Eurozone Macro Daily(Beta Mode)

ZEW Sentiment Plunges Amid Geopolitical Tensions

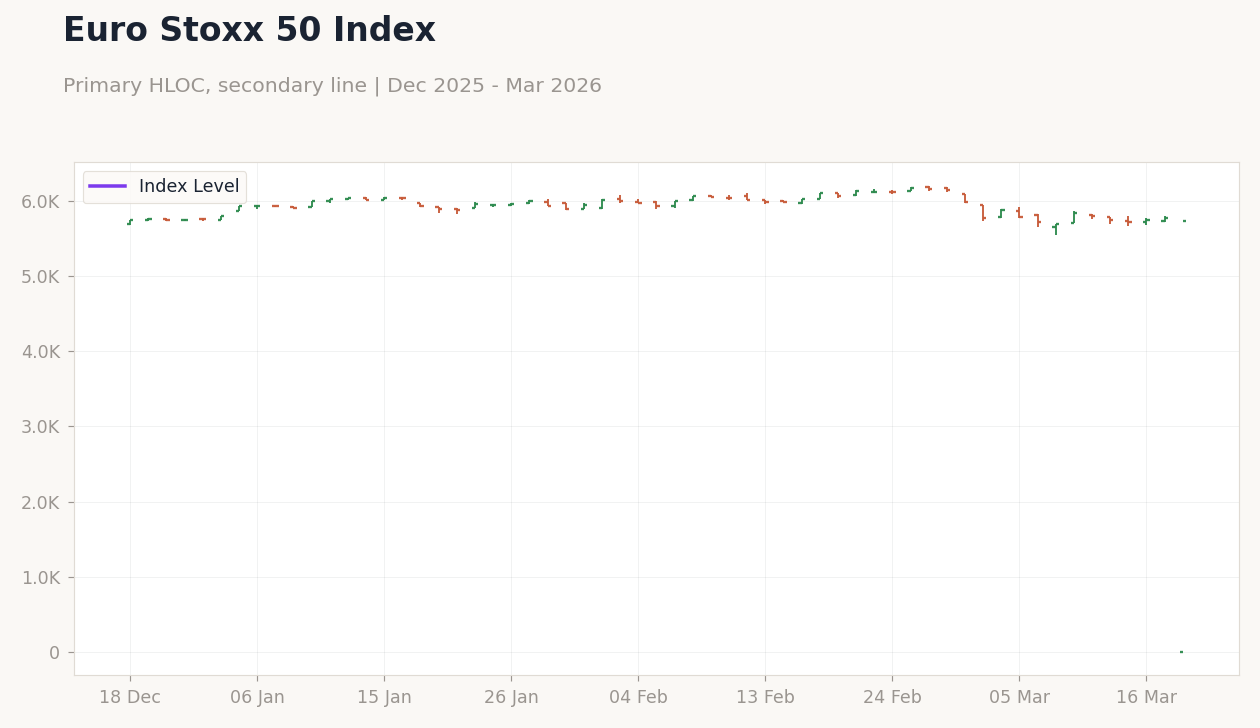

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Euro Stoxx 50 | 5,736.85 | -0.56% |

| DAX | 23,730.92 | +0.71% |

| CAC 40 | 7,969.88 | -0.06% |

| EUR/USD | 1.15 | -0.59% |

| EUR/GBP | 0.86 | +0.03% |

| EUR/JPY | 183.11 | -0.14% |

| Gold | 4,848.20 | -0.85% |

| Brent Crude | 106.86 | -0.48% |

| Bitcoin | 70,851.50 | -4.15% |

| German 2Y Bund | - | - |

| German 10Y Bund | 2.81% | -0.27% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| ZEW Economic Sentiment Index | 58.30 | 39 | -0.50 |

DAX Index | Type: market_hloc | Index Level: 2.35e+04 (2026-03-18) | Range: 2.341e+04–2.542e+04 | Trend(5pt): 2.42e+04,2.535e+04,2.449e+04,2.529e+04,2.35e+04

DAX Index | Type: market_hloc | Index Level: 2.35e+04 (2026-03-18) | Range: 2.341e+04–2.542e+04 | Trend(5pt): 2.42e+04,2.535e+04,2.449e+04,2.529e+04,2.35e+04

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Headline Unemployment Rate | 4 | - | 21:30 |

| Producer Price Index Year-over-Year | -3 | -2.70 | 23:00 |

| Trade Balance | 6,037m | 5,650m | 01:00 |

- German ZEW index fell sharply to -0.5, missing consensus of 39, highlighting pessimism from Middle East tensions.

- Markets mixed: Euro Stoxx 50 down 0.56%, DAX up 0.71%, EUR/USD slips 0.59% to 1.15.

- ECB eyes energy shocks; Lagarde denies imminent exit, De Guindos warns of policy shifts if Iran conflict persists.

Yesterday's Recap

Germany's ZEW Economic Sentiment Index dropped to -0.5 in March, well below consensus of 39 and down from 58.3 prior, underscoring concerns over geopolitical risks and energy disruptions. This weak data weighed on European stocks, with the Euro Stoxx 50 falling 0.56% to 5,736.85 amid risk aversion. Germany's DAX bucked the trend, rising 0.71% to 23,730.92, lifted by industrial sector strength.

France's CAC 40 dipped 0.06% to 7,969.88, as luxury stocks provided some support but caution dominated. The euro softened against peers, with EUR/USD declining 0.59% to 1.15 on dollar gains, EUR/GBP edging up 0.03% to 0.86, and EUR/JPY falling 0.14% to 183.11. German 10-year Bund yields decreased 0.27% to 2.81%, reflecting safe-haven demand amid the ZEW miss and global uncertainties.

No other significant Eurozone data was released, shifting focus to the sentiment decline's impact on growth in major economies like Germany and France.

The Day Ahead

Key releases include the Netherlands' headline unemployment rate at 21:30 ET, with prior at 4%, providing clues on labor market health amid slowdown worries. Germany's producer price index year-over-year follows at 23:00 ET, consensus -2.7% versus -3% previous, which may indicate softening input costs for the bloc's biggest economy. Italy's trade balance arrives at 01:00 ET on March 20, expected at €5.65 billion against €6.037 billion prior, shedding light on export trends in the third-largest economy.

These medium-impact indicators could affect ECB rate expectations if they point to disinflation. Markets may also watch for ECB commentary on geopolitical developments. No high-impact events are slated, directing attention to these for market direction.

Other Economic Notes

Austria's HICP rose to 2.3%, drawing ECB attention to varying inflation trends across countries like Germany and France. Supply chain issues persist, with China's lead in Industry 4.0 technologies—such as supply chain transparency, digital twins, automation, and AI—challenging European competitiveness in sectors like tech and manufacturing in the Netherlands and Germany. The ECB deposit rate stands at 2.00% as of March 18, balancing disinflation against external risks.