Eurozone Macro Daily(Beta Mode)

German Data Misses, Oil Surges

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Euro Stoxx 50 | 5,685.20 | -0.61% |

| DAX | 23,591.03 | -0.94% |

| CAC 40 | 7,915.36 | -0.98% |

| EUR/USD | 1.16 | +0.80% |

| EUR/GBP | 0.86 | -0.16% |

| EUR/JPY | 182.55 | -0.17% |

| Gold | 5,174.10 | +0.54% |

| Brent Crude | 94.25 | +1.68% |

| Bitcoin | 70,082.05 | +6.23% |

| German 2Y Bund | - | - |

| German 10Y Bund | 2.81% | -0.27% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Factory Orders Month-over-Month | 6.40 | -4.30 | -11.10 |

| Industrial Production Month-over-Month | -1 | 0.90 | -0.50 |

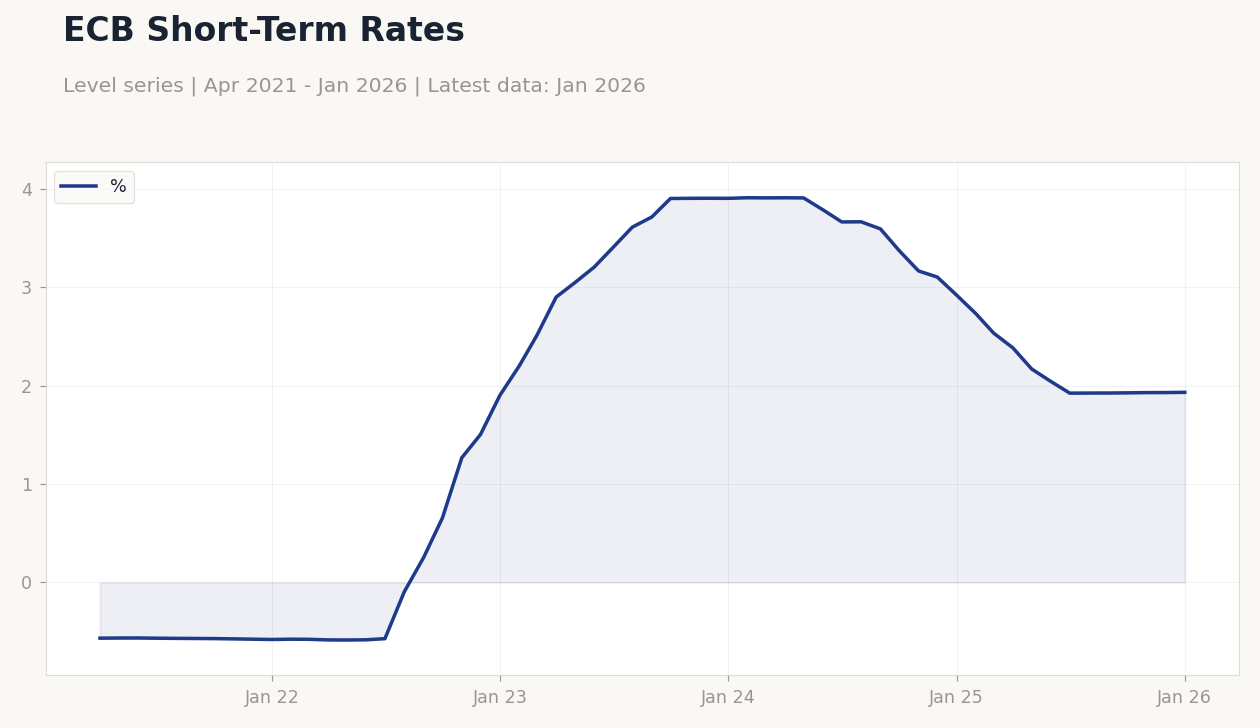

ECB Short-Term Rates | Type: macro_line | %: 1.932 (2026-01-01) | Range: -0.5847–3.909 | Trend(6pt): -0.5661,-0.5826,3.61,3.371,1.929,1.932

ECB Short-Term Rates | Type: macro_line | %: 1.932 (2026-01-01) | Range: -0.5847–3.909 | Trend(6pt): -0.5661,-0.5826,3.61,3.371,1.929,1.932

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Trade Balance | 17,100m | 15,200m | 23:00 |

| Exports Month-over-Month | 4 | - | 23:00 |

| Trade Balance | -4,800m | -4,600m | 23:45 |

| Wholesale Prices Month-over-Month | 0.90 | 0.40 | 23:00 |

| Wholesale Prices Year-over-Year | 1.20 | - | 23:00 |

| Industrial Production Month-over-Month | -0.40 | 0.20 | 01:00 |

- German factory orders and industrial production disappointed, signaling manufacturing weakness amid global tensions.

- Equities dipped while EUR strengthened; oil rallied on Iran conflict escalation.

- Geopolitical risks fuel inflation fears, pressuring ECB policy outlook.

Yesterday's Recap

German factory orders plunged 11.1% month-over-month, far below the consensus forecast of -4.3% and previous 6.4%, highlighting export sector vulnerabilities. German industrial production also missed, declining 0.5% month-over-month against expectations of 0.9% growth and prior -1%, exacerbating concerns over Europe's largest economy. Eurozone equities weakened, with the Euro Stoxx 50 down 0.61% to 5,685.20, the German DAX falling 0.94% to 23,591.03, and the French CAC 40 dropping 0.98% to 7,915.36, driven by risk-off sentiment.

The euro appreciated, with EUR/USD up 0.80% to 1.16, EUR/GBP down 0.16% to 0.86, and EUR/JPY slipping 0.17% to 182.55, reflecting safe-haven flows. Brent crude surged 1.68% to 94.25 amid Iran war disruptions, while German 10-year Bund yields eased 0.27% to 2.81%, signaling flight to quality. No major data emerged from France, Italy, or Spain, but broader market moves underscored Eurozone exposure to energy shocks.

The Day Ahead

German trade balance data, a high-impact release, is due with consensus expecting 15.2 billion euros versus previous 17.1 billion, potentially revealing export trends amid global disruptions. German exports month-over-month follow, with prior 4% growth but no consensus, offering insights into manufacturing resilience. French trade balance arrives mid-morning, forecasted at -4.6 billion euros improving from -4.8 billion, amid domestic demand concerns.

Later, German wholesale prices month-over-month and year-over-year are slated, with MoM consensus at 0.4% from 0.9% prior, signaling input cost pressures. Italian industrial production month-over-month rounds out the day, expected at 0.2% versus -0.4% previous, critical for assessing southern Eurozone recovery.

Other Economic Notes

Broader Eurozone themes highlight inflation resurgence compounded by oil surges from Middle East strife. A German survey shows 53% favoring delaying climate neutrality from 2045 to 2050, potentially easing fiscal pressures but risking green transition delays. Unemployment remains steady at 6.70% based on latest available figures, supporting consumer spending yet vulnerable to energy-driven slowdowns.