Emerging Europe Macro Daily(Beta Mode)

Turkish Confidence Up, Hungarian Yields Down

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| BIST 100 | 14,259.80 | -0.50% |

| iShares Poland | 37.99 | -1.91% |

| EUR/PLN | 4.28 | +0.07% |

| EUR/HUF | 354.36 | -0.25% |

| EUR/CZK | 24.27 | +0.21% |

| USD/TRY | 46.62 | +0.25% |

| Brent Crude | 74.27 | -1.32% |

| Gold | 4,041.20 | +0.27% |

| Bitcoin | 60,151.85 | +0.72% |

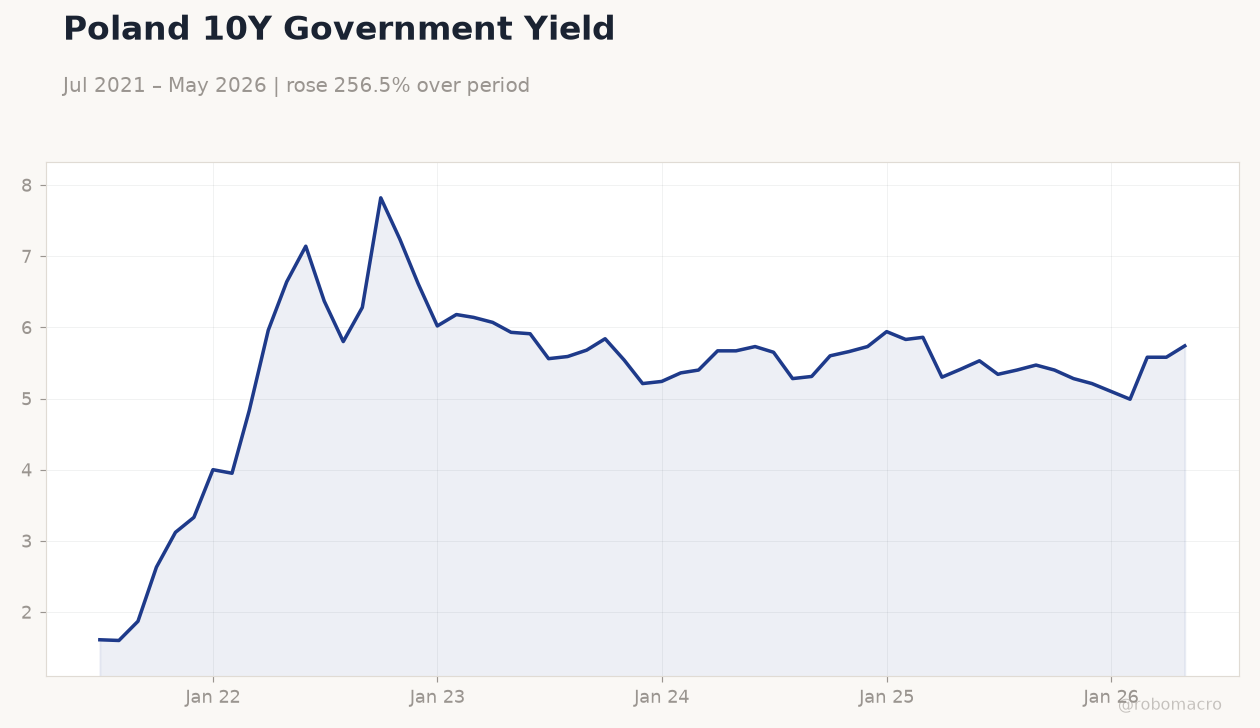

| Poland 10Y Govt Yield | 5.74% | +2.87% |

| Hungary 10Y Govt Yield | 5.65% | -9.89% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

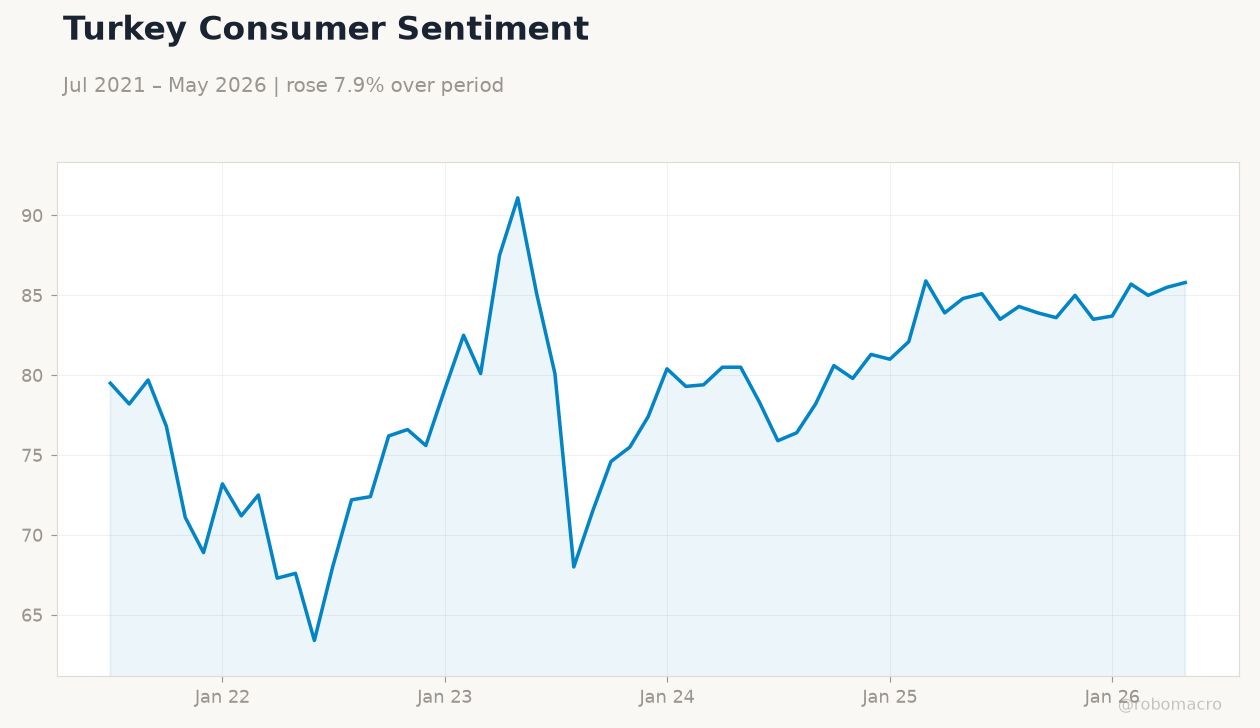

| Consumer Confidence Index | 85.80 | - | 87.90 |

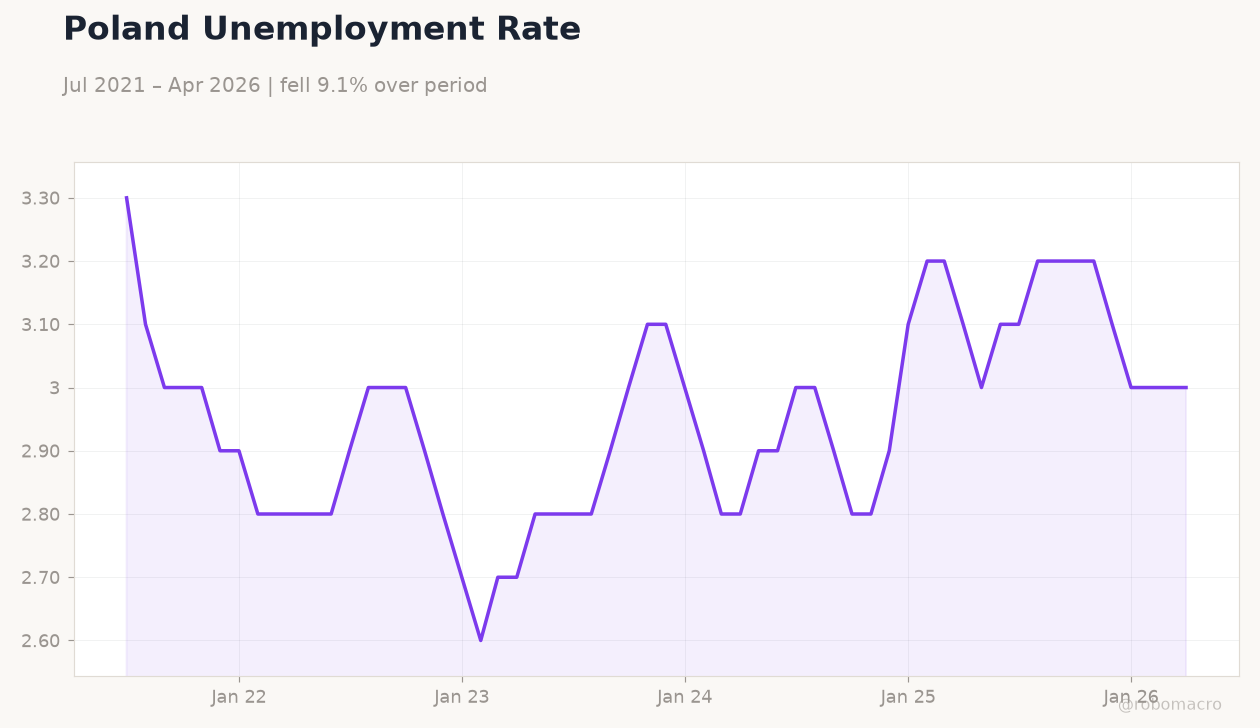

| Headline Unemployment Rate | 6 | 5.90 | 5.90 |

Poland 10Y Government Yield | Type: macro_line | Yield %: 5.74 (2026-05-01) | Range: 1.6–7.82 | Trend(6pt): 1.61,6.28,5.54,5.94,5.58,5.74

Poland 10Y Government Yield | Type: macro_line | Yield %: 5.74 (2026-05-01) | Range: 1.6–7.82 | Trend(6pt): 1.61,6.28,5.54,5.94,5.58,5.74

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Turkish consumer confidence improved to 87.9 in June while Polish unemployment held at 5.9 percent.

- Hungarian 10-year yields dropped 9.89 percent amid softer MNB inflation projections; Polish yields rose 2.87 percent.

- BIST 100 fell 0.50 percent and iShares Poland declined 1.91 percent as EUR/PLN edged 0.07 percent higher.

Yesterday's Recap

Turkish consumer confidence rose to 87.9 from 85.8, signaling modest improvement in household sentiment ahead of summer. Poland’s headline unemployment rate stayed at 5.9 percent, matching consensus and confirming labor-market stability in the region’s largest EU economy. Hungary’s 10-year government yield fell sharply to 5.65 percent as the MNB’s updated inflation report pointed to a 2 percent reading in the second half of the year.

Poland’s 10-year yield climbed to 5.74 percent, widening the spread versus Hungary. The BIST 100 closed 0.50 percent lower at 14,259.80 while the Polish equity ETF dropped 1.91 percent to 37.99. EUR/HUF eased 0.25 percent to 354.36, reflecting forint strength on the softer inflation outlook.

EUR/CZK rose 0.21 percent to 24.27 as the koruna lagged regional peers. Poland submitted its eighth KPO disbursement request worth 33.8 billion zloty, underscoring continued EU fund inflows that support both fiscal and investment spending.

The Day Ahead

No major data releases are scheduled across the five markets today or tomorrow, leaving trading desks focused on positioning ahead of the weekend. Attention will remain on any follow-up comments from the MNB after its revised forecasts and on Polish officials’ statements regarding the latest KPO payment request. Currency desks will monitor EUR/PLN around 4.28 and USD/TRY near 46.62 for signs of further drift.

Equity flows may stay light given the absence of corporate earnings or policy events. Regional fixed-income markets are expected to take cues from Bund movements and any ECB speakers.

Other Economic Notes

The MNB highlighted an 18 percent year-on-year rise in apartment prices and warned that new housing supply could stagnate without further policy support. Energy-import dependence remains a common vulnerability for Poland, Hungary and the Czech Republic, with Brent crude down 1.32 percent to 74.27 offering limited near-term relief. Regional equity markets continue to price divergent growth trajectories, with Hungary appearing more sensitive to inflation revisions than Poland.

Trade tensions and reconstruction financing in Ukraine continued to feature in Polish policy discussions, with potential knock-on effects for regional supply chains.