Emerging Europe Macro Daily(Beta Mode)

Polish CPI, Turkish Trade Data in Focus

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| BIST 100 | 14,183.20 | -0.64% |

| iShares Poland | 38.48 | +0.55% |

| EUR/PLN | 4.29 | +0.05% |

| EUR/HUF | 354.43 | +0.75% |

| EUR/CZK | 24.25 | +0.06% |

| USD/TRY | 46.66 | +0.08% |

| Brent Crude | 73.12 | -0.04% |

| Gold | 4,035.80 | +0.34% |

| Bitcoin | 59,500.78 | -1.06% |

| Poland 10Y Govt Yield | 5.74% | +2.87% |

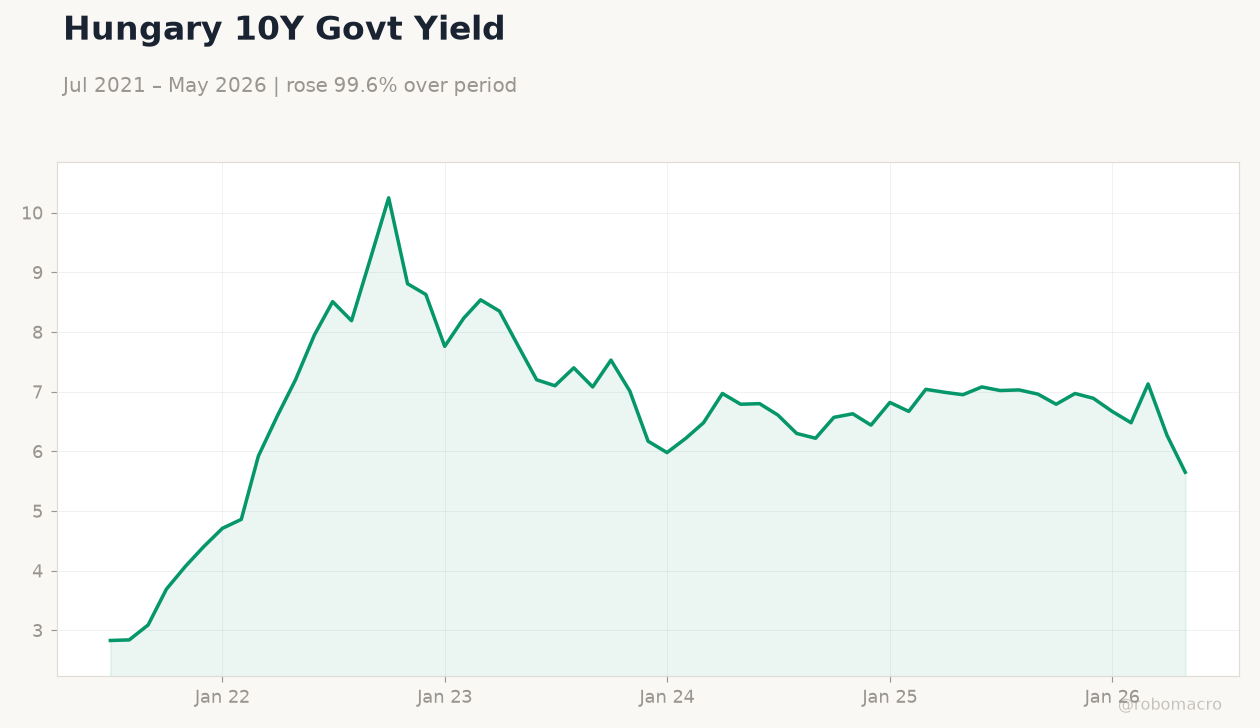

| Hungary 10Y Govt Yield | 5.65% | -9.89% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Poland vs Hungary 10Y Yields | Type: macro_line | Poland Yield %: 5.74 (2026-05-01) | Range: 1.6–7.82 | Trend(6pt): 1.61,6.28,5.54,5.94,5.58,5.74 | Hungary Yield %: 5.65 (2026-05-01) | Range: 2.83–10.25 | Trend(6pt): 2.83,9.23,7.01,6.82,7.13,5.65

Poland vs Hungary 10Y Yields | Type: macro_line | Poland Yield %: 5.74 (2026-05-01) | Range: 1.6–7.82 | Trend(6pt): 1.61,6.28,5.54,5.94,5.58,5.74 | Hungary Yield %: 5.65 (2026-05-01) | Range: 2.83–10.25 | Trend(6pt): 2.83,9.23,7.01,6.82,7.13,5.65

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Balance of Trade Final | -8,500m | -5,600m | 23:00 |

| Headline Unemployment Rate | 8.20 | - | 23:00 |

| Inflation Rate Year-over-Year Preliminary | 3.10 | - | 23:30 |

| Inflation Rate Month-over-Month | 1.71 | - | 23:00 |

| Inflation Rate Year-over-Year | 32.61 | - | 23:00 |

- Polish banks posted 17.6 billion zł net profit in Jan-May, down 15.6% y/y, while discount stores now account for nearly half of retail outlets.

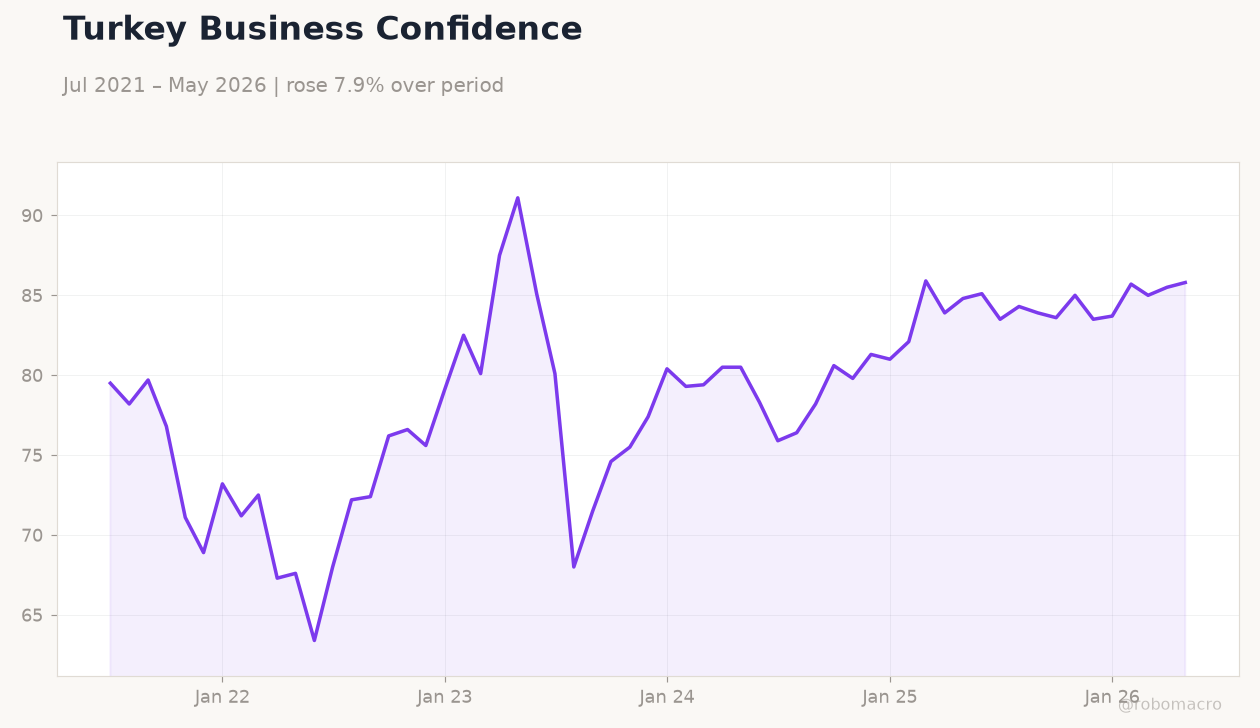

- Regional FX stayed stable with EUR/PLN at 4.29 and USD/TRY at 46.66; BIST 100 fell 0.64% while iShares Poland rose 0.55%.

- Ukraine secured over €10bn in recovery agreements at the Gdańsk conference; extreme heat raises energy and agricultural risks across Europe.

Yesterday's Recap

Polish equity and fixed-income markets reflected caution ahead of inflation data, with the WIG-linked iShares Poland ETF gaining 0.55% while the Poland 10Y yield climbed 2.87% to 5.74%. Hungary 10Y yields dropped 9.89% to 5.65%. Turkish assets were little changed, with BIST 100 declining 0.64% to 14,183.20 and USD/TRY rising 0.08% to 46.66.

News that Polish banks earned 17.6 billion zł through May but saw profits shrink 15.6% year-on-year added to domestic sentiment. EUR/HUF rose 0.75% to 354.43 while EUR/CZK edged 0.06% higher to 24.25. Brent Crude held at 73.12, gold rose 0.34% to 4,035.80 and Bitcoin fell 1.06% to 59,500.78.

No major data prints occurred across the region on 29 June.

The Day Ahead

Turkey releases final Balance of Trade and Headline Unemployment Rate figures tonight, with markets focused on the trade gap narrowing from the prior -8.5 billion USD print. Poland publishes preliminary Inflation Rate YoY at 23:30 ET, following the last reading of 3.1%. Two further Turkish inflation prints follow on 2 July covering both monthly and annual rates.

No releases are scheduled for the Czech Republic, Hungary or Romania. Traders will monitor any ECB-related spillovers given the 2.25% deposit rate.

Other Economic Notes

Extreme heat across Europe is raising concerns over energy demand and agricultural output, with potential knock-on effects for import-dependent economies in the region. Poland continues to receive cohesion funds after satisfying rule-of-law conditions, while Hungary faces ongoing delays on roughly €10 billion. Retail concentration in Poland, where discount stores approach 50% of outlets, signals maturing consumer markets that could cap future price pressures.

Ukraine left the Gdańsk conference with roughly 200 agreements worth over €10bn.

Global Macro News

The ECB Deposit Rate stands at 2.25%, providing a benchmark for CNB and MNB policy calibration. Eurozone unemployment registered 6.70% on the latest available reading. <i>↓ p.2</i>