Emerging Europe Macro Daily(Beta Mode)

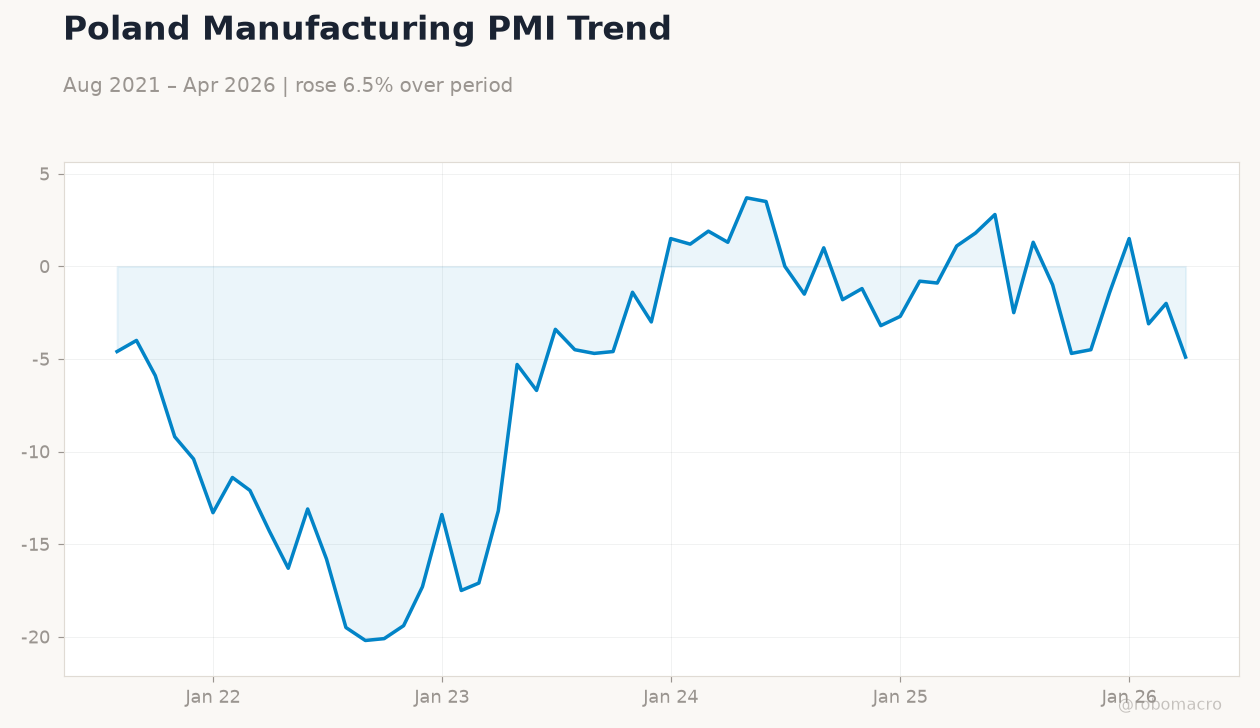

Poland CPI Cools, PMI Slumps

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| BIST 100 | 14,423.74 | +0.51% |

| iShares Poland | 38.69 | +0.21% |

| EUR/PLN | 4.29 | -0.05% |

| EUR/HUF | 355.66 | +0.26% |

| EUR/CZK | 24.23 | -0.01% |

| USD/TRY | 46.69 | +0.07% |

| Brent Crude | 70.58 | -1.38% |

| Gold | 4,079.10 | +0.27% |

| Bitcoin | 60,081.74 | +0.13% |

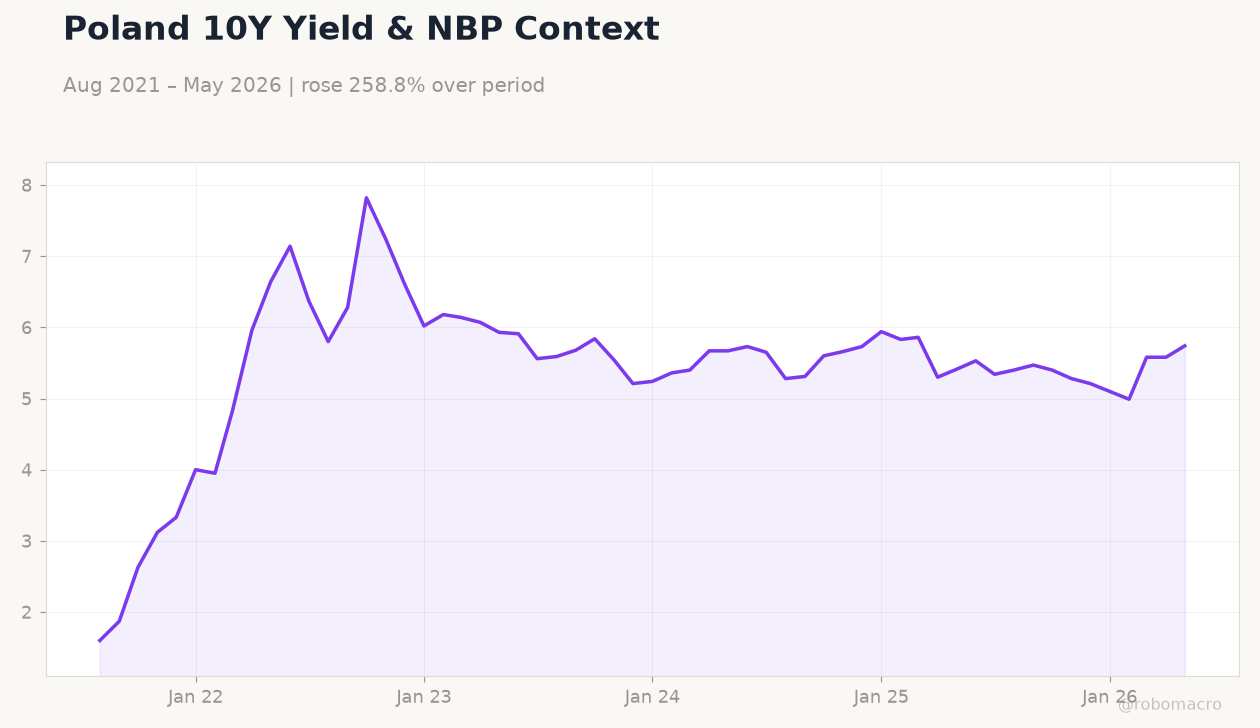

| Poland 10Y Govt Yield | 5.74% | +2.87% |

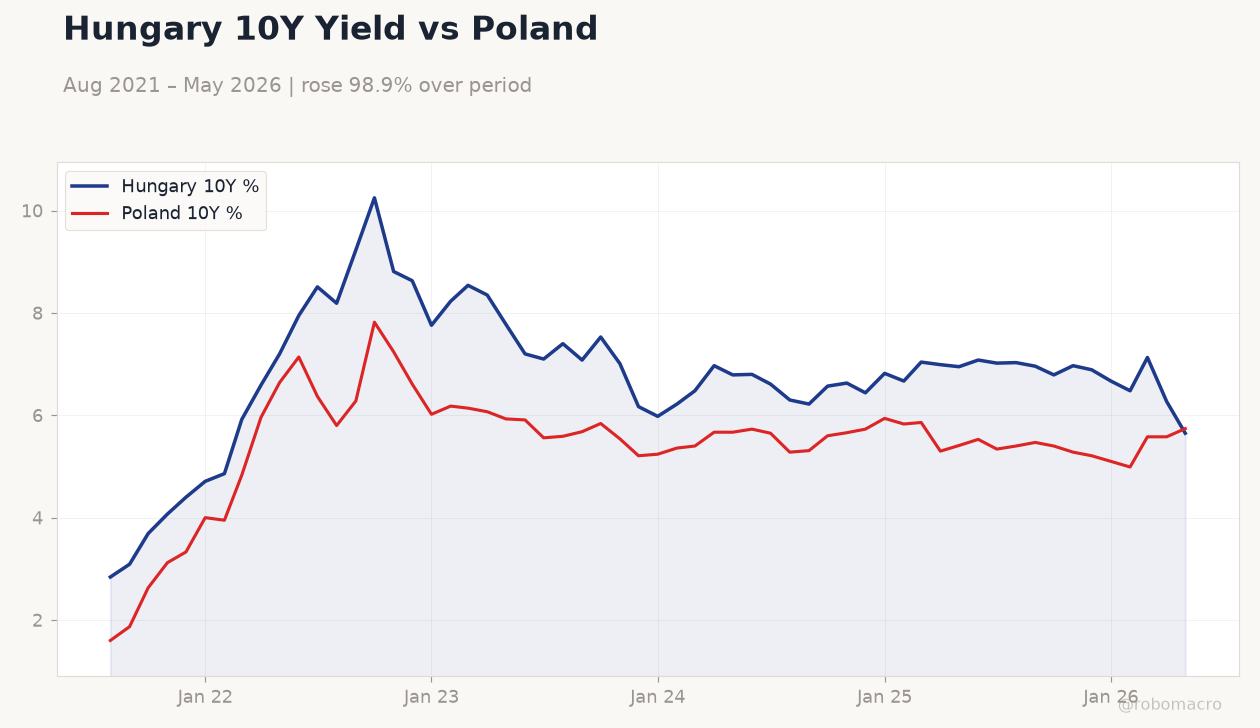

| Hungary 10Y Govt Yield | 5.65% | -9.89% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Balance of Trade Final | -8,500m | -5,600m | -5,610m |

| Headline Unemployment Rate | 8.20 | - | 8.20 |

| Inflation Rate Year-over-Year Preliminary | 3.10 | 2.70 | 2.50 |

Hungary 10Y Yield vs Poland | Type: macro_line | Hungary 10Y %: 5.65 (2026-05-01) | Range: 2.84–10.25 | Trend(6pt): 2.84,10.25,6.17,6.67,6.27,5.65 | Poland 10Y %: 5.74 (2026-05-01) | Range: 1.6–7.82 | Trend(6pt): 1.6,7.82,5.21,5.83,5.58,5.74

Hungary 10Y Yield vs Poland | Type: macro_line | Hungary 10Y %: 5.65 (2026-05-01) | Range: 2.84–10.25 | Trend(6pt): 2.84,10.25,6.17,6.67,6.27,5.65 | Poland 10Y %: 5.74 (2026-05-01) | Range: 1.6–7.82 | Trend(6pt): 1.6,7.82,5.21,5.83,5.58,5.74

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Inflation Rate Month-over-Month | 1.71 | - | 23:00 |

| Inflation Rate Year-over-Year | 32.61 | - | 23:00 |

| Friday (2026-07-03) | |||

| Inflation Rate Month-over-Month | 1.71 | - | 23:00 |

| Inflation Rate Year-over-Year | 32.61 | - | 23:00 |

- Poland June inflation fell to 2.5% y/y, below 2.7% consensus, easing NBP pressure.

- Turkey trade deficit narrowed to $5.61 bn while unemployment held at 8.2%.

- BIST 100 rose 0.51% and Poland 10Y yields climbed 2.87% amid mixed regional flows.

Yesterday's Recap

Poland’s preliminary June inflation printed 2.5% y/y, undershooting consensus and prior 3.1%, reflecting softer food and energy prices. The print reinforces NBP’s hold stance as real rates remain positive. Turkey’s final trade balance came in at -$5.61 bn, virtually in line with expectations, while the unemployment rate stayed at 8.2%.

Equity markets showed modest gains with BIST 100 advancing 0.51% and iShares Poland up 0.21%. EUR/PLN eased 0.05% to 4.29 while USD/TRY rose 0.07% to 46.69. Hungary 10Y yields dropped 9.89% as investors rotated into local bonds.

Poland’s June PMI slump dominated CEE headlines, contrasting with expanding Czech and Hungarian factory output.

The Day Ahead

Turkey will release June inflation data tonight, with both month-on-month and year-on-year prints due at 23:00 ET. Markets expect the figures to confirm the ongoing disinflation path after yesterday’s trade and labor releases. No other major data are scheduled across Poland, Czech Republic, Hungary or Romania.

Traders will monitor any CBRT commentary for signals on the next policy move. Regional FX and bond markets are likely to stay range-bound ahead of the print.

Other Economic Notes

Poland remains the largest CEE economy and continues to attract EU cohesion funds, with €66 mn allocated for fertilizer support to farmers. Regional energy import dependence on Russian gas keeps inflation vulnerable to external shocks. Hungary’s industrial output contraction highlights euro-area demand weakness affecting multiple CEE exporters.

Romania’s trade deficit narrowing supports BNR stability while Czech output stabilization leaves room for one further CNB cut.

Global Macro News

The ECB deposit rate sits at 2.25%, anchoring regional policy expectations. Eurozone unemployment holds at 6.70%, supporting steady external demand for CEE exports. Brent crude fell 1.38% to $70.58, easing imported inflation pressures across the region.

Gold rose 0.27% to $4,079.10 as a safe-haven bid persisted. Bitcoin gained 0.13%, reflecting broader risk appetite. <i>↓ p.2</i>