Emerging Europe Macro Daily(Beta Mode)

Turkey IP Rebounds, BIST Rises as CEE FX Weakens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| BIST 100 | 14,827.40 | +2.82% |

| iShares Poland | 39.86 | -0.92% |

| EUR/PLN | 4.26 | +0.47% |

| EUR/HUF | 353.16 | +0.70% |

| EUR/CZK | 24.21 | +0.36% |

| USD/TRY | 46.44 | +0.01% |

| Brent Crude | 80.29 | +0.55% |

| Gold | 4,163.00 | -1.45% |

| Bitcoin | 62,828.58 | -0.11% |

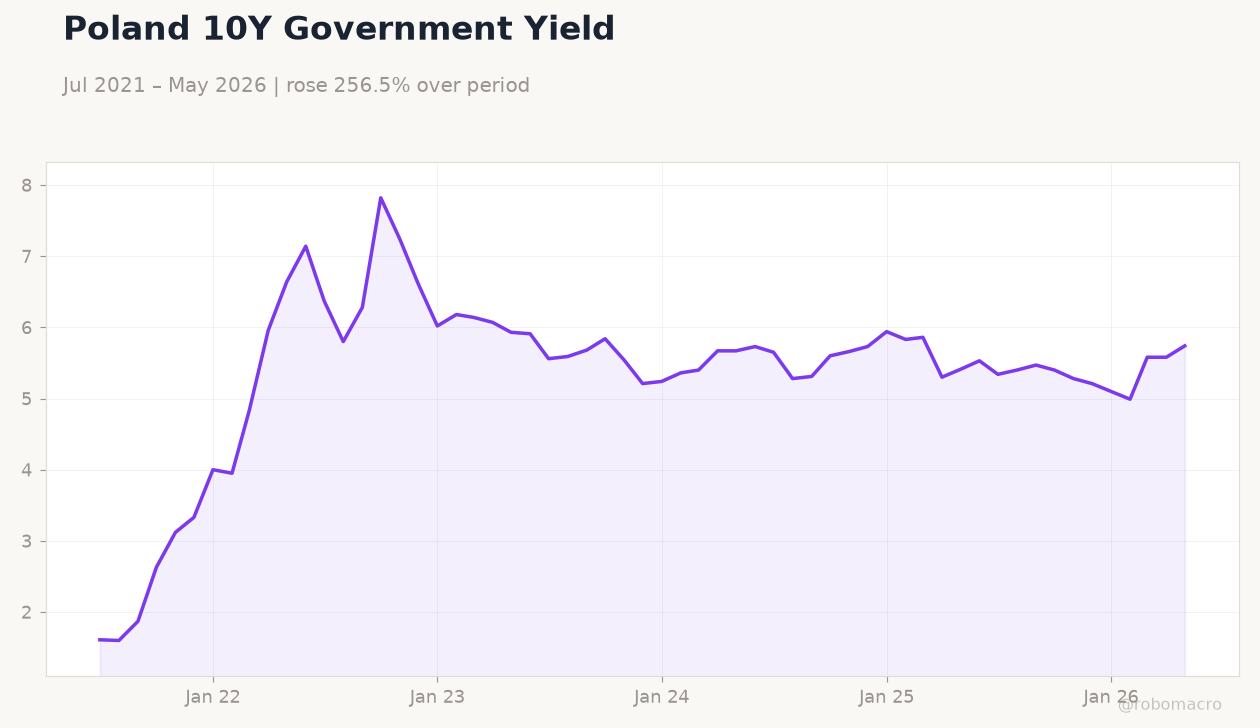

| Poland 10Y Govt Yield | 5.74% | +2.87% |

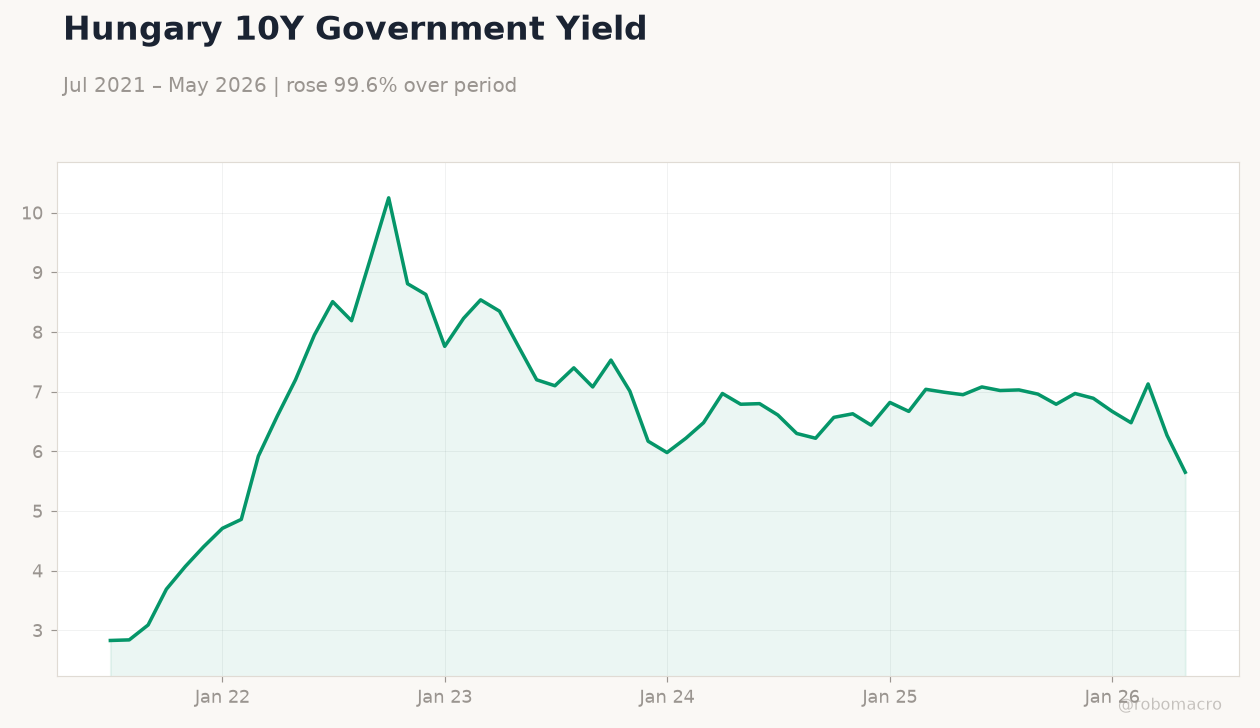

| Hungary 10Y Govt Yield | 5.65% | -9.89% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

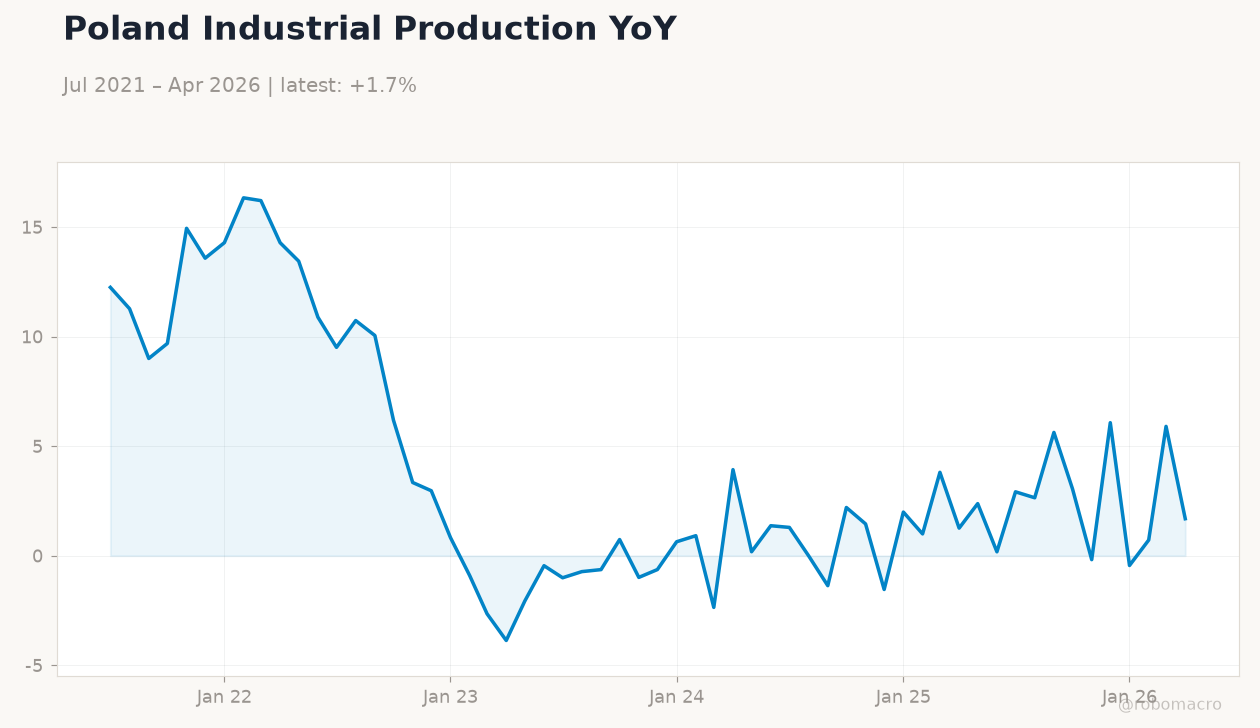

| Industrial Production Year-over-Year | -1.10 | - | 6 |

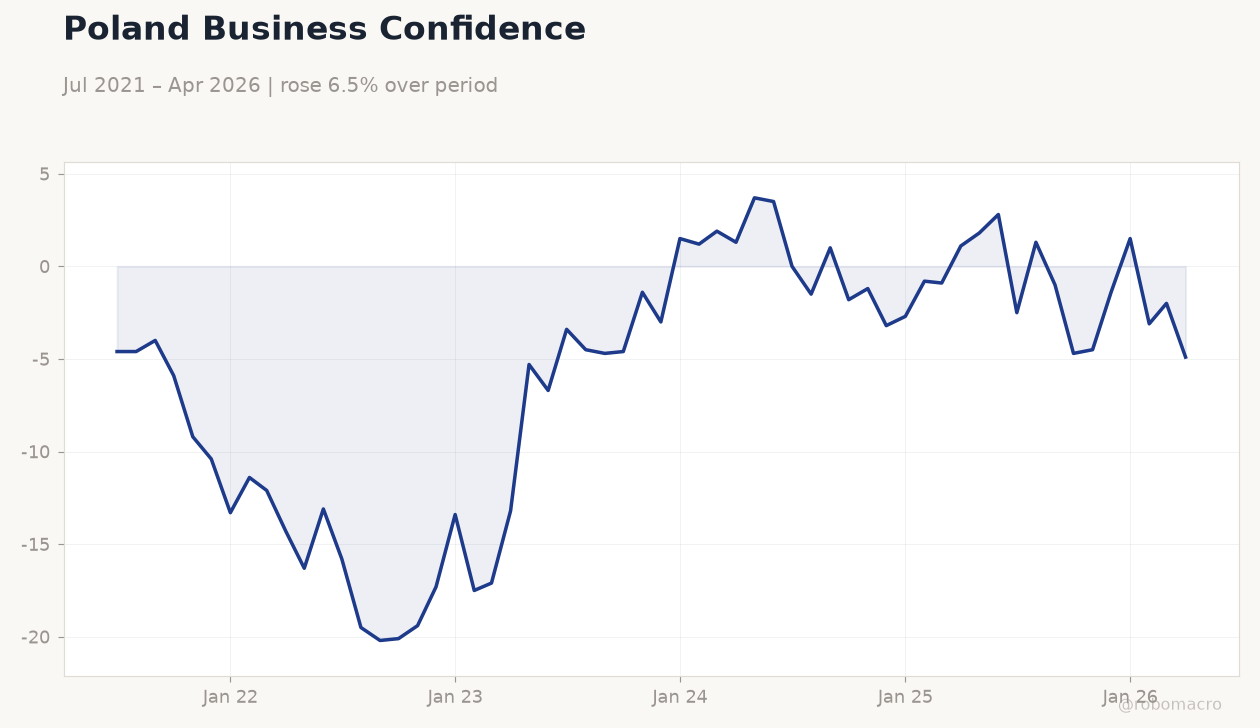

Poland Business Confidence | Type: macro_line | Index: -4.9 (2026-04-01) | Range: -20.2–3.7 | Trend(6pt): -4.6,-20.2,-1.4,-2.7,-2,-4.9

Poland Business Confidence | Type: macro_line | Index: -4.9 (2026-04-01) | Range: -20.2–3.7 | Trend(6pt): -4.6,-20.2,-1.4,-2.7,-2,-4.9

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Business Confidence Index | 103.30 | - | 23:00 |

- Turkey industrial production jumped 6% y/y in May, reversing the prior -1.1% contraction.

- BIST 100 climbed 2.82% while Polish equities fell 0.92%; EUR/PLN rose to 4.26.

- CNB delivered its first rate hike in four years, diverging from dovish MNB and NBP stances.

Yesterday's Recap

Turkey’s May industrial production rebounded sharply to +6% y/y, signalling a recovery in manufacturing after last year’s contraction. The print lifted BIST 100 by 2.82% to 14,827.40, with investors pricing reduced downside risks to growth. In contrast, Polish equities fell 0.92% as EUR/PLN climbed 0.47% to 4.26 on hawkish Fed repricing.

Hungarian and Czech currencies also weakened modestly, with EUR/HUF up 0.70% and EUR/CZK up 0.36%. Poland 10-year yields rose 2.87% to 5.74% while Hungarian yields fell 9.89% to 5.65%, reflecting divergent fiscal and monetary outlooks. No major data emerged from Poland, Czech Republic, Hungary or Romania.

The Day Ahead

Markets will focus on Turkey’s June business confidence index, due tonight, for fresh signals on domestic demand. The reading follows yesterday’s strong industrial production print and will inform expectations for CBRT policy. Elsewhere in Emerging Europe, calendars remain light with no tier-1 releases scheduled in Poland, Czech Republic, Hungary or Romania.

Investors will monitor any follow-through from CNB’s surprise hike and its impact on regional FX. Thin volumes are likely ahead of the weekend.

Other Economic Notes

Poland secured further KPO energy-sector allocations totalling 67 billion zlotys, supporting fixed-income sentiment. World Bank’s new Poland strategy emphasises green transition and productivity gains amid concerns that the post-EU growth model may be fading. Hungary’s MNB began divesting Matolcsy-era properties at a loss, underscoring efforts to streamline central-bank balance-sheet optics.

Romania’s trade deficit narrowed last month, lending modest support to RON stability.

Global Macro News

The Fed’s hawkish tone strengthened the dollar and weighed on CEE currencies. ECB deposit rate stands at 2.25%, anchoring regional policy expectations. Eurozone unemployment remains at 6.70%, consistent with a soft-landing baseline that supports gradual ECB easing.

Yen weakness and renewed intervention bets in Japan have little direct spillover to Emerging Europe but highlight global FX volatility. <i>↓ p.2</i>