Emerging Europe Macro Daily(Beta Mode)

CNB Hike Odds Rise as Poland Trade Gap Widens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| BIST 100 | 13,938.50 | +1.42% |

| iShares Poland | 40.95 | +0.96% |

| EUR/PLN | 4.24 | -0.18% |

| EUR/HUF | 350.66 | -0.43% |

| EUR/CZK | 24.12 | -0.11% |

| USD/TRY | 46.27 | +0.07% |

| Brent Crude | 83.49 | -4.40% |

| Gold | 4,328.60 | +2.70% |

| Bitcoin | 65,718.06 | +2.01% |

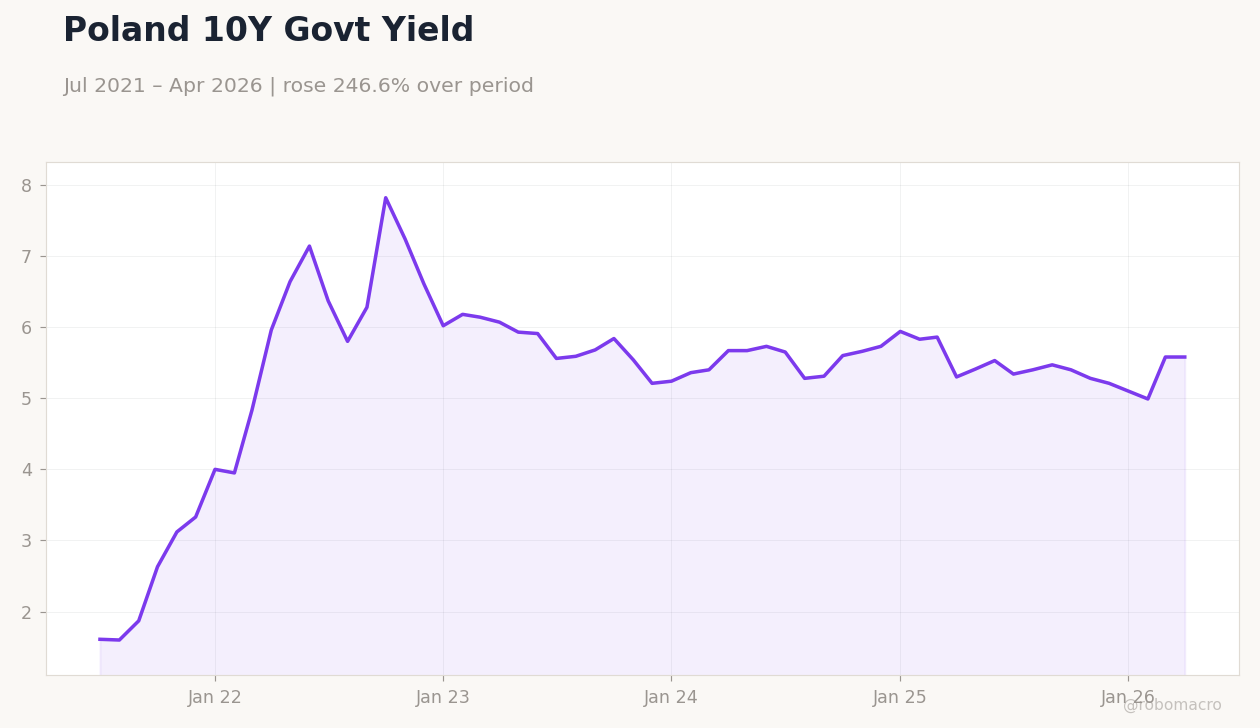

| Poland 10Y Govt Yield | 5.58% | +0.00% |

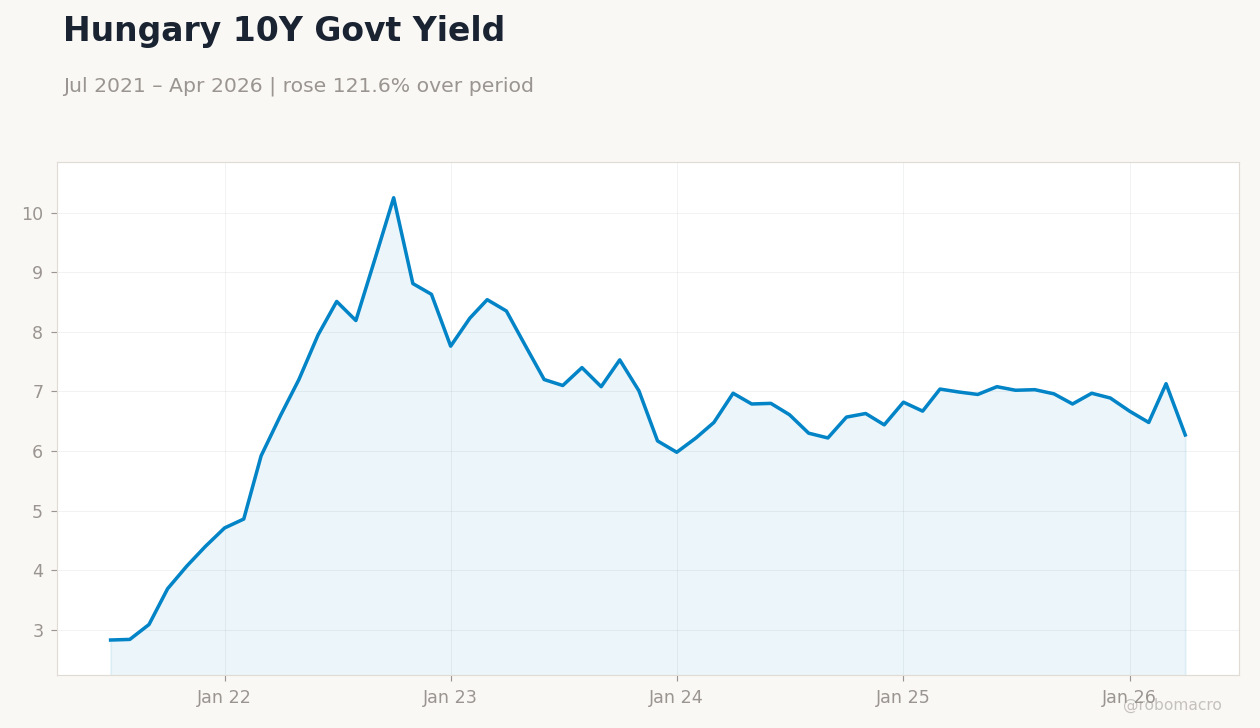

| Hungary 10Y Govt Yield | 6.27% | -12.06% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

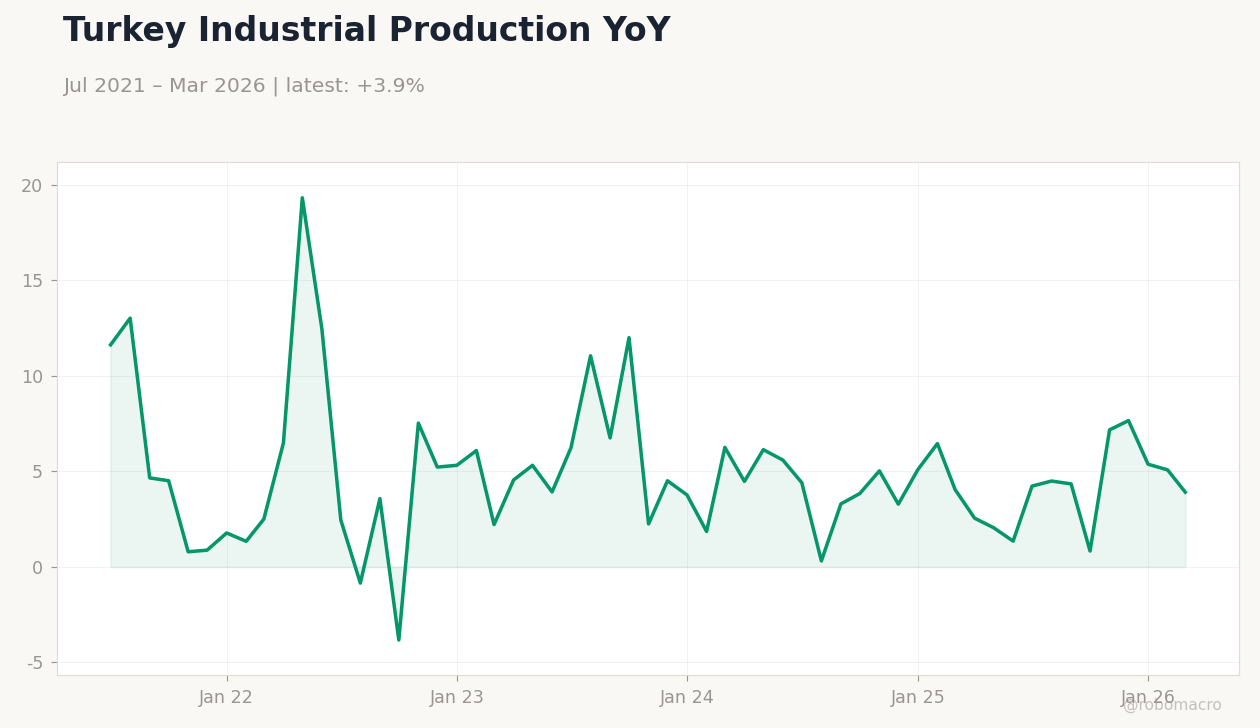

| Industrial Production Year-over-Year | -1.10 | - | - |

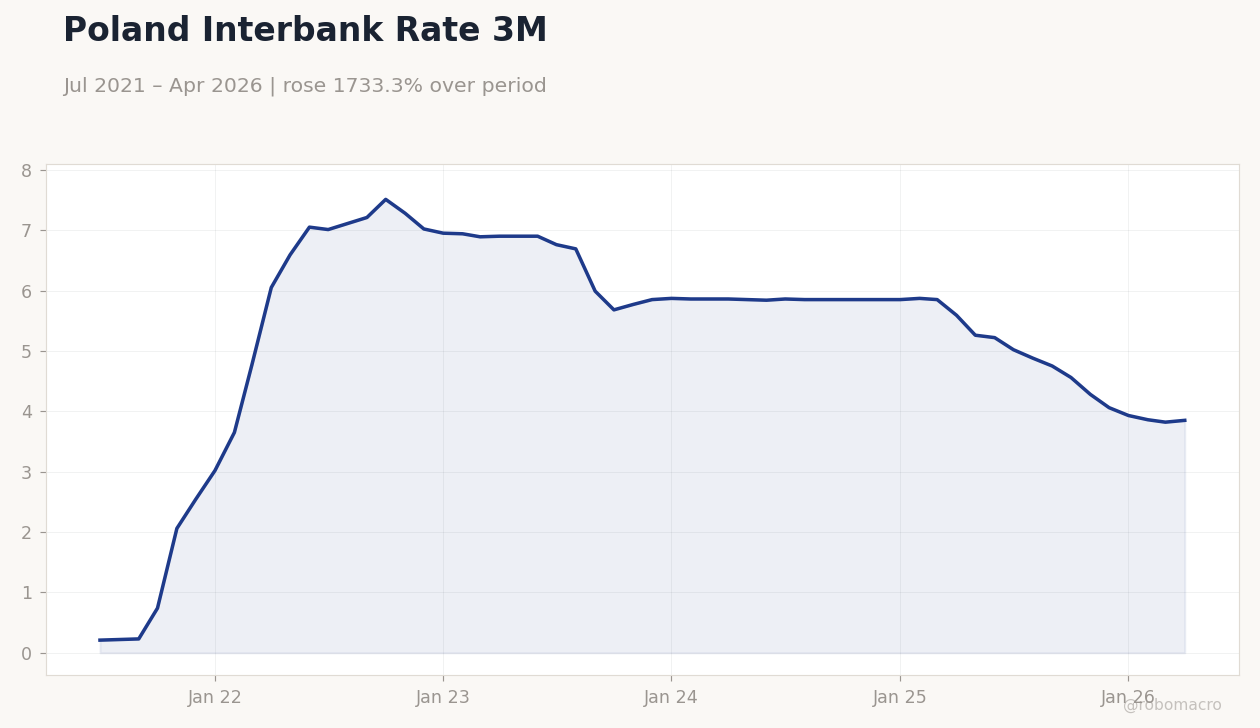

Poland Interbank Rate 3M | Type: macro_line | Rate %: 3.85 (2026-04-01) | Range: 0.21–7.51 | Trend(6pt): 0.21,7.21,5.77,5.85,3.82,3.85

Poland Interbank Rate 3M | Type: macro_line | Rate %: 3.85 (2026-04-01) | Range: 0.21–7.51 | Trend(6pt): 0.21,7.21,5.77,5.85,3.82,3.85

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Business Confidence Index | 103.30 | - | 23:00 |

- Czech Governor Michl strengthened the case for a June rate hike amid rising inflation risks.

- Poland posted a PLN 6.6 bn current account deficit in April, extending the negative streak.

- Turkish industrial production remained weak while BIST 100 gained 1.42% on lira stability.

Yesterday's Recap

Turkey released April industrial production data showing persistent contraction, with the year-over-year reading at -1.1%. Poland’s April current account balance swung to a PLN 6.6 bn deficit, driven by goods trade weakness, while the zloty firmed modestly to 4.24 versus the euro. Hungarian 10-year yields fell sharply to 6.27% as investors priced limited near-term policy easing.

The BIST 100 rose 1.42% to 13,938.50, supported by USD/TRY stability near 46.27. Brent crude dropped 4.40% to 83.49, easing energy import costs for the region. Gold advanced 2.70% to 4,328.60, reflecting broader safe-haven demand.

Czech and Romanian data releases were absent, leaving markets focused on external drivers. Poland’s pension funds delivered the highest real returns among OECD peers in 2025 at 31.2%, bolstering household balance sheets.

The Day Ahead

Turkey will publish its June Business Confidence Index, with the prior reading at 103.30; any downside surprise could reinforce CBRT caution on policy. No major releases are scheduled for Poland, Hungary, Czech Republic or Romania. Markets will monitor ECB speakers for signals on the 2.00% deposit rate path and potential spillovers to regional FX.

Regional equity flows may respond to any updates on EU Recovery Fund disbursements to Poland.

Other Economic Notes

Hungary’s weak industrial output and soft retail sales continue to weigh on growth prospects despite contained inflation. Regional energy import dependence remains a shared vulnerability, with Brent’s sharp decline providing modest relief to current account pressures across the EU-5. Moldova has entered the top 10 wine suppliers to Poland, adding a positive note to bilateral trade.

Global Macro News

The ECB raised its deposit rate to 2.00%, marking the first hike in three years and prompting regional central banks to reassess timing. Eurozone unemployment stood at 6.70%, supporting a gradual policy normalization narrative. Stronger US data and elevated gold prices added to external volatility for CEE currencies.

Global equity sentiment improved, lifting Bitcoin 2.01% and supporting risk assets in Turkey and Poland. <i>↓ p.2</i>