Eurozone Macro Daily(Beta Mode)

Stoxx Dips, DAX Edges Up

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Euro Stoxx 50 | 6,161.56 | -0.19% |

| DAX | 25,289.02 | +0.45% |

| CAC 40 | 8,620.93 | +0.72% |

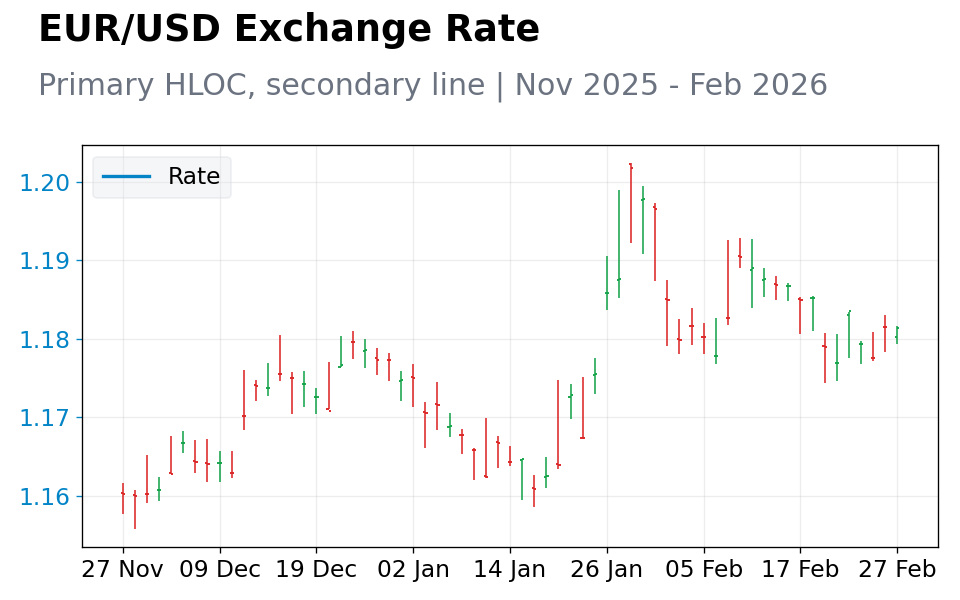

| EUR/USD | 1.18 | -0.02% |

| EUR/GBP | 0.88 | +0.50% |

| EUR/JPY | 184.54 | +0.55% |

| Gold | 5,210.90 | +0.66% |

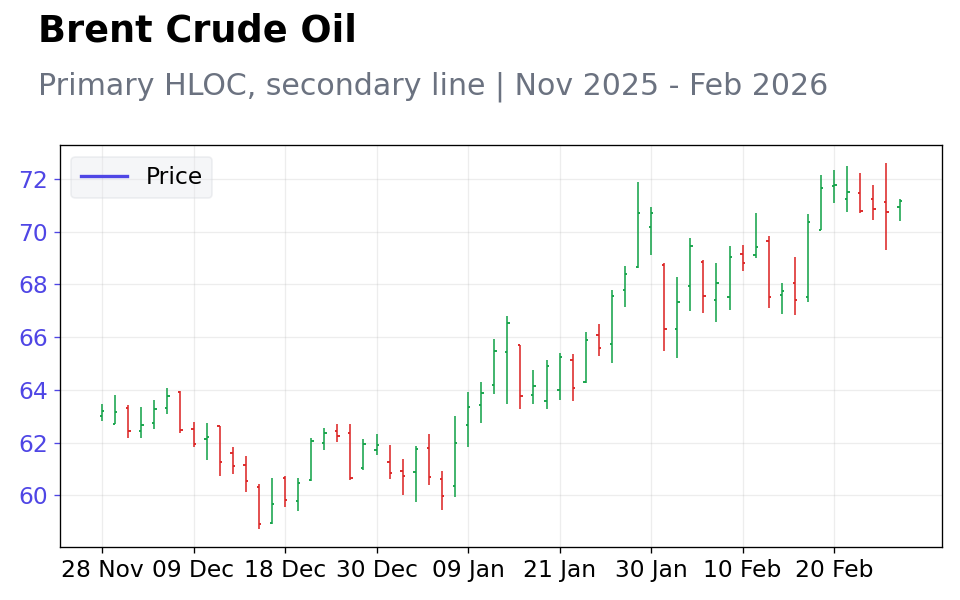

| Brent Crude | 71.17 | +0.59% |

| Bitcoin | 67,699.02 | -0.38% |

| German 2Y Bund | - | - |

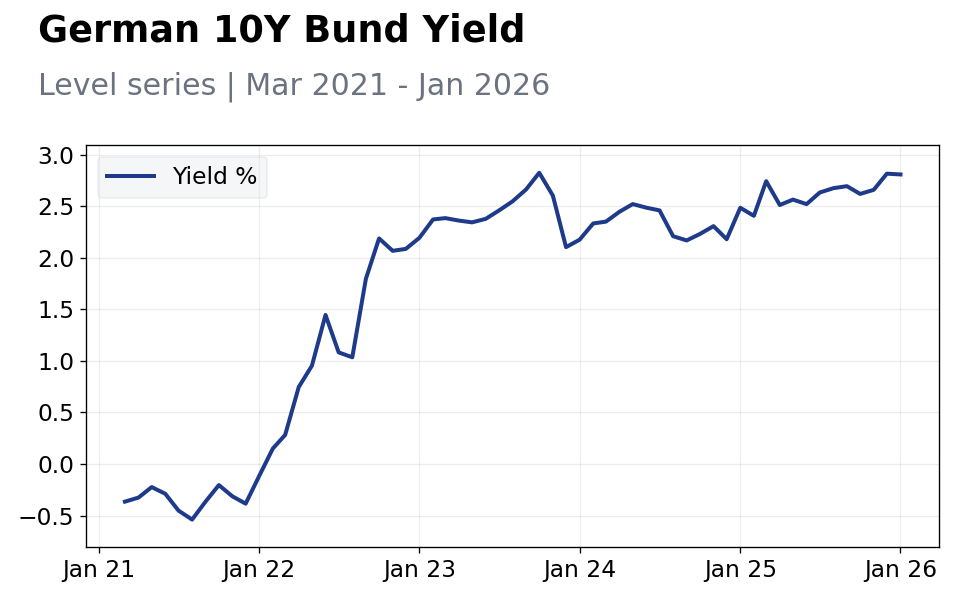

| German 10Y Bund | 2.81% | -0.27% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Eurozone equities mixed: Euro Stoxx 50 down 0.19% on tech weakness, DAX up 0.45% on auto gains, CAC 40 up 0.72% on luxury strength.

- Euro stable vs. dollar at 1.18 (-0.02%), but firmer vs. pound at 0.88 (+0.50%) and yen at 184.54 (+0.55%).

- German 10Y Bund yield fell to 2.81% (-0.27%), signaling bets on ECB caution amid inflation concerns.

Yesterday's Recap

Eurozone markets closed mixed on February 26, with the Euro Stoxx 50 down 0.19% at 6,161.56, pressured by tech sector declines after global earnings misses. Germany's DAX rose 0.45% to 25,289.02, lifted by automotive stocks like Volkswagen on positive export signals. France's CAC 40 gained 0.72% to 8,620.93, supported by luxury firms such as LVMH amid strong Asian demand.

The euro held steady against the dollar at 1.18 with a slight 0.02% drop, but advanced 0.50% versus the pound to 0.88 due to UK fiscal issues, and 0.55% against the yen to 184.54 on Japanese policy expectations. German 10Y Bund yields decreased 0.27% to 2.81%, reflecting market anticipation of delayed ECB rate cuts from persistent wage pressures. No significant data releases occurred, though earlier German Ifo business climate data at 87.0 sustained resilient sentiment despite manufacturing softness.

Italian bond spreads widened slightly, highlighting peripheral concerns over energy costs.

The Day Ahead

February 27 features a sparse calendar with no key Eurozone data due, giving markets time to assess recent inflation figures from France and Germany. Traders will watch for any impromptu ECB remarks on quantitative tightening, especially from Governing Council members. Focus may shift to EUR cross volatility driven by global risk mood and U.S.

indicators. Italian fiscal developments remain in view as budget plans could affect BTP spreads. Spanish jobs data, while not scheduled, might prompt analyst previews.

A calm day could heighten sensitivity to external events like U.S. tariff decisions.

Other Economic Notes

Inflation persists in France and Germany, with core CPI above 2% targets, straining consumer spending. Italian industrial production lags from elevated energy prices, unlike Spain's strengthening job market aiding growth. The Netherlands' trade surplus enhances bloc stability, but Eastern European geopolitical risks disrupt supply chains.