Eurozone Macro Daily(Beta Mode)

Stocks Rally on Tariff Rejection

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Euro Stoxx 50 | 6,131.31 | +1.18% |

| DAX | 25,260.69 | +0.87% |

| CAC 40 | 8,515.49 | +1.39% |

| EUR/USD | 1.18 | +0.52% |

| EUR/GBP | 0.87 | -0.02% |

| EUR/JPY | 182.50 | -0.06% |

| Gold | 5,181.30 | +2.41% |

| Brent Crude | 70.53 | -1.71% |

| Bitcoin | 65,327.77 | -3.94% |

| German 2Y Bund | - | - |

| German 10Y Bund | 2.81% | -0.27% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Eurozone equities surged on US tariff ruling relief, Euro Stoxx 50 up 1.18%.

- EUR/USD gained 0.52%, but Bund yields eased on mixed signals.

- Brent fell 1.71%, easing inflation pressures amid global volatility.

Yesterday's Recap

Eurozone markets closed higher on February 22, lifted by the US Supreme Court's rejection of President Trump's tariffs, reducing trade tensions and aiding exporters. The Euro Stoxx 50 rose 1.18% to 6,131.31, fueled by strong performances in German and French stocks. Germany's DAX increased 0.87% to 25,260.69, supported by positive manufacturing vibes.

France's CAC 40 climbed 1.39% to 8,515.49, boosted by luxury and services sectors. EUR/USD advanced 0.52% to 1.18 on dollar softness after US GDP weakness, while EUR/GBP dipped 0.02% to 0.87. EUR/JPY fell 0.06% to 182.50.

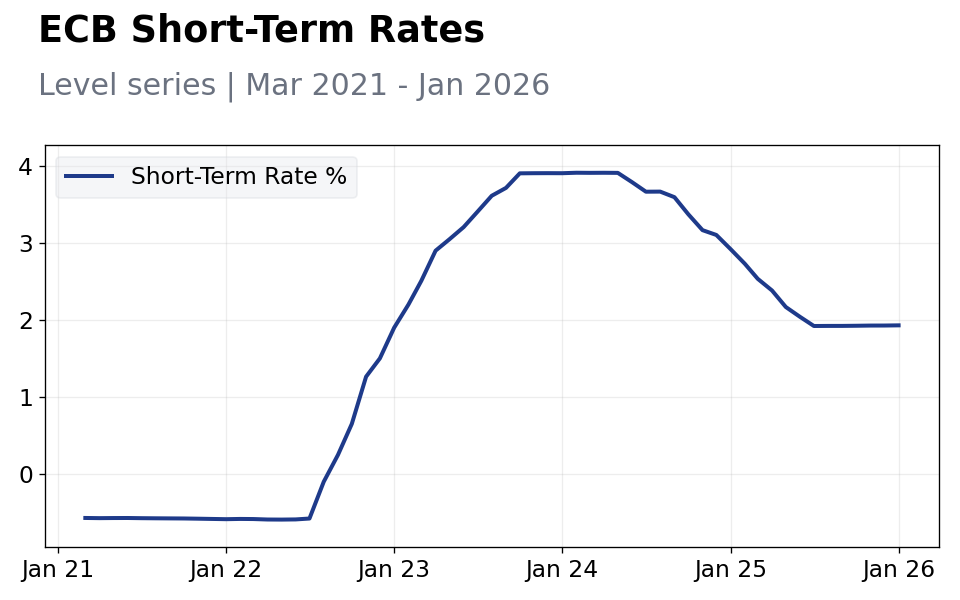

German 10-year Bund yields dropped 0.27% to 2.81%, reflecting dovish expectations from regional data. No key releases occurred, but steady Italian CPI at 2.1% y/y and Spanish unemployment at 11.2% helped peripheral bonds. The day underscored Eurozone equity strength despite external risks.

The Day Ahead

February 23 features a sparse calendar with no major Eurozone data, shifting focus to US tariff fallout and currency shifts. Traders eye potential ECB remarks on rates amid inflation trends. Italian budget news could sway BTP spreads.

Global risk mood may drive EUR pairs, with yen and pound in play. Trading volumes likely low before tomorrow's quiet day, though energy policy updates from Brussels might spark moves. Bund yields expected stable absent surprises.

Other Economic Notes

Eurozone recovery shows fragility, with German manufacturing gaining from exports but French services hiding wage strains. Italian debt near 140% of GDP challenges ECB policy transmission to Spain and others. Rising EU carbon prices elevate energy costs, risking higher CPI and hindering disinflation.

Global Macro News

Markets worldwide cheered the US tariff rejection, boosting European stocks by easing trade fears for exporters. US soft GDP and elevated inflation curbed Fed cut bets, aiding EUR/USD via yield gaps. Brent crude declined 1.71% to 70.53, lowering Eurozone import bills but signaling China demand woes that may hit German industry.

Gold rose 2.41% to 5,181.30 as a safe haven, shaping ECB risk views. (cont...)