Eurozone Macro Daily(Beta Mode)

Mixed Stocks, EUR Dips

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Euro Stoxx 50 | 6,116.60 | +0.04% |

| DAX | 24,991.97 | -1.06% |

| CAC 40 | 8,519.21 | +0.26% |

| EUR/USD | 1.18 | -0.49% |

| EUR/GBP | 0.87 | +0.02% |

| EUR/JPY | 182.66 | +0.03% |

| Gold | 5,160.50 | -0.85% |

| Brent Crude | 71.08 | -0.57% |

| Bitcoin | 64,098.80 | -0.80% |

| German 2Y Bund | - | - |

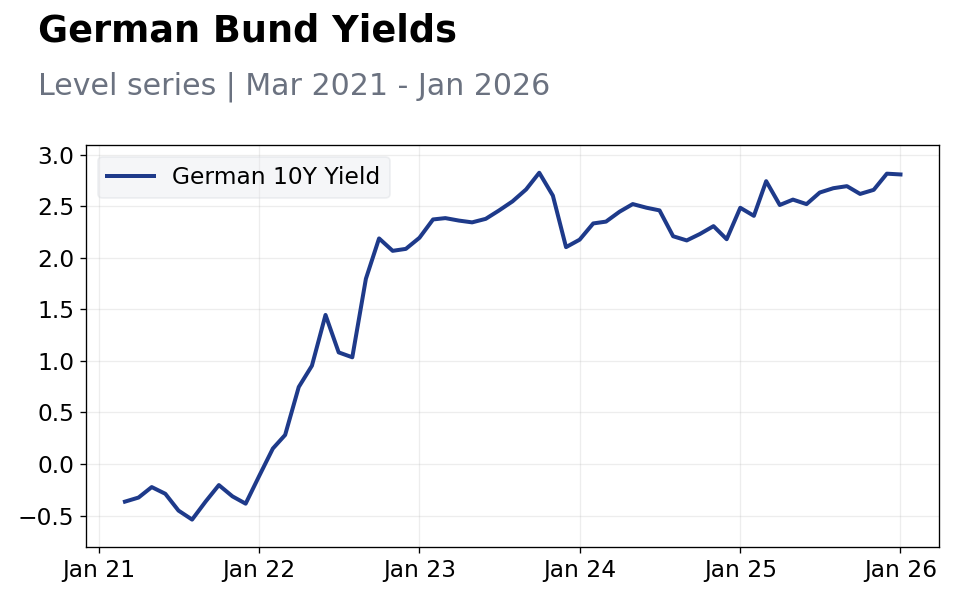

| German 10Y Bund | 2.81% | -0.27% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Eurozone equities showed mixed performance with Euro Stoxx 50 edging up slightly amid global tariff relief.

- EUR weakened against USD, reflecting broader dollar strength post-US court ruling.

- Bund yields declined modestly, signaling dovish ECB expectations.

Yesterday's Recap

Eurozone markets exhibited mixed movements yesterday with the Euro Stoxx 50 closing at 6,116.60, up 0.04%, driven by gains in French and Italian stocks offsetting German weakness. Germany's DAX fell 1.06% to 24,991.97, pressured by tech sector declines and lingering industrial concerns, while France's CAC 40 rose 0.26% to 8,519.21 on luxury goods resilience. The EUR/USD pair dropped 0.49% to 1.18, influenced by dollar gains following the US Supreme Court's tariff ruling, which boosted global risk appetite but weighed on the euro.

No major Eurozone data releases occurred, allowing markets to focus on external factors; however, prior German Ifo sentiment lingered in investor minds, supporting cautious Bund buying. Italian bond spreads widened slightly amid fiscal policy debates, while Spanish equities held steady without new employment figures. Overall, periphery markets like Italy and Spain showed relative stability compared to core declines in Germany.

The Day Ahead

Today features no scheduled Eurozone economic releases, shifting focus to broader market sentiment and potential ECB commentary. Investors will monitor any unscheduled statements from ECB officials, particularly on inflation trends in Germany and France. Attention may turn to Dutch consumer confidence indicators if ad-hoc data emerges, though none are planned.

Tomorrow's calendar is also empty, but anticipation builds for later-week events like potential Italian GDP revisions. Markets could react to global developments, including US economic data influencing EUR crosses.

Other Economic Notes

Broader Eurozone themes highlight persistent inflation divergences, with German core prices cooling faster than in France and Italy. Fiscal pressures in Italy and Spain continue to challenge debt sustainability, potentially widening bond spreads. Resilient services sectors in the Netherlands and France offer growth buffers amid manufacturing slowdowns.

Global Macro News

Global markets reacted positively to the US Supreme Court's ruling against sweeping tariffs, lifting Wall Street stocks and indirectly supporting Eurozone equities through reduced trade tensions. (cont...)