Emerging Europe Macro Daily(Beta Mode)

MNB Cuts Rates as Forint Strengthens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| BIST 100 | 14,539.60 | -1.29% |

| iShares Poland | 39.86 | -0.92% |

| EUR/PLN | 4.28 | +0.33% |

| EUR/HUF | 355.65 | +1.04% |

| EUR/CZK | 24.22 | +0.18% |

| USD/TRY | 46.49 | +0.06% |

| Brent Crude | 76.35 | -0.95% |

| Gold | 4,103.90 | -0.63% |

| Bitcoin | 62,718.71 | +0.08% |

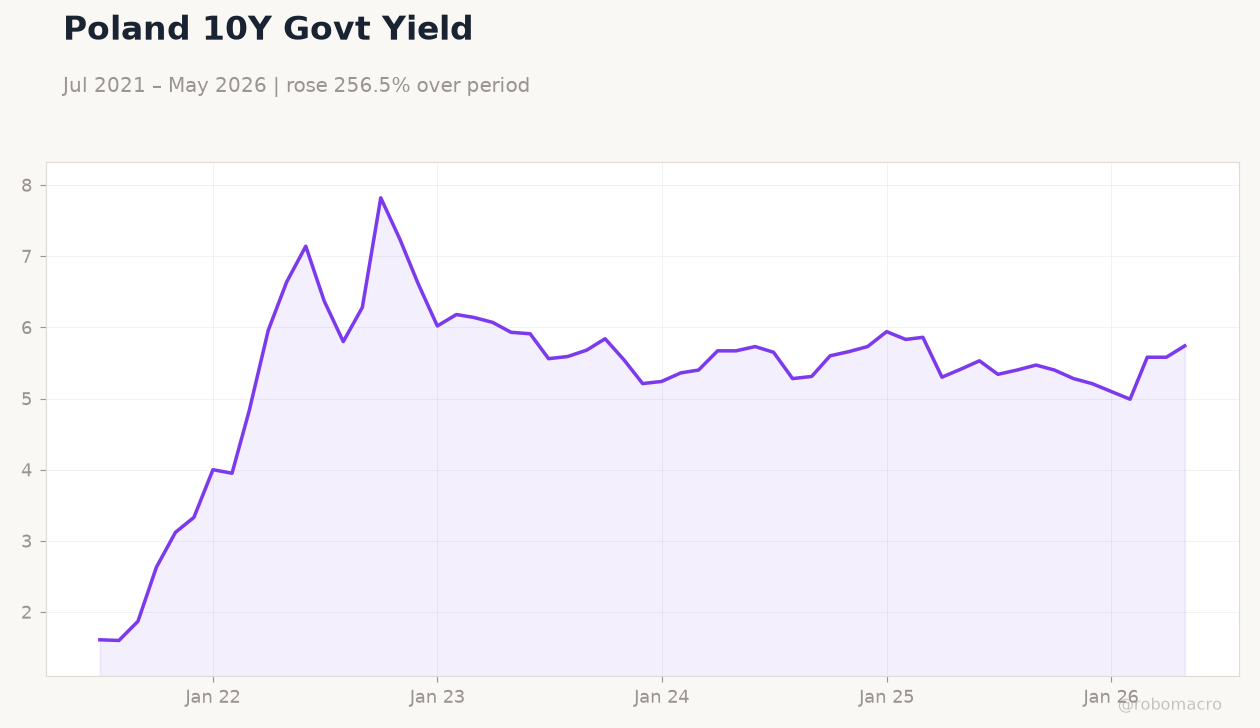

| Poland 10Y Govt Yield | 5.74% | +2.87% |

| Hungary 10Y Govt Yield | 5.65% | -9.89% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

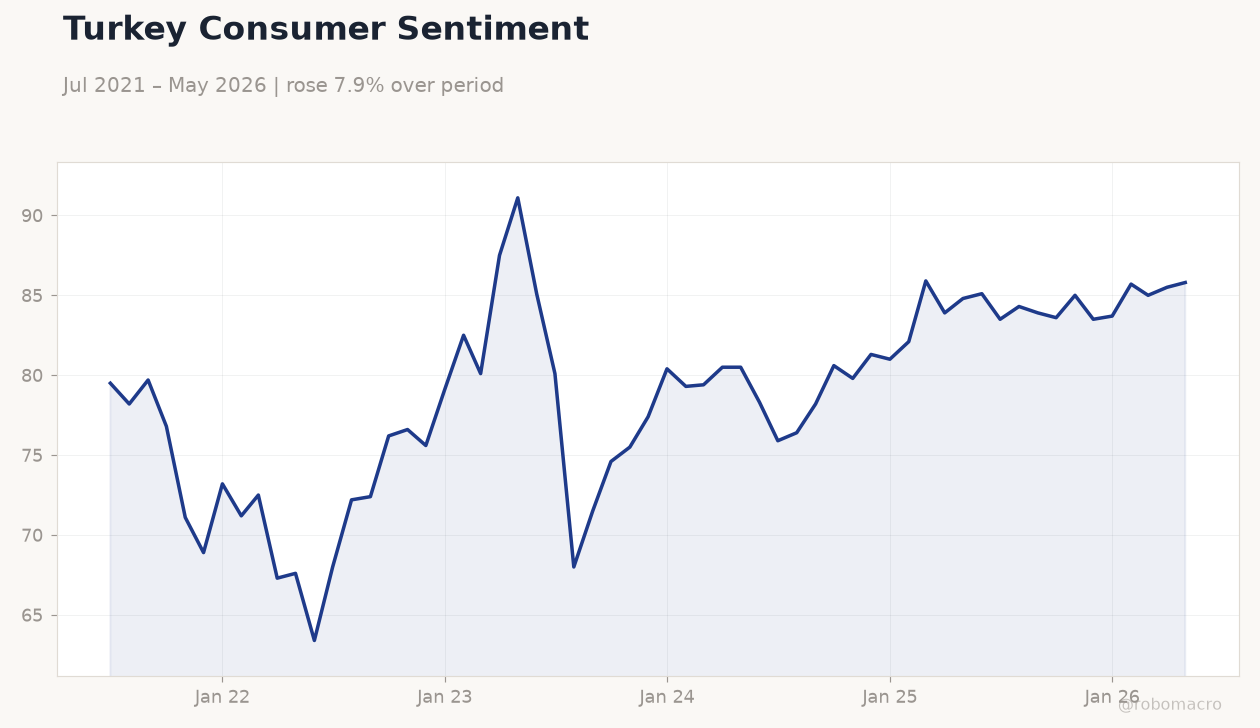

| Consumer Confidence Index | 85.80 | - | 87.90 |

Turkey Consumer Sentiment | Type: macro_line | Index: 85.8 (2026-05-01) | Range: 63.4–91.1 | Trend(6pt): 79.5,72.4,75.5,81,85,85.8

Turkey Consumer Sentiment | Type: macro_line | Index: 85.8 (2026-05-01) | Range: 63.4–91.1 | Trend(6pt): 79.5,72.4,75.5,81,85,85.8

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Headline Unemployment Rate | 6 | 5.90 | 23:30 |

- MNB reduced its key rate by 25bp to 6%, citing forint gains and cooling inflation pressures.

- Turkey’s consumer confidence rose to 87.9 in June from 85.8 prior.

- Regional assets closed mixed: BIST 100 fell 1.29% while Hungary 10Y yields dropped 9.89%.

Yesterday's Recap

Turkey’s June consumer confidence index climbed to 87.9, reflecting modest improvement in household sentiment. Hungary’s MNB delivered the widely expected 25bp cut to 6%, highlighting room for further easing if forint stability persists. Equity markets reflected divergent sentiment, with BIST 100 declining 1.29% to 14,539.60 while iShares Poland slipped 0.92% to 39.86.

Currency moves showed EUR/PLN rising 0.33% to 4.28 and EUR/HUF jumping 1.04% to 355.65, while USD/TRY edged 0.06% higher to 46.49. Sovereign yields reacted sharply in Hungary, where the 10Y yield fell 9.89% to 5.65%, contrasting with Poland’s 10Y yield rising 2.87% to 5.74%. Brent crude declined 0.95% to 76.35, adding mild downside pressure to energy importers across the region.

News flow also highlighted ongoing Poland-Ukraine tensions and Türkiye’s continued push for closer EU defense ties.

The Day Ahead

Poland’s headline unemployment rate for May is due today with consensus at 5.9% versus 6.0% prior, offering the first labor-market read since the NBP’s last hold. No other high-impact releases are scheduled across the five markets. Traders will monitor any follow-up comments from MNB Governor Varga on the scope for additional cuts.

FX markets remain sensitive to ECB signals given the 2.25% deposit rate. Broader regional focus stays on forint and zloty performance after yesterday’s moves.

Other Economic Notes

Poland stands to gain up to 12% in GDP from AI adoption by 2035 according to recent estimates, supporting long-term productivity. Hungary’s rate cut diverges from the global tightening tilt, reflecting forint appreciation and subdued industrial output. Energy import dependence remains a shared vulnerability for all five economies, with Brent at 76.35 underscoring the risk.

EU fund flows continue to favor Poland and Romania while Hungary’s disbursements stay frozen over rule-of-law concerns.

Global Macro News

The ECB deposit rate holds at 2.25%, anchoring regional policy expectations and limiting CNB and MNB room for aggressive divergence. US-China tariff tensions are generating uneven third-country gains, with limited direct spillovers so far to CEE supply chains. <i>↓ p.2</i>