Emerging Europe Macro Daily(Beta Mode)

Poland's Gold Buys Lift Reserves as CEE Markets Dip

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| BIST 100 | 14,734.50 | -0.63% |

| iShares Poland | 39.86 | -0.92% |

| EUR/PLN | 4.26 | +0.09% |

| EUR/HUF | 351.61 | -0.01% |

| EUR/CZK | 24.18 | -0.02% |

| USD/TRY | 46.46 | +0.08% |

| Brent Crude | 78.96 | -1.11% |

| Gold | 4,214.40 | -0.23% |

| Bitcoin | 64,087.97 | -0.24% |

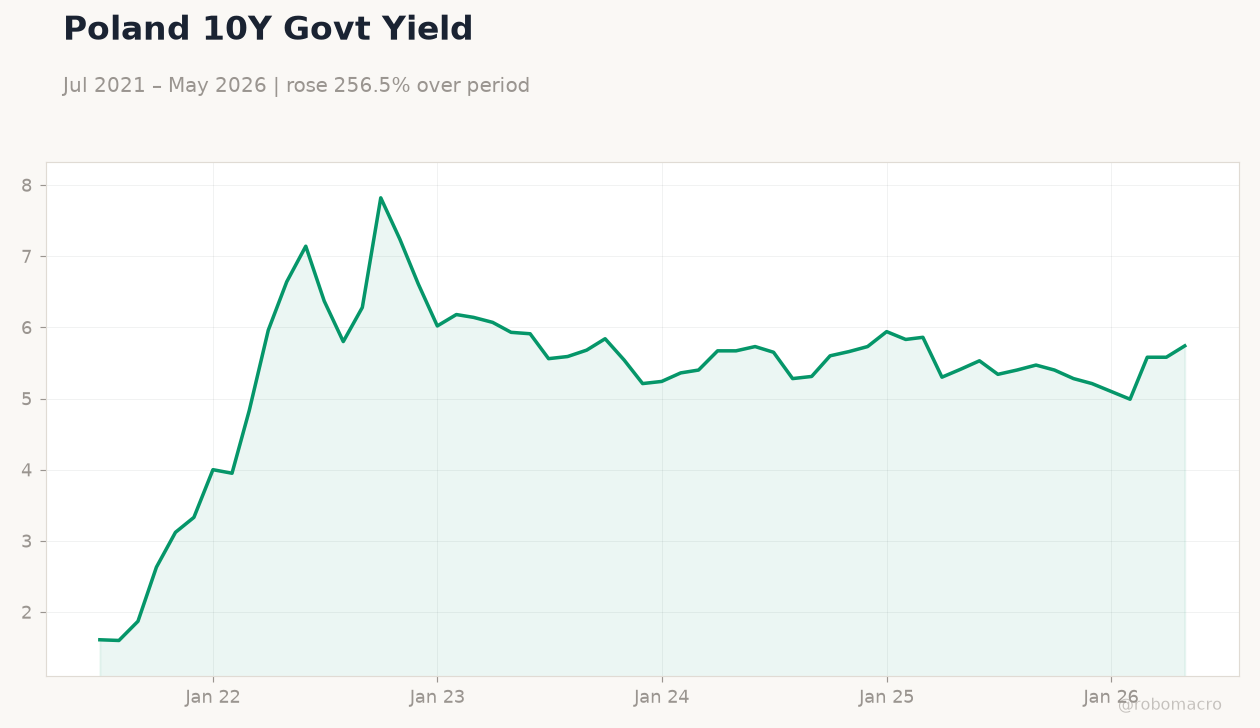

| Poland 10Y Govt Yield | 5.74% | +2.87% |

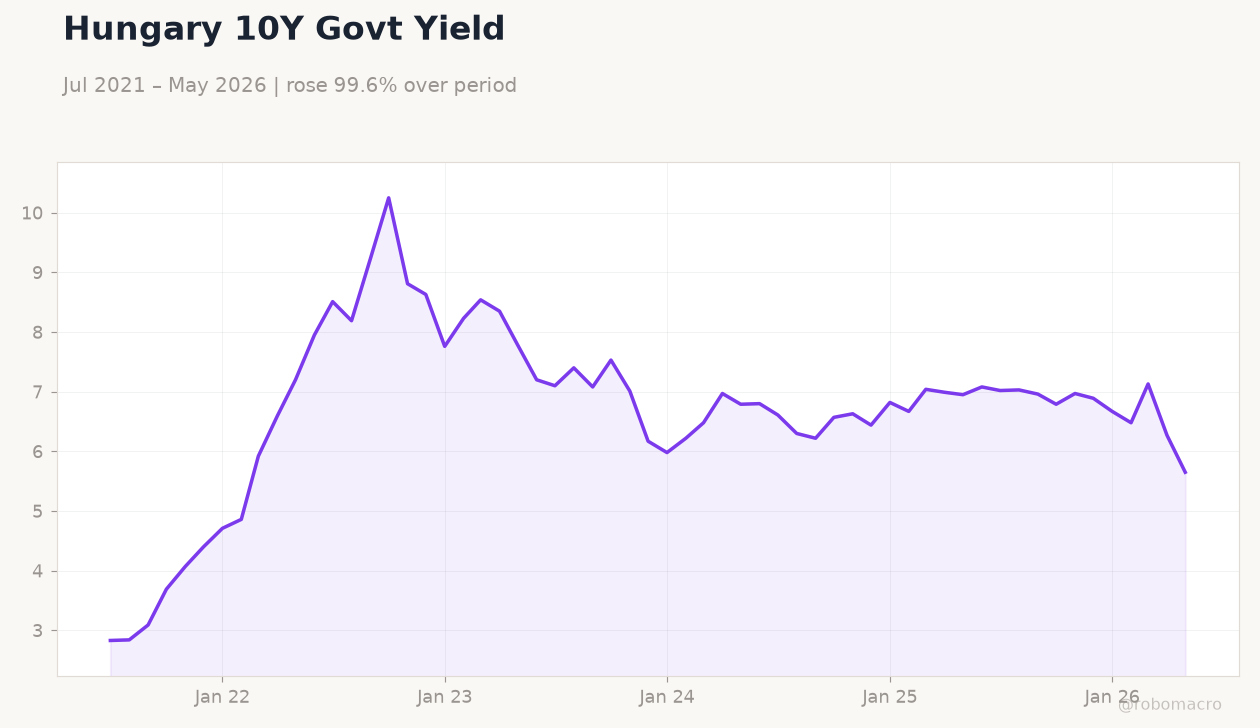

| Hungary 10Y Govt Yield | 5.65% | -9.89% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

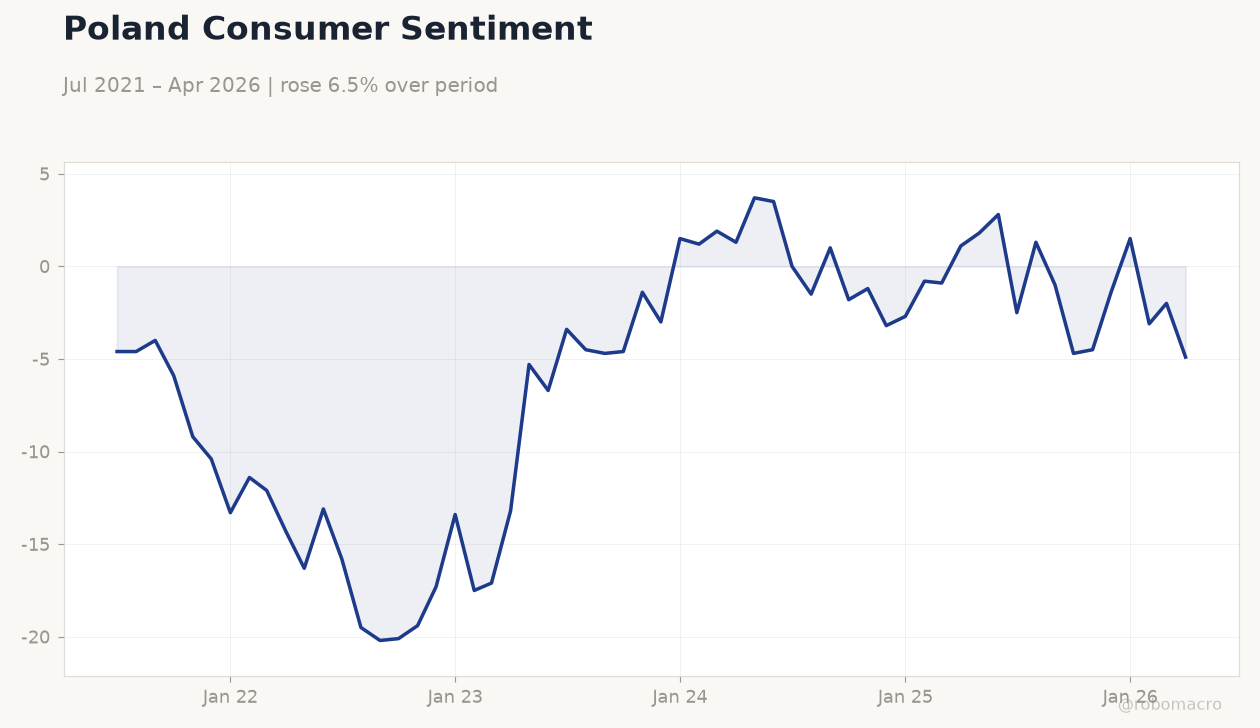

Poland Consumer Sentiment | Type: macro_line | Index: -4.9 (2026-04-01) | Range: -20.2–3.7 | Trend(6pt): -4.6,-20.2,-1.4,-2.7,-2,-4.9

Poland Consumer Sentiment | Type: macro_line | Index: -4.9 (2026-04-01) | Range: -20.2–3.7 | Trend(6pt): -4.6,-20.2,-1.4,-2.7,-2,-4.9

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Consumer Confidence Index | 85.80 | - | 23:00 |

| Headline Unemployment Rate | 6 | 5.90 | 23:30 |

- Poland's NBP gold reserves climbed to 613.9 tons, entering global top 10, while household prosperity index reached record EU levels.

- BIST 100 fell 0.63% to 14,734.50 and iShares Poland dropped 0.92% as EUR/PLN edged up 0.09% to 4.26 amid thin volumes.

- Hungary 10Y yields fell 9.89% to 5.65% on debt management changes; Turkey CCI and Poland unemployment due next.

Yesterday's Recap

Poland reported no macro releases but highlighted NBP gold accumulation of 18 tons through May, reinforcing reserve strength in the largest CEE economy. Equity markets closed lower with BIST 100 at 14,734.50 (-0.63%) and Poland ETF at 39.86 (-0.92%), while EUR/PLN rose modestly to 4.26. Hungary's 10Y yield dropped sharply to 5.65% after appointment of new debt chief focused on cost cuts, and e-commerce expanded 9.3% y/y.

Romania and Czech Republic saw negligible moves with EUR/CZK steady near 24.18. Turkey's USD/TRY held at 46.46 despite ongoing inflation pressures. Broader news underscored Poland's trillion-dollar economy status and EU prosperity gains, offsetting concerns over potential slowdown.

The Day Ahead

Turkey's Consumer Confidence Index releases tonight with prior reading at 85.8, offering insight into household sentiment under persistent high inflation. Poland's headline unemployment rate follows tomorrow at 23:30 ET, consensus pointing to 5.9% from 6.0% previously. No events scheduled for Czech Republic, Hungary or Romania.

Markets will monitor any CBRT signals on intervention amid USD/TRY stability. Thin summer liquidity may amplify reactions to these prints across CEE FX and bonds.

Other Economic Notes

Poland's rise in EU household prosperity rankings past four peers reflects sustained wage and consumption gains despite manufacturing softness. Hungary advances on Article 7 procedure exit talks could unlock cohesion funds and support forint stability. Czech kitchen sector bankruptcy highlights localized industrial strains but does not alter broader euro-convergence path.

Regional energy import reliance remains a shared vulnerability, though Poland's data-hub ambitions add diversification potential.

Global Macro News

ECB deposit rate stands at 2.25%, anchoring policy expectations for CNB and MNB responsiveness in the region. Eurozone unemployment at 6.70% supports steady external demand for Polish and Czech exports. Brent crude at 78.96 (-1.11%) eases import costs for Turkey and Hungary while gold at 4,214.40 provides reserve buffer.

<i>↓ p.2</i>