13,743.50. In Poland, iShares Poland gained 1.80% to 39.61 as EUR/PLN eased 0.05% to 4.25.

Hungary’s 10-year government yield dropped sharply to 6.27%, while EUR/HUF fell 0.33% to 353.27. Czech and Romanian markets saw limited moves, with EUR/CZK declining 0.13% to 24.15. Brent crude fell 2.01% to 88.56, providing modest relief to energy-importing economies across the region.

Gold and Bitcoin posted gains of 2.88% and 3.17%, respectively, reflecting broader risk-on sentiment.

The Day Ahead

The calendar is empty of major data releases across Poland, Czech Republic, Hungary, Romania and Turkey. Markets will monitor any follow-up comments from CBRT Governor after yesterday’s hold decision. Polish energy-price discussions among four ministries may generate domestic headlines but lack immediate market impact.

Regional FX will remain sensitive to ECB rhetoric and any updates on EU cohesion-fund disbursements. Investors are likely to focus on external drivers such as Brent crude and global risk appetite until next week’s releases.

Other Economic Notes

Poland continues to weigh its stance on EU budget streams linked to CO2 pricing, potentially affecting future fiscal flows. Energy-cost containment remains a priority for Warsaw as ministries coordinate new measures. Hungary’s tighter foreign-labor rules threaten planned industrial investment, adding downside risk to medium-term growth.

Romania’s euro-adoption timeline stays aspirational amid still-elevated inflation. All five economies retain structural exposure to energy-import costs despite recent Brent weakness.

Global Macro News

The ECB deposit rate stood at 2.00%. Euro-area unemployment stood at 6.70%, supporting a gradual rather than aggressive ECB path. IMF warnings on Middle East energy risks underscore shared vulnerabilities for gas-dependent CEE economies.

<i>↓ p.2</i>