Emerging Europe Macro Daily(Beta Mode)

Turkey IP Surges, Polish Equities Advance

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| BIST 100 | 14,493.10 | +0.32% |

| iShares Poland | 40.69 | +1.95% |

| EUR/PLN | 4.24 | -0.26% |

| EUR/HUF | 350.06 | -0.06% |

| EUR/CZK | 24.16 | +0.17% |

| USD/TRY | 46.31 | +0.06% |

| Brent Crude | 78.20 | -0.96% |

| Gold | 4,347.90 | +0.39% |

| Bitcoin | 65,554.90 | -0.07% |

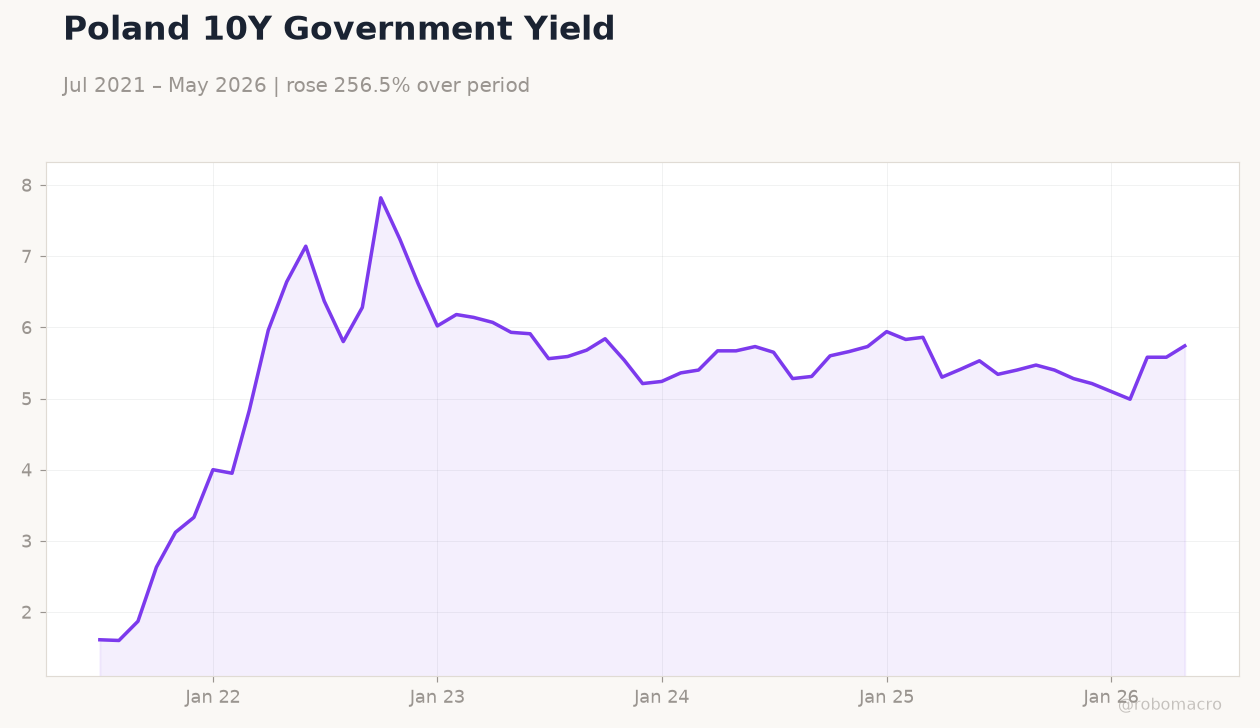

| Poland 10Y Govt Yield | 5.74% | +2.87% |

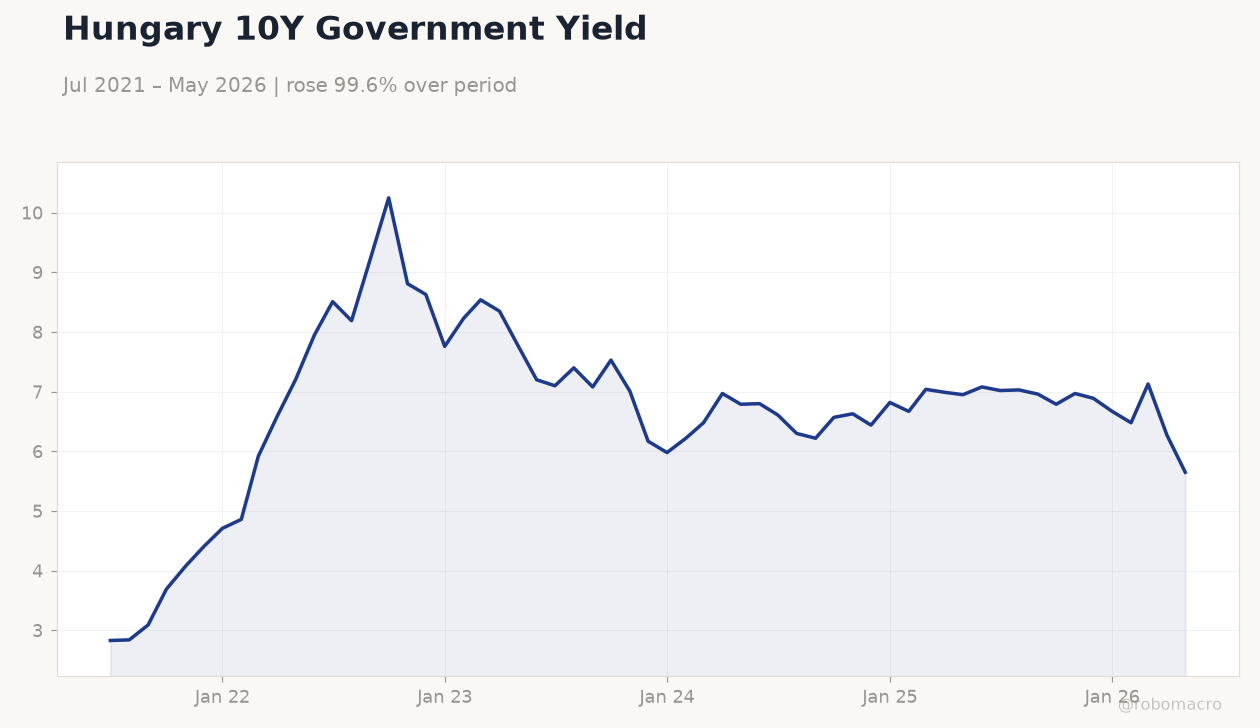

| Hungary 10Y Govt Yield | 5.65% | -9.89% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

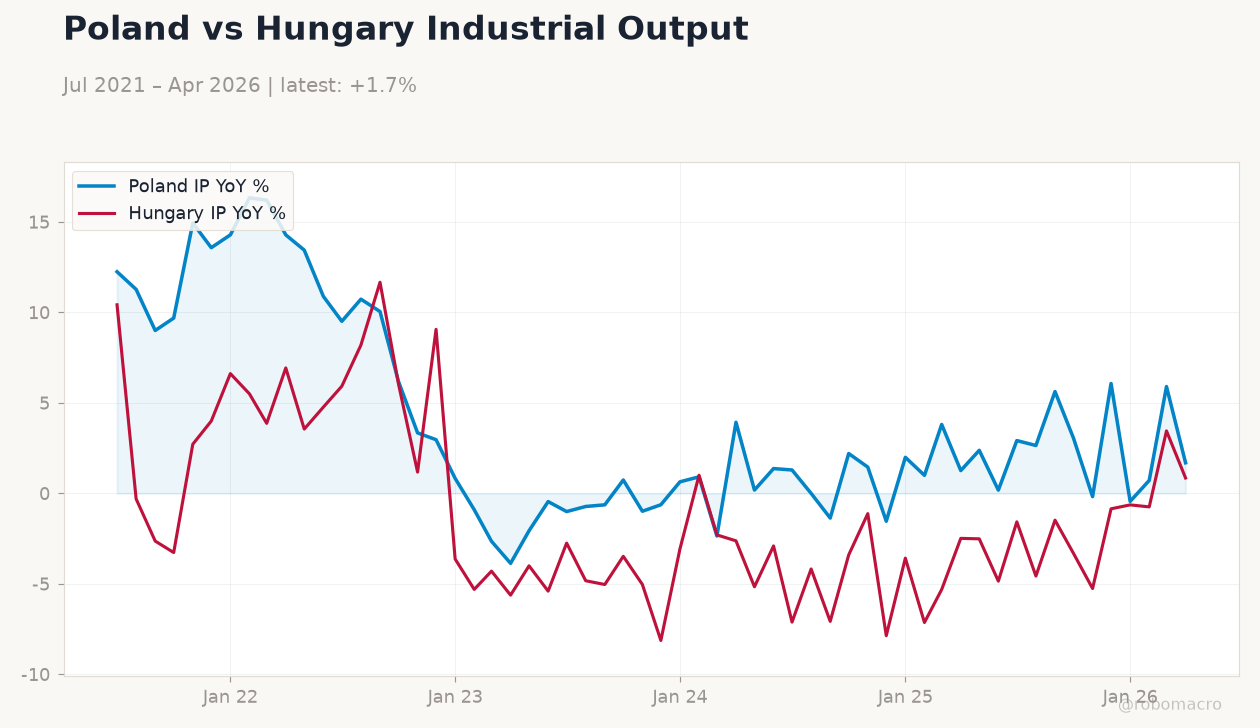

| Industrial Production Year-over-Year | -1.10 | - | 6 |

Hungary 10Y Government Yield | Type: macro_line | 10Y Yield %: 5.65 (2026-05-01) | Range: 2.83–10.25 | Trend(6pt): 2.83,9.23,7.01,6.82,7.13,5.65

Hungary 10Y Government Yield | Type: macro_line | 10Y Yield %: 5.65 (2026-05-01) | Range: 2.83–10.25 | Trend(6pt): 2.83,9.23,7.01,6.82,7.13,5.65

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Business Confidence Index | 103.30 | - | 23:00 |

- Turkey industrial production rose 6% y/y in May, sharply reversing the prior contraction and supporting lira stability.

- Polish equities outperformed with iShares Poland gaining 1.95% as World Bank lending exit lifted sentiment.

- Regional FX showed modest zloty strength while Hungary yields fell nearly 10 bp on thin buying.

Yesterday's Recap

Turkey released May industrial production at +6.0% y/y, a strong rebound from the -1.1% print and a clear positive surprise for manufacturing. The data reinforced resilience in the export-oriented sectors despite elevated borrowing costs. In Poland, equities advanced notably with the iShares Poland ETF rising 1.95% to 40.69 amid news that Warsaw will exit the World Bank lending program.

EUR/PLN eased 0.26% to 4.24 while Poland’s 10-year yield rose 2.87% to 5.74%. Hungary 10-year yields dropped 9.89% to 5.65% on light foreign inflows. BIST 100 closed 0.32% higher at 14,493.10 as USD/TRY held near 46.31.

Broader news of a new Germany-Poland defense agreement added to constructive regional tone.

The Day Ahead

Turkey’s Business Confidence Index for June is due tonight and will be watched for any follow-through from the industrial production beat. No major data releases are scheduled for Poland, Czechia, Hungary or Romania. Markets will monitor ECB speakers for any hints on the 2.00% deposit rate path.

Regional equity flows may stay light ahead of month-end positioning. FX traders will focus on EUR crosses given mixed global risk signals.

Other Economic Notes

Poland’s exit from World Bank lending marks a structural shift reflecting sustained income convergence and stronger domestic capital markets. Hungary continues to face pressure from elevated food import dependence, which complicates inflation control. Energy import reliance remains a common vulnerability across the EU-4 economies, keeping external balances sensitive to Brent moves near $78.20.

The proposed Polish “Copper Valley” initiative could support medium-term export diversification if new mining projects advance.

Global Macro News

Eurozone growth momentum stayed resilient according to latest PMI readings, supporting demand for CEE exports. The Fed’s likely near-term easing path, highlighted by recent analyst commentary, eased pressure on EM currencies including the zloty and forint. UK inflation held at 2.8% while Australia kept rates unchanged at 4.35%, underscoring divergent developed-market policy cycles.

<i>↓ p.2</i>