Eurozone Macro Daily(Beta Mode)

Equities Plunge on Soft Data

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Euro Stoxx 50 | 5,771.73 | -3.59% |

| DAX | 24,638.00 | -2.56% |

| CAC 40 | 8,103.84 | -3.46% |

| EUR/USD | 1.16 | -0.86% |

| EUR/GBP | 0.87 | -0.29% |

| EUR/JPY | 182.66 | -0.69% |

| Gold | 5,147.20 | -2.78% |

| Brent Crude | 82.00 | +5.48% |

| Bitcoin | 68,124.01 | -0.95% |

| German 2Y Bund | - | - |

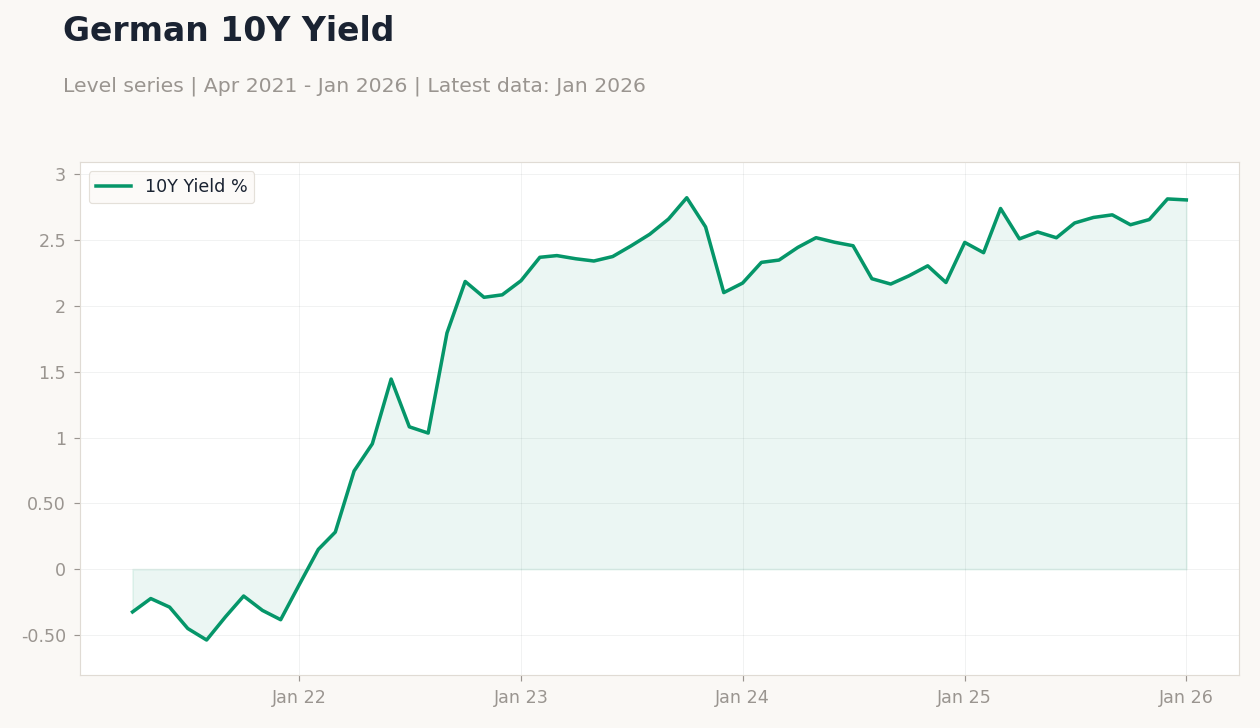

| German 10Y Bund | 2.81% | -0.27% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Retail Sales Month-over-Month | 1.20 | -0.20 | -0.90 |

| Retail Sales Year-over-Year | 2.50 | - | 1.20 |

| HCOB Manufacturing PMI | 49.20 | 50.10 | 50 |

| HCOB Manufacturing PMI | 48.10 | 49.50 | 50.60 |

| Full Year GDP Growth | 0.70 | - | 0.50 |

| Government Budget | -3.40 | - | -3.10 |

| Inflation Rate Year-over-Year Preliminary | 2.40 | - | 2.40 |

| Unemployment Level Change | 30,400 | 37,500 | 3,584 |

| Inflation Rate Year-over-Year Preliminary | 1 | - | 1.60 |

| Inflation Rate Month-over-Month Preliminary | 0.40 | 0.20 | 0.80 |

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| HCOB Services PMI | 53.50 | 52.80 | 22:15 |

| HCOB Services PMI | 52.90 | - | 22:45 |

| Headline Unemployment Rate | 5.60 | 5.60 | 23:00 |

| Industrial Production Month-over-Month | -0.70 | 0.50 | 21:45 |

| Retail Sales Month-over-Month | -0.80 | 0.20 | 23:00 |

| Factory Orders Month-over-Month | 7.80 | -4.30 | 21:00 |

- German retail sales disappointed, signaling consumer weakness amid high rates.

- Italian PMI surprised positively, but GDP growth revised lower.

- Markets tumbled, with Euro Stoxx down 3.59% on growth fears.

Yesterday's Recap

German retail sales fell 0.9% month-over-month in February, missing the consensus of -0.2% and down from 1.2% prior, while year-over-year growth slowed to 1.2% from 2.5%, highlighting consumer caution. Spain's HCOB Manufacturing PMI came in at 50.0, slightly below the expected 50.1 but up from 49.2, indicating stabilization. Italy's HCOB Manufacturing PMI beat expectations at 50.6 versus 49.5 forecast and 48.1 prior, suggesting manufacturing recovery.

Italian full-year GDP growth was revised to 0.5% from 0.7%, with the government budget improving to -3.1% from -3.4%, reflecting fiscal tightening. Netherlands inflation held steady at 2.4% year-over-year preliminary, matching prior, while Spanish unemployment change was a modest 3,584 increase, far below the 37,500 consensus and 30,400 prior. Italian preliminary inflation rose to 1.6% year-over-year, exceeding prior 1.0%, with month-over-month at 0.8% versus 0.2% expected.

Markets reacted sharply, with Euro Stoxx 50 dropping 3.59% to 5,771.73, DAX falling 2.56% to 24,638.00, CAC 40 declining 3.46% to 8,103.84, EUR/USD weakening 0.86% to 1.16, and German 10Y Bund yield easing 0.27% to 2.81%.

The Day Ahead

Spain's HCOB Services PMI is due at 22:15, with consensus at 52.8 from 53.5 prior, potentially signaling service sector slowdown. Italy's HCOB Services PMI follows at 22:45, lacking consensus but building on 52.9 prior, amid broader recovery hopes. Italian headline unemployment rate releases at 23:00, expected steady at 5.6%, which could influence wage dynamics.

French industrial production month-over-month arrives Tuesday at 21:45, forecasted at 0.5% rebound from -0.7%, key for manufacturing outlook. Italian retail sales month-over-month is set for Tuesday at 23:00, with 0.2% growth expected from -0.8% prior, testing consumer resilience. German factory orders month-over-month comes Wednesday at 21:00, with consensus at -4.3% from 7.8% prior, providing insights into industrial demand.

Other Economic Notes

Persistent inflation pressures in Italy and steady Dutch rates underscore challenges in achieving the ECB's 2% target, complicating monetary easing. Weak German retail and revised Italian GDP highlight uneven recovery across the Eurozone, with core economies lagging peripherals. (cont...)