Emerging Europe Macro Daily(Beta Mode)

Poland CPI Hits NBP Target as Turkey Trade Narrows

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| BIST 100 | 14,121.80 | -0.43% |

| iShares Poland | 38.61 | +0.34% |

| EUR/PLN | 4.30 | +0.38% |

| EUR/HUF | 356.06 | +0.90% |

| EUR/CZK | 24.27 | +0.14% |

| USD/TRY | 46.67 | +0.07% |

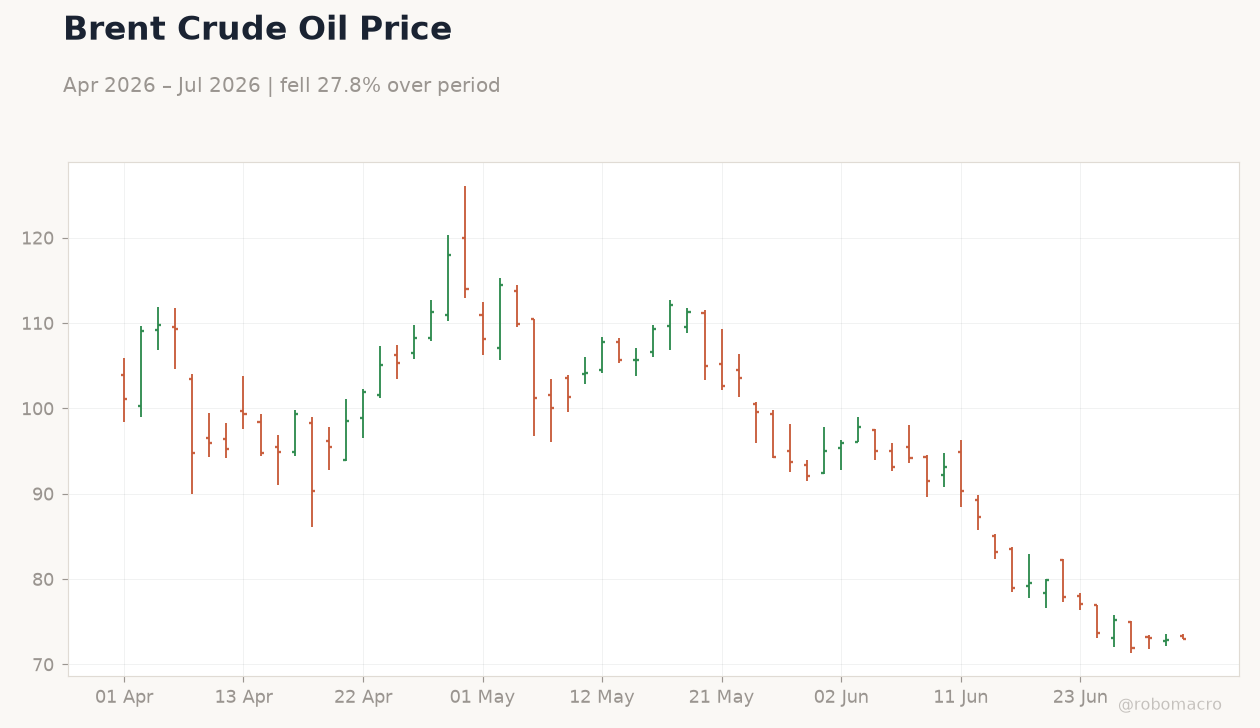

| Brent Crude | 72.97 | +0.07% |

| Gold | 3,983.50 | -0.98% |

| Bitcoin | 58,687.94 | +0.22% |

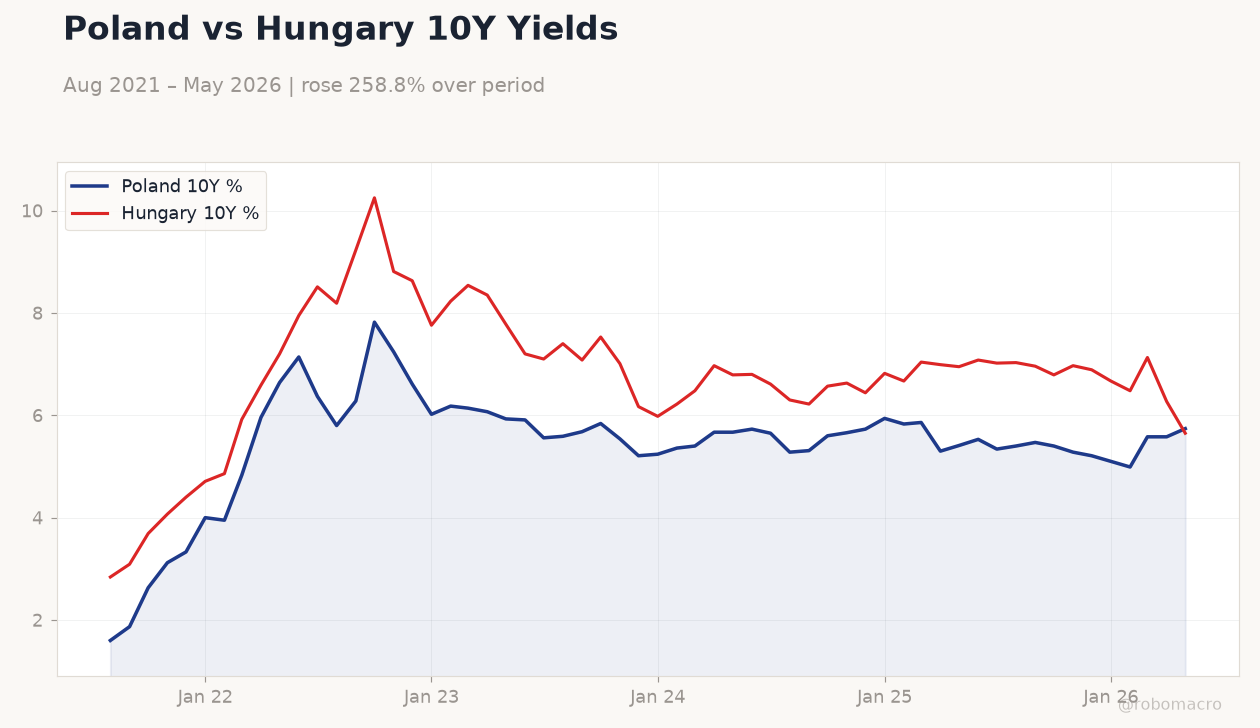

| Poland 10Y Govt Yield | 5.74% | +2.87% |

| Hungary 10Y Govt Yield | 5.65% | -9.89% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Balance of Trade Final | -8,500m | -5,600m | -5,610m |

| Headline Unemployment Rate | 8.20 | - | 8.20 |

| Inflation Rate Year-over-Year Preliminary | 3.10 | 2.70 | 2.50 |

Poland vs Hungary 10Y Yields | Type: macro_line | Poland 10Y %: 5.74 (2026-05-01) | Range: 1.6–7.82 | Trend(6pt): 1.6,7.82,5.21,5.83,5.58,5.74 | Hungary 10Y %: 5.65 (2026-05-01) | Range: 2.84–10.25 | Trend(6pt): 2.84,10.25,6.17,6.67,6.27,5.65

Poland vs Hungary 10Y Yields | Type: macro_line | Poland 10Y %: 5.74 (2026-05-01) | Range: 1.6–7.82 | Trend(6pt): 1.6,7.82,5.21,5.83,5.58,5.74 | Hungary 10Y %: 5.65 (2026-05-01) | Range: 2.84–10.25 | Trend(6pt): 2.84,10.25,6.17,6.67,6.27,5.65

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Inflation Rate Month-over-Month | 1.71 | - | 23:00 |

| Inflation Rate Year-over-Year | 32.61 | - | 23:00 |

- Poland June CPI fell to 2.5% y/y, landing exactly at the NBP target and below consensus.

- Turkey May trade deficit narrowed to $5.61bn, matching expectations, while unemployment held at 8.2%.

- Regional FX saw EUR/PLN rise 0.38% to 4.30 and Hungary 10Y yields drop 9.89% as markets digested the prints.

Yesterday's Recap

Poland’s preliminary June inflation printed at 2.5% y/y, undershooting the 2.7% consensus and landing exactly at the NBP 2.5% target. The outturn reflected broad-based disinflation. Turkey’s May trade balance came in at -$5.61bn, in line with the consensus forecast, while the headline unemployment rate remained steady at 8.2%.

Equity markets showed modest divergence, with the BIST 100 declining 0.43% to 14,121.80 and iShares Poland gaining 0.34% to 38.61. EUR/PLN rose 0.38% to 4.30 and EUR/HUF climbed 0.90% to 356.06. Poland’s 10Y yield rose 2.87% to 5.74% while Hungary’s 10Y yield fell 9.89% to 5.65%.

Brent crude edged 0.07% higher to 72.97.

The Day Ahead

Turkey will release June inflation figures at 23:00 ET, covering both month-on-month and year-on-year prints. Markets will focus on whether the recent moderation in monthly price pressures persists. No Tier-1 data are scheduled for Poland, Hungary, Czech Republic or Romania.

Central bank speakers from the NBP and CNB are expected to comment on the latest inflation trajectory. Regional FX desks will monitor any follow-through in EUR/PLN after yesterday’s move above 4.30.

Other Economic Notes

Poland’s return to the NBP target reduces the likelihood of near-term rate cuts and supports zloty stability. Hungary’s sharp 10Y yield compression signals improving local demand for duration. Broader CEE economies continue to benefit from lower imported energy costs, though Turkey’s structurally higher inflation keeps real rates negative and sustains pressure on TRY.

EU fund disbursements remain a key swing factor for Poland and Romania’s fiscal outlooks.

Global Macro News

Yen weakness to 40-year lows has revived intervention risks, indirectly supporting carry trades into higher-yielding CEE currencies. US Republican pressure on defense spending bills tied to Poland highlights ongoing geopolitical funding linkages. Global equity sentiment remains supported by stable oil prices near 73, limiting imported inflation risks for net energy importers in the region.

Polish media noted that inflation will surge again but the NBP will not panic, with CPI expected to return to target only in Q3 2027.