Emerging Europe Macro Daily(Beta Mode)

Turkey IP Rebounds as Polish Yields Rise

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| BIST 100 | 14,454.31 | +0.23% |

| iShares Poland | 40.23 | -1.13% |

| EUR/PLN | 4.25 | +0.32% |

| EUR/HUF | 350.75 | +0.66% |

| EUR/CZK | 24.15 | +0.07% |

| USD/TRY | 46.44 | +0.29% |

| Brent Crude | 77.71 | -2.31% |

| Gold | 4,324.90 | -0.78% |

| Bitcoin | 63,940.00 | -2.53% |

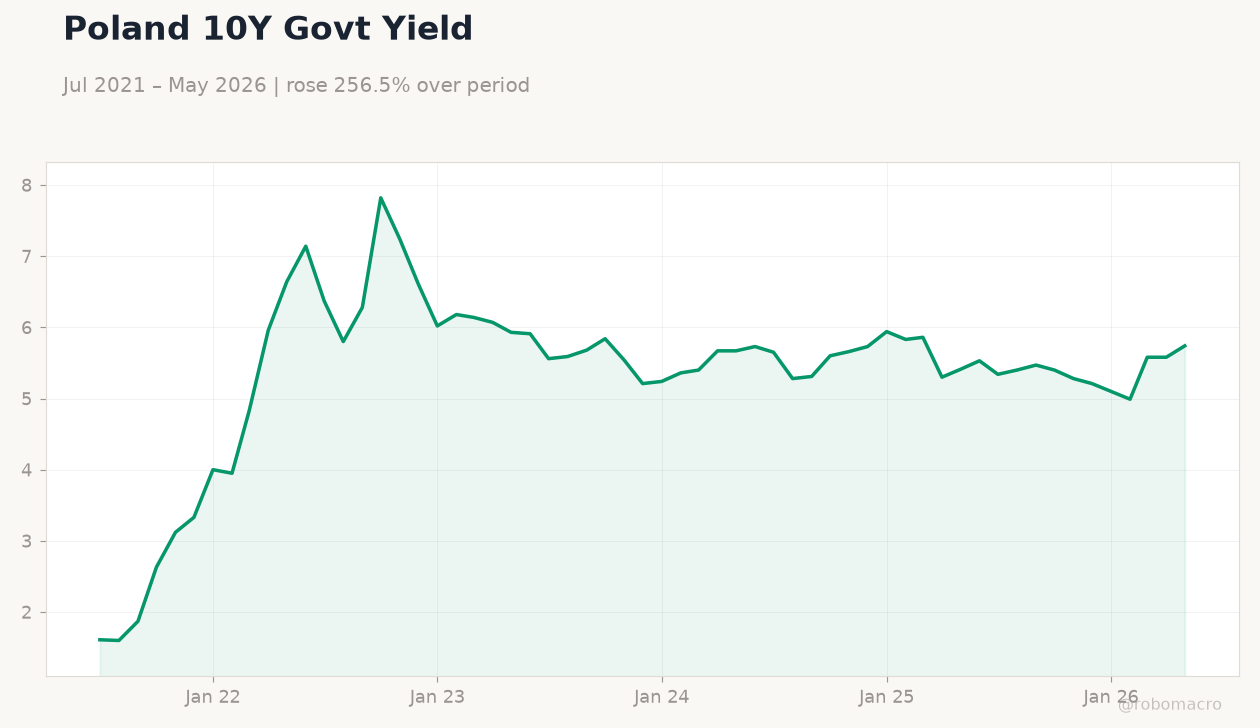

| Poland 10Y Govt Yield | 5.74% | +2.87% |

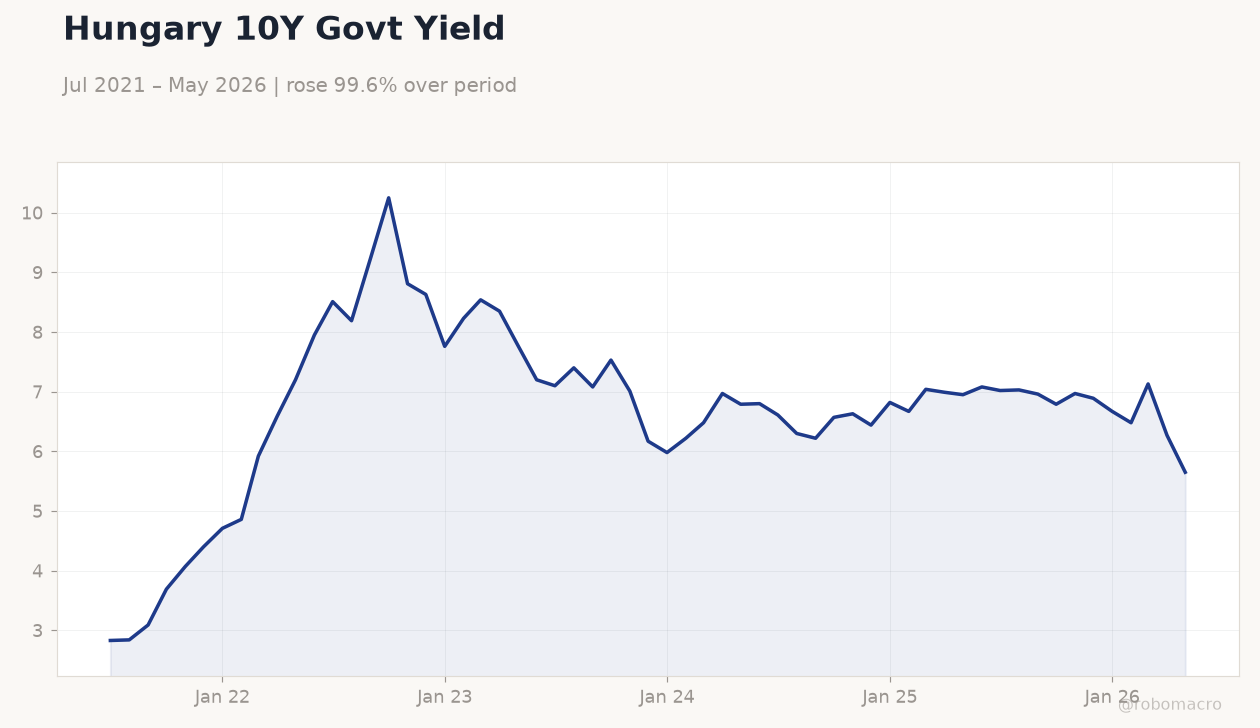

| Hungary 10Y Govt Yield | 5.65% | -9.89% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

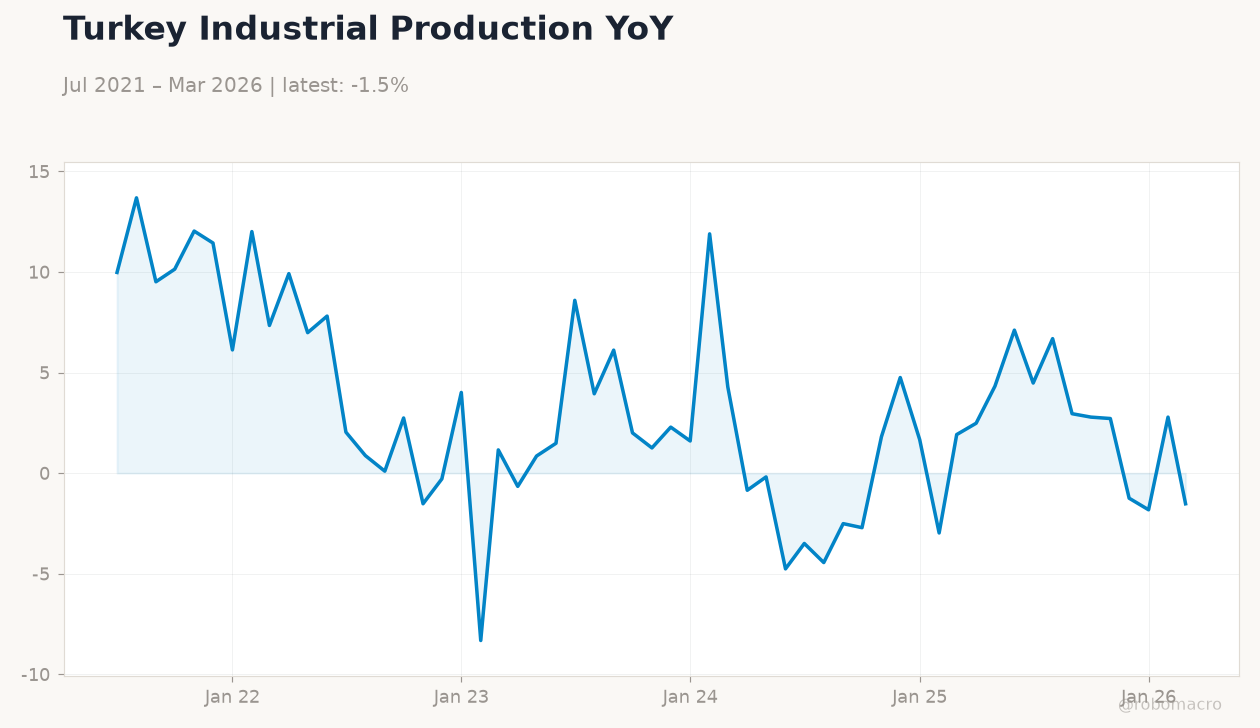

| Industrial Production Year-over-Year | -1.10 | - | 6 |

Hungary 10Y Govt Yield | Type: macro_line | Yield %: 5.65 (2026-05-01) | Range: 2.83–10.25 | Trend(6pt): 2.83,9.23,7.01,6.82,7.13,5.65

Hungary 10Y Govt Yield | Type: macro_line | Yield %: 5.65 (2026-05-01) | Range: 2.83–10.25 | Trend(6pt): 2.83,9.23,7.01,6.82,7.13,5.65

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Business Confidence Index | 103.30 | - | 23:00 |

| Friday (2026-06-19) | |||

| Business Confidence Index | 103.30 | - | 23:00 |

- Turkey industrial production jumped to 6% y/y in May from -1.1% prior, signalling manufacturing recovery.

- Polish assets underperformed with iShares Poland falling 1.13% and 10-year yields rising 2.87% to 5.74%.

- Hungary 10-year yields dropped 9.89% to 5.65% amid forint strength, while BIST 100 gained 0.23%.

Yesterday's Recap

Turkey released May industrial production at 6% y/y, a sharp turnaround from the prior contraction and the only major data point across the region. Polish equities and bonds sold off, with the iShares Poland ETF declining 1.13% and the 10-year government yield climbing to 5.74%. EUR/PLN rose 0.32% to 4.25 while EUR/HUF advanced 0.66% to 350.75.

Hungary’s 10-year yield fell sharply to 5.65% on improved sentiment. Brent crude dropped 2.31% to 77.71, weighing on energy importers. News flow highlighted Poland’s defence agreement with Germany and its planned exit from the World Bank lending programme after sustained growth.

Czech and Romanian markets remained quiet with no fresh macro releases.

The Day Ahead

Turkey’s Business Confidence Index is scheduled for release tonight, with markets watching for any shift from the prior 103.30 reading. No other high-impact data are due from Poland, Czech Republic, Hungary or Romania. Regional FX desks will monitor EUR/TRY and USD/TRY flows ahead of the weekend.

ECB speakers may comment on the 2.25% deposit rate path, influencing CNB and MNB positioning. Investors will also track any updates on Poland’s remaining EU cohesion fund disbursements.

Other Economic Notes

Poland’s exit from World Bank lending reflects decades of convergence and rising per-capita income, reducing its reliance on multilateral support. Hungary continues to benefit from EU Recovery and Resilience Facility tranche releases after meeting rule-of-law milestones, supporting fiscal buffers. Energy import dependence remains a shared vulnerability for all five economies, with Brent’s decline offering modest relief to current-account balances.

Czech inflation pressures have prompted discussion of the first CNB rate hike since 2022.

Global Macro News

The US FOMC meeting today keeps markets focused on any signals that could affect dollar funding costs for Emerging Europe banks. Eurozone unemployment stood at 6.70%, providing a stable external demand backdrop for Polish and Czech exporters. <i>↓ p.2</i>