Emerging Europe Macro Daily(Beta Mode)

Polish Jobless Rate Eyed as Turkish Confidence Climbs

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| BIST 100 | 14,729.70 | -0.03% |

| iShares Poland | 39.86 | -0.92% |

| EUR/PLN | 4.28 | +0.69% |

| EUR/HUF | 350.45 | -0.34% |

| EUR/CZK | 24.20 | +0.10% |

| USD/TRY | 46.45 | +0.07% |

| Brent Crude | 76.68 | -1.57% |

| Gold | 4,137.80 | -1.05% |

| Bitcoin | 62,866.05 | -1.70% |

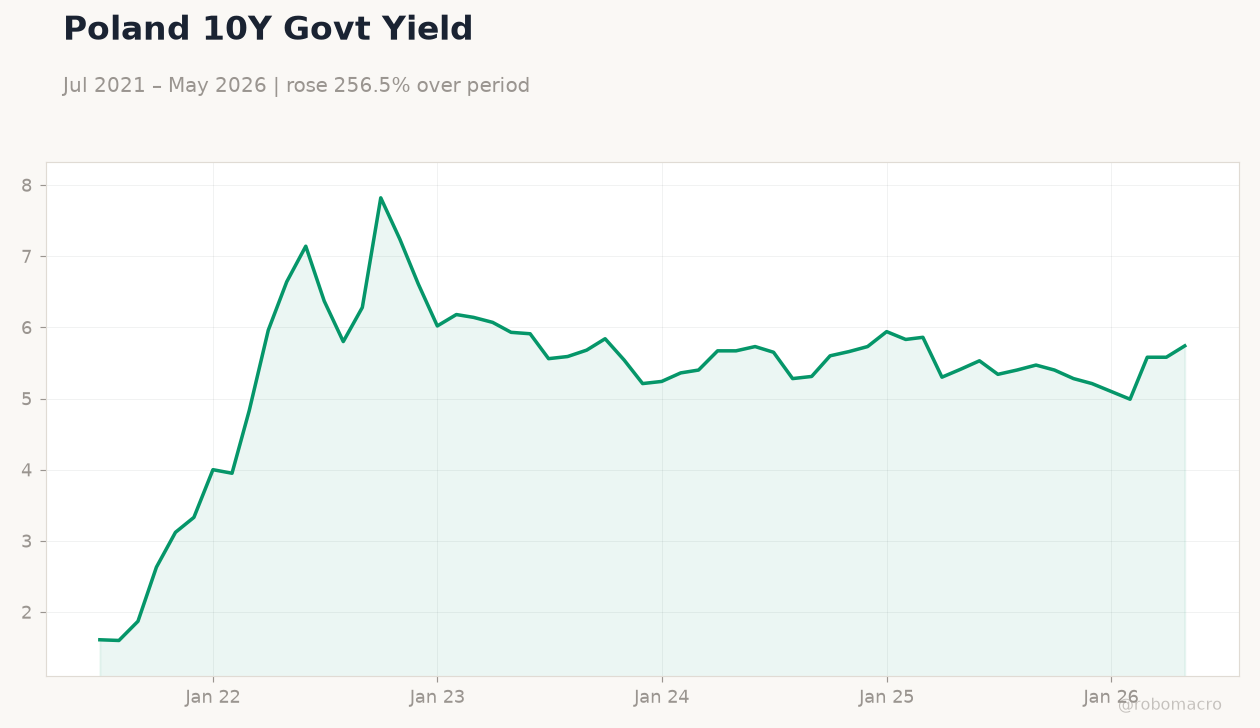

| Poland 10Y Govt Yield | 5.74% | +2.87% |

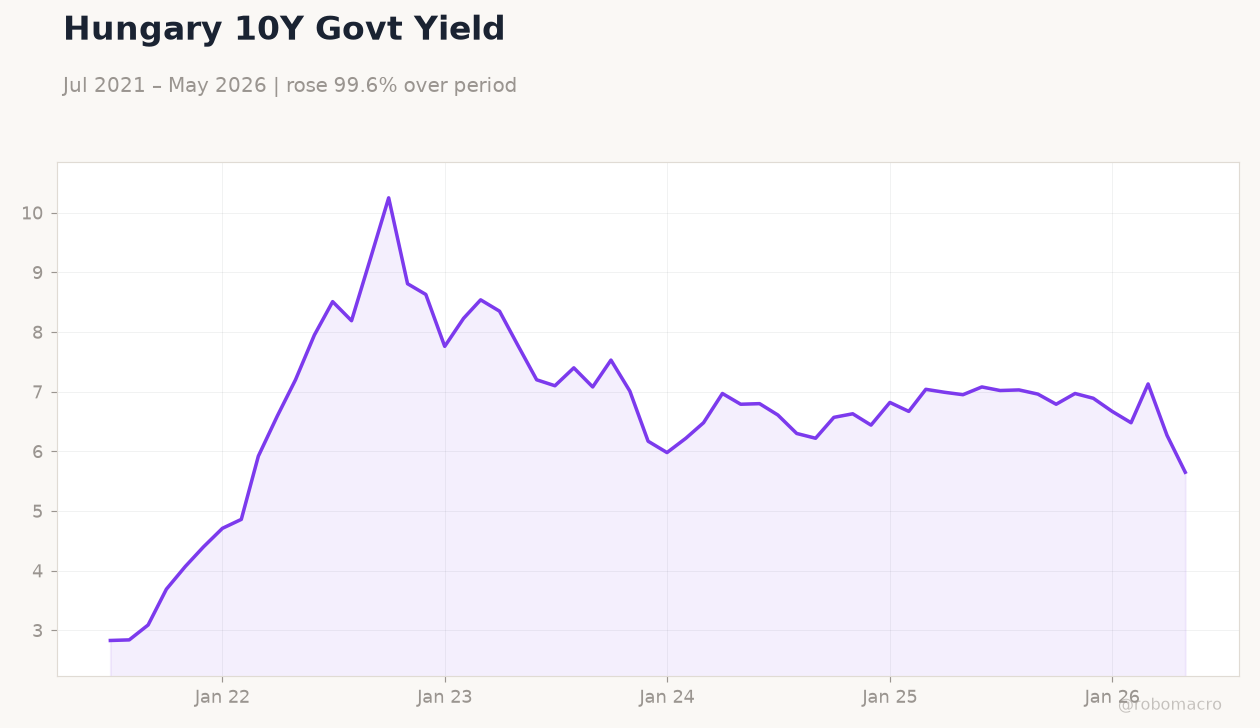

| Hungary 10Y Govt Yield | 5.65% | -9.89% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

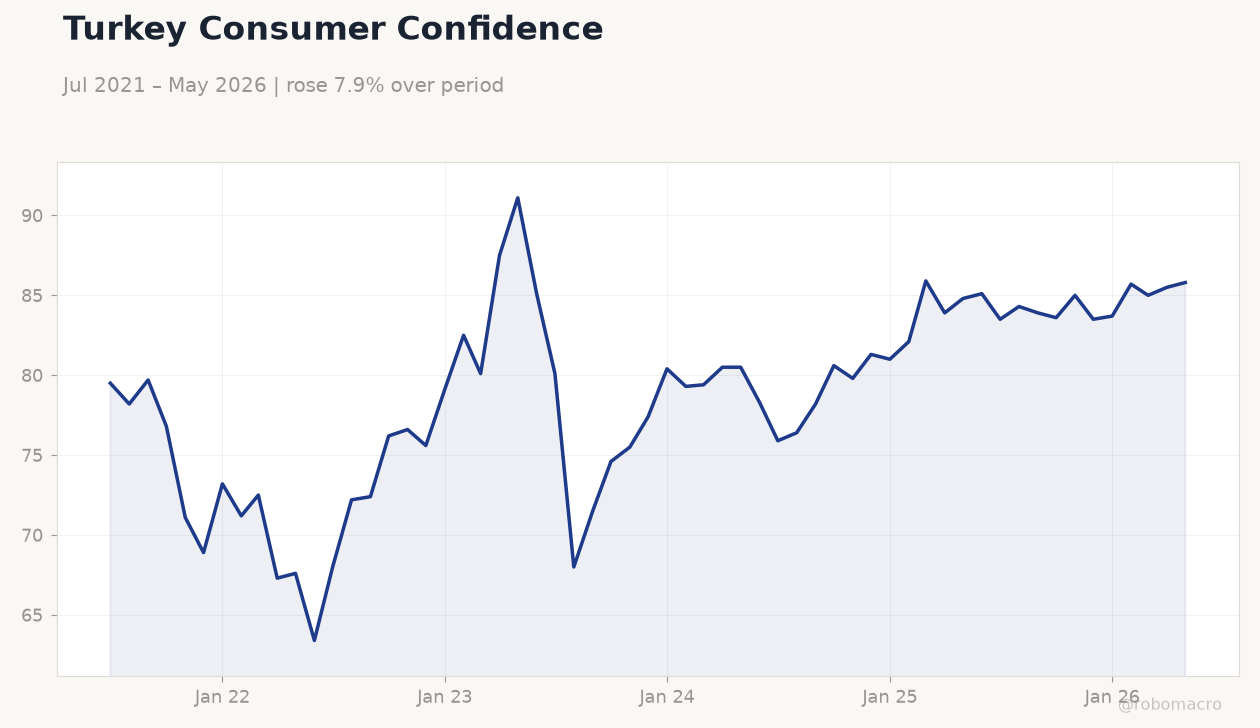

| Consumer Confidence Index | 85.80 | - | 87.90 |

Turkey Consumer Confidence | Type: macro_line | Consumer Confidence Index: 85.8 (2026-05-01) | Range: 63.4–91.1 | Trend(6pt): 79.5,72.4,75.5,81,85,85.8

Turkey Consumer Confidence | Type: macro_line | Consumer Confidence Index: 85.8 (2026-05-01) | Range: 63.4–91.1 | Trend(6pt): 79.5,72.4,75.5,81,85,85.8

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Headline Unemployment Rate | 6 | 5.90 | 23:30 |

| Wednesday (2026-06-24) | |||

| Headline Unemployment Rate | 6 | 5.90 | 23:30 |

- Turkey’s consumer confidence rose to 87.9 in June, beating prior reading and signalling modest household resilience.

- Poland’s unemployment rate is expected to edge lower to 5.9 % today, extending the labour-market improvement.

- Regional assets showed mixed moves, with Polish equities falling 0.92 % while Hungarian yields dropped sharply.

Yesterday's Recap

Turkey’s Consumer Confidence Index climbed to 87.9 from 85.8, the first gain in three months and a sign that households are adjusting to still-elevated but stabilising inflation. In Poland, June business sentiment indicators pointed to caution across manufacturing and services, with forward-looking components remaining below neutral. Equity markets closed mixed: the BIST 100 slipped 0.03 % while iShares Poland declined 0.92 %.

EUR/PLN rose 0.69 % to 4.28 amid positioning ahead of the unemployment print, whereas EUR/HUF eased 0.34 % to 350.45. Poland’s 10-year yield climbed 2.87 % to 5.74 %, contrasting with Hungary’s 10-year yield, which fell 9.89 % to 5.65 %. Brent crude dropped 1.57 % to 76.68, easing imported-energy costs for the region.

The Day Ahead

Poland releases its headline unemployment rate at 23:30 ET, with consensus pointing to a 5.9 % print that would mark further labour-market tightening. No other high-impact data are scheduled across the five markets today. Traders will monitor any follow-through from yesterday’s Turkish confidence reading for clues on domestic demand.

FX desks remain focused on EUR/PLN volatility around the Polish labour figure. Hungarian forint positioning may also react to any fresh comments from MNB officials on the timing of the next rate cut.

Other Economic Notes

A World Bank report highlighted that AI adoption could lift Poland’s GDP by up to 12 % by 2035 through productivity gains in services and manufacturing. Ukrainian workers and businesses continue to support Polish growth, adding both labour supply and entrepreneurial activity. Hungary’s central bank is likely to cut rates soon as forint strength and slowing inflation create room for easing.

Political tensions in Hungary intensified after Peter Magyar called for constitutional changes and removal of the president. Broader euro-area contraction data released overnight add downside risk to regional export outlooks.

Global Macro News

The eurozone economy contracted in the latest reading, weighing on external demand for Polish and Czech exporters. Singapore’s May inflation held at 1.8 %, cooler than expected and reinforcing the global disinflation narrative. <i>↓ p.2</i>