Emerging Europe Macro Daily(Beta Mode)

Turkey IP Rebounds, BIST Climbs as Yields Diverge

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| BIST 100 | 13,938.50 | +1.42% |

| iShares Poland | 40.95 | +0.96% |

| EUR/PLN | 4.25 | +0.23% |

| EUR/HUF | 350.05 | -0.06% |

| EUR/CZK | 24.15 | +0.12% |

| USD/TRY | 46.29 | +0.07% |

| Brent Crude | 82.71 | -0.55% |

| Gold | 4,340.00 | +0.28% |

| Bitcoin | 66,206.08 | +0.75% |

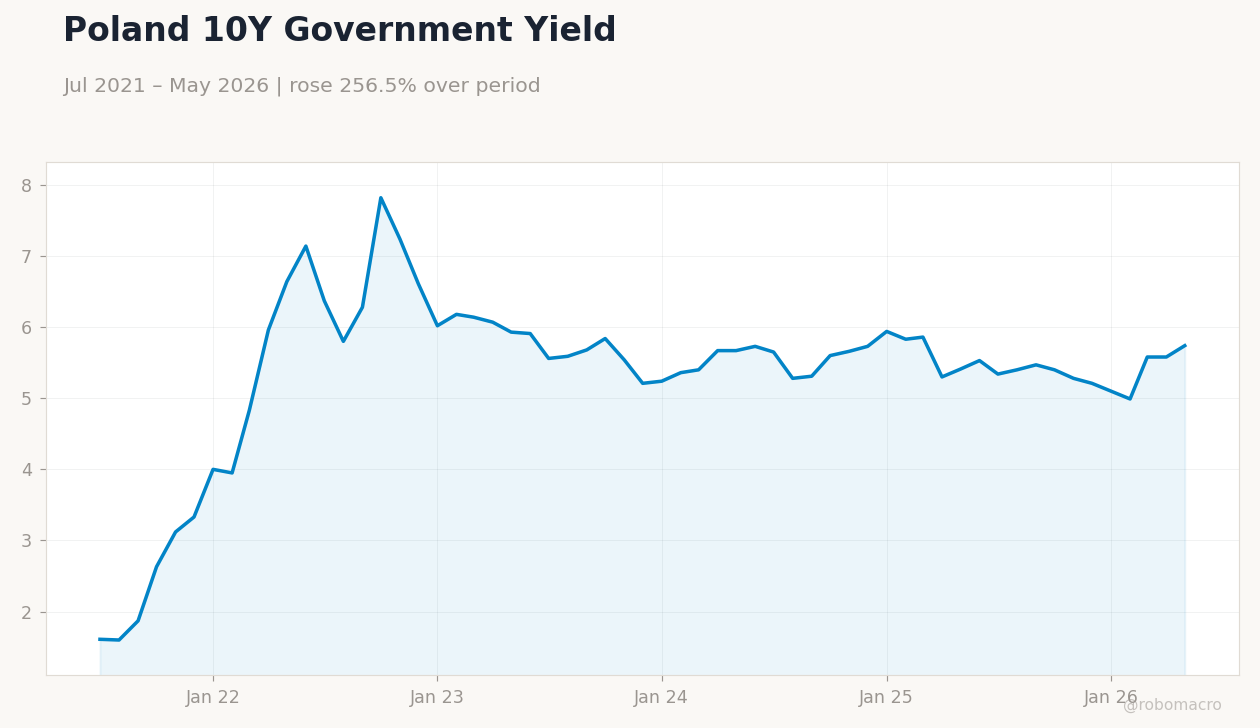

| Poland 10Y Govt Yield | 5.74% | +2.87% |

| Hungary 10Y Govt Yield | 5.65% | -9.89% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Industrial Production Year-over-Year | -1.10 | - | 6 |

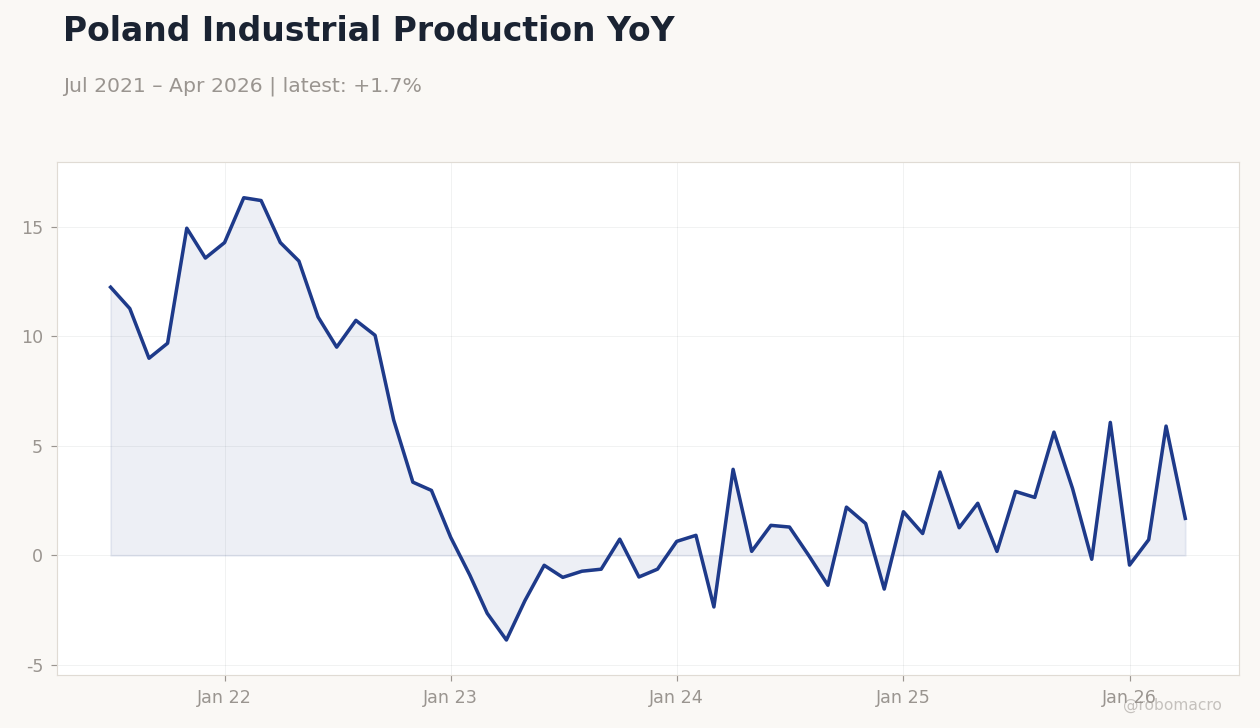

Poland Industrial Production YoY | Type: macro_line | YoY %: 1.689 (2026-04-01) | Range: -3.867–16.33 | Trend(6pt): 12.25,10.05,-0.9883,1.993,5.903,1.689

Poland Industrial Production YoY | Type: macro_line | YoY %: 1.689 (2026-04-01) | Range: -3.867–16.33 | Trend(6pt): 12.25,10.05,-0.9883,1.993,5.903,1.689

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Business Confidence Index | 103.30 | - | 23:00 |

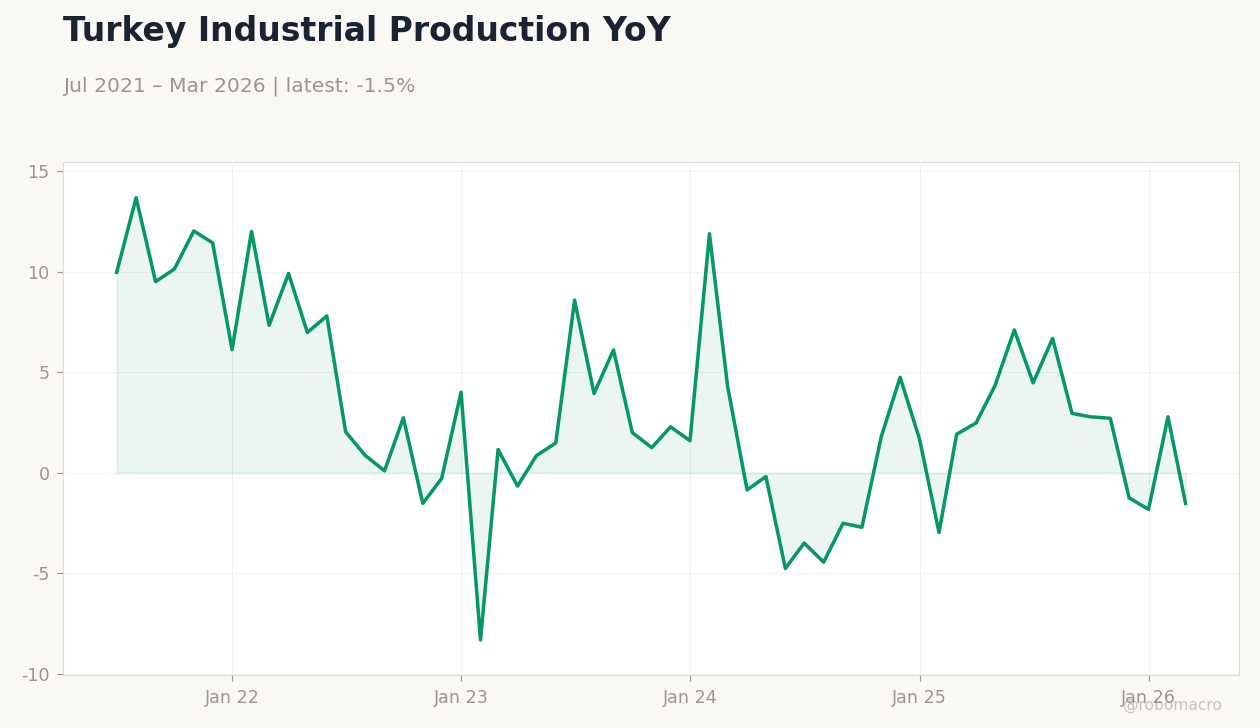

- Turkey industrial production jumped to 6% y/y in May, reversing the prior contraction and lifting BIST 100 by 1.42%.

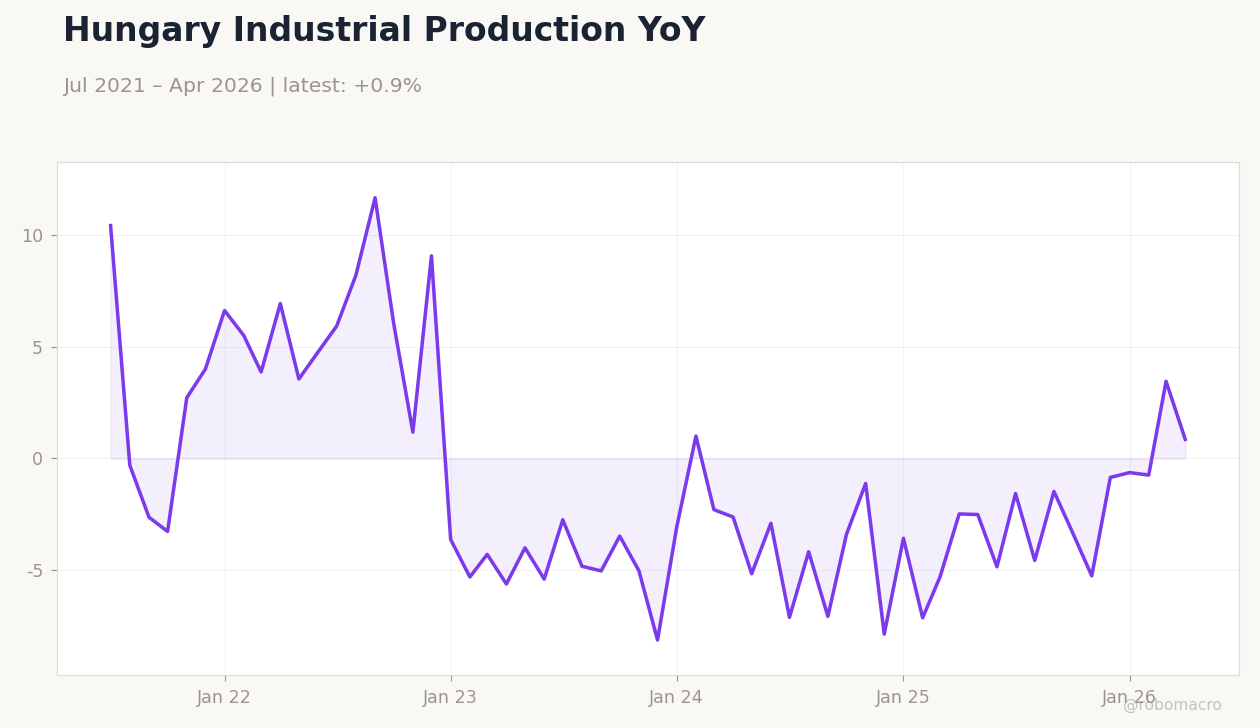

- Regional FX showed modest EUR strength against PLN and CZK while HUF held steady; Hungary 10Y yields fell nearly 10 bp.

- ECB deposit rate at 2.00% and euro-area unemployment at 6.70% set a stable external backdrop for CEE central banks.

Yesterday's Recap

Turkey reported a sharp rebound in industrial production, rising 6% y/y after contracting 1.1% previously, signaling improved manufacturing momentum ahead of the June business confidence print. The BIST 100 advanced 1.42% to 13,938.50 while iShares Poland gained 0.96%. EUR/PLN edged 0.23% higher to 4.25 and EUR/CZK rose 0.12% to 24.15, whereas EUR/HUF eased 0.06% to 350.05.

USD/TRY ticked up 0.07% to 46.29. Poland’s 10Y yield climbed 2.87% to 5.74% while Hungary’s 10Y yield dropped 9.89% to 5.65%. Brent crude fell 0.55% to 82.71 amid softer global energy demand.

Gold and Bitcoin posted modest gains of 0.28% and 0.75%.

The Day Ahead

Markets will focus on Turkey’s Business Confidence Index release tonight, with the prior reading at 103.30. No other high-impact data are scheduled for Poland, Czech Republic, Hungary or Romania. Traders will monitor any follow-through from yesterday’s Turkish industrial production strength into equity and FX flows.

Regional central banks remain in data-dependent mode ahead of next week’s inflation prints.

Other Economic Notes

Poland continues to attract US defense commitments under the SAFE program, supporting fiscal inflows and zloty stability. Czech authorities moved to replace public-media license fees with direct budget funding, a step that may ease fiscal pressures but leaves monetary policy focused on inflation convergence. Romania and Poland maintain steady EU fund absorption trajectories, underpinning medium-term growth outlooks.

Global Macro News

The ECB deposit rate stands at 2.00%, providing a clear anchor for CNB and MNB policy expectations. Euro-area unemployment at 6.70% signals contained labor-market slack that limits imported disinflation pressures on CEE economies. Subsidized Chinese exports remain a G7 concern, raising the risk of renewed trade frictions that could affect Polish and Czech manufacturing supply chains.

Australia’s central bank held rates at 4.35%, echoing the cautious stance seen across CEE non-euro central banks. Bank of Japan’s latest hike to a 31-year high widened global yield differentials, supporting selective inflows into higher-yielding Hungarian and Polish paper. <i>↓ p.2</i>