Emerging Europe Macro Daily(Beta Mode)

Turkish Confidence Rises, ECB Flags CEE Gaps

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| BIST 100 | 14,331.20 | -1.43% |

| iShares Poland | 37.99 | -1.91% |

| EUR/PLN | 4.29 | +0.20% |

| EUR/HUF | 354.94 | +0.31% |

| EUR/CZK | 24.23 | +0.14% |

| USD/TRY | 46.51 | +0.08% |

| Brent Crude | 72.58 | -1.57% |

| Gold | 4,013.80 | +0.59% |

| Bitcoin | 61,440.36 | -1.96% |

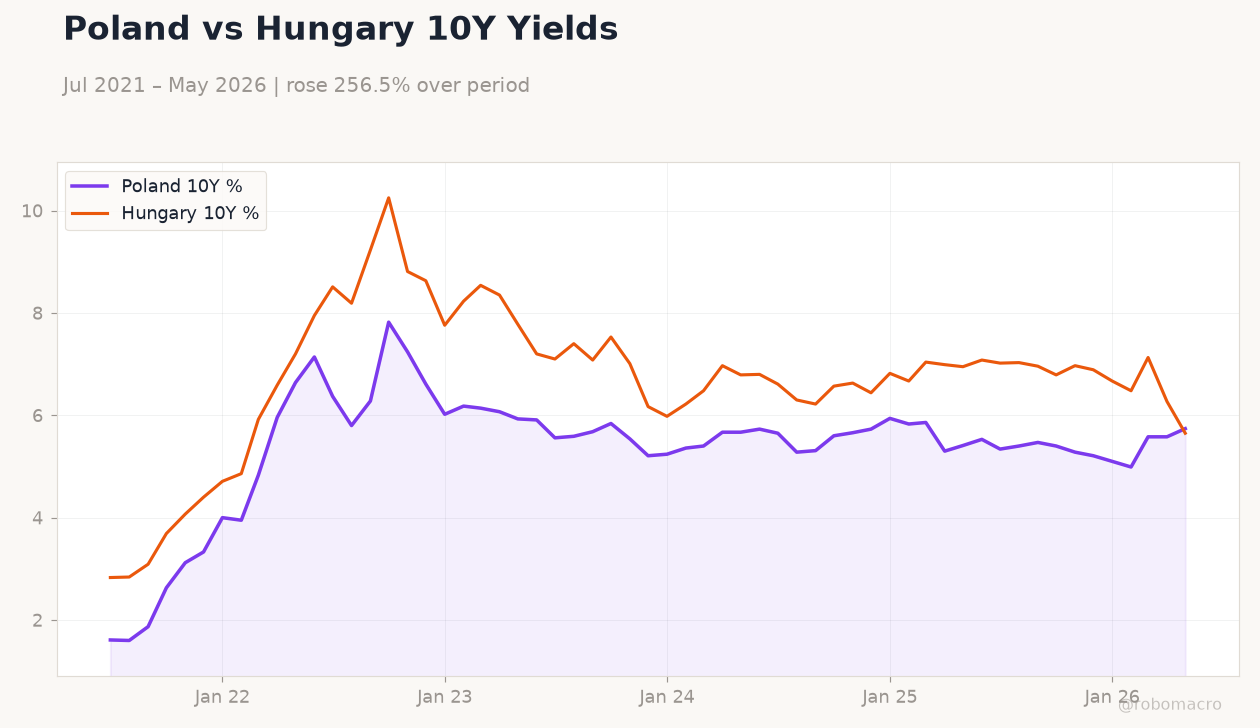

| Poland 10Y Govt Yield | 5.74% | +2.87% |

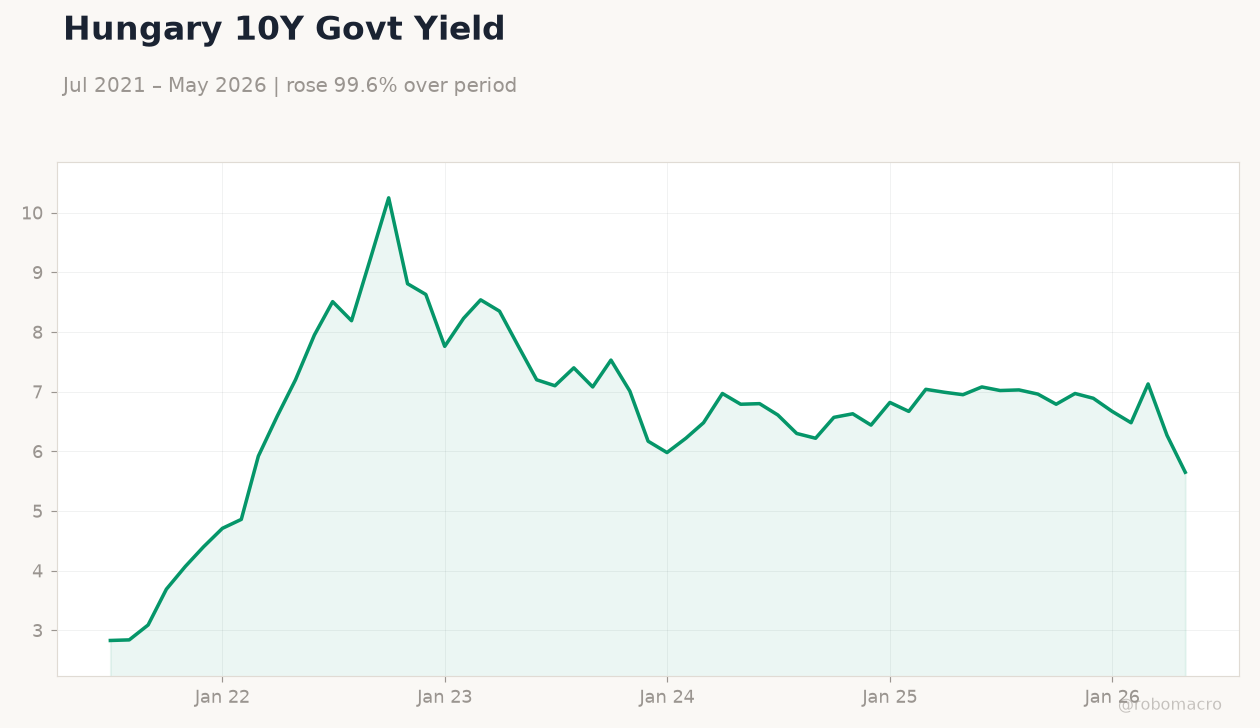

| Hungary 10Y Govt Yield | 5.65% | -9.89% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

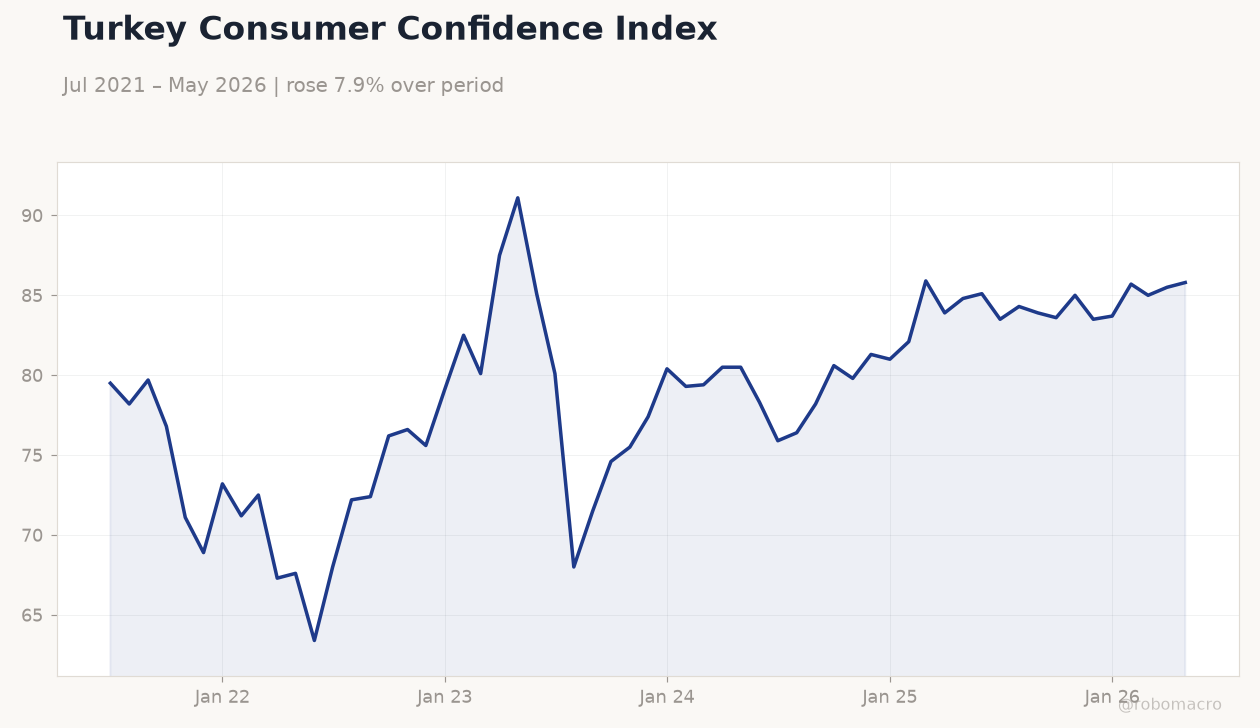

| Consumer Confidence Index | 85.80 | - | 87.90 |

| Headline Unemployment Rate | 6 | 5.90 | 5.90 |

Turkey Consumer Confidence Index | Type: macro_line | Index: 85.8 (2026-05-01) | Range: 63.4–91.1 | Trend(6pt): 79.5,72.4,75.5,81,85,85.8

Turkey Consumer Confidence Index | Type: macro_line | Index: 85.8 (2026-05-01) | Range: 63.4–91.1 | Trend(6pt): 79.5,72.4,75.5,81,85,85.8

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Turkish consumer confidence rose to 87.9 in June from 85.8, while Polish unemployment held at 5.9%.

- Regional equities fell with BIST 100 down 1.43% and iShares Poland off 1.91%; EUR/PLN edged up 0.20% to 4.29.

- ECB convergence report showed Poland, Czech Republic, Hungary and Romania still miss euro-adoption criteria.

Yesterday's Recap

Turkey’s Consumer Confidence Index climbed to 87.9, beating the prior 85.8 reading and signalling modest household resilience. Poland’s headline unemployment rate printed at 5.9%, matching consensus and improving from 6.0% previously, consistent with steady labour-market conditions. Equity markets closed lower, with BIST 100 falling 1.43% to 14,331.20 and iShares Poland declining 1.91% to 37.99 amid risk-off flows.

Currency moves were modest: EUR/PLN rose 0.20% to 4.29, EUR/HUF gained 0.31% to 354.94 and EUR/CZK advanced 0.14% to 24.23. Sovereign yields diverged, with Poland’s 10-year yield rising 2.87% to 5.74% while Hungary’s 10-year yield dropped 9.89% to 5.65%. Brent crude fell 1.57% to 72.58, adding mild downward pressure on energy importers.

The Day Ahead

No major data releases are scheduled for Poland, Czech Republic, Hungary, Romania or Turkey today or tomorrow. Markets will monitor follow-through from the ECB’s latest convergence assessment and any comments from regional central-bank officials. Poland’s finance ministry continues to advance space-sector ambitions, which may influence medium-term fiscal priorities.

Hungary’s forint trajectory after the recent MNB easing remains in focus for carry-trade positioning. Broader sentiment will also track euro-area developments given tight trade linkages.

Other Economic Notes

The ECB convergence report underscores persistent gaps in price stability, fiscal metrics and legal compatibility for euro adoption across Poland, Czech Republic, Hungary and Romania. Retail-bond issuance in the Czech Republic attracted record demand, trimming institutional allocations and highlighting strong domestic liquidity. Hungary’s demographic headwinds are already constraining labour supply and potential growth, according to ING’s latest forecast.

Energy-import dependence continues to expose the region to global commodity swings, with Brent’s decline offering limited near-term relief.

Global Macro News

The ECB maintains its deposit rate at 2.25%, providing a stable external anchor for CEE monetary-policy expectations. Euro-area unemployment stood at 6.70% in the latest reading, supporting gradual demand recovery that benefits Polish and Czech exporters. <i>↓ p.2</i>