Eurozone Macro Daily(Beta Mode)

PMIs Soften, Equities Edge Up

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Euro Stoxx 50 | 5,581.29 | +0.13% |

| DAX | 22,653.86 | +1.22% |

| CAC 40 | 7,743.92 | +0.23% |

| EUR/USD | 1.16 | -0.05% |

| EUR/GBP | 0.86 | -0.29% |

| EUR/JPY | 184.26 | +0.18% |

| Gold | 4,568.70 | +3.85% |

| Brent Crude | 99.31 | -4.96% |

| Bitcoin | 70,810.71 | -0.15% |

| German 2Y Bund | - | - |

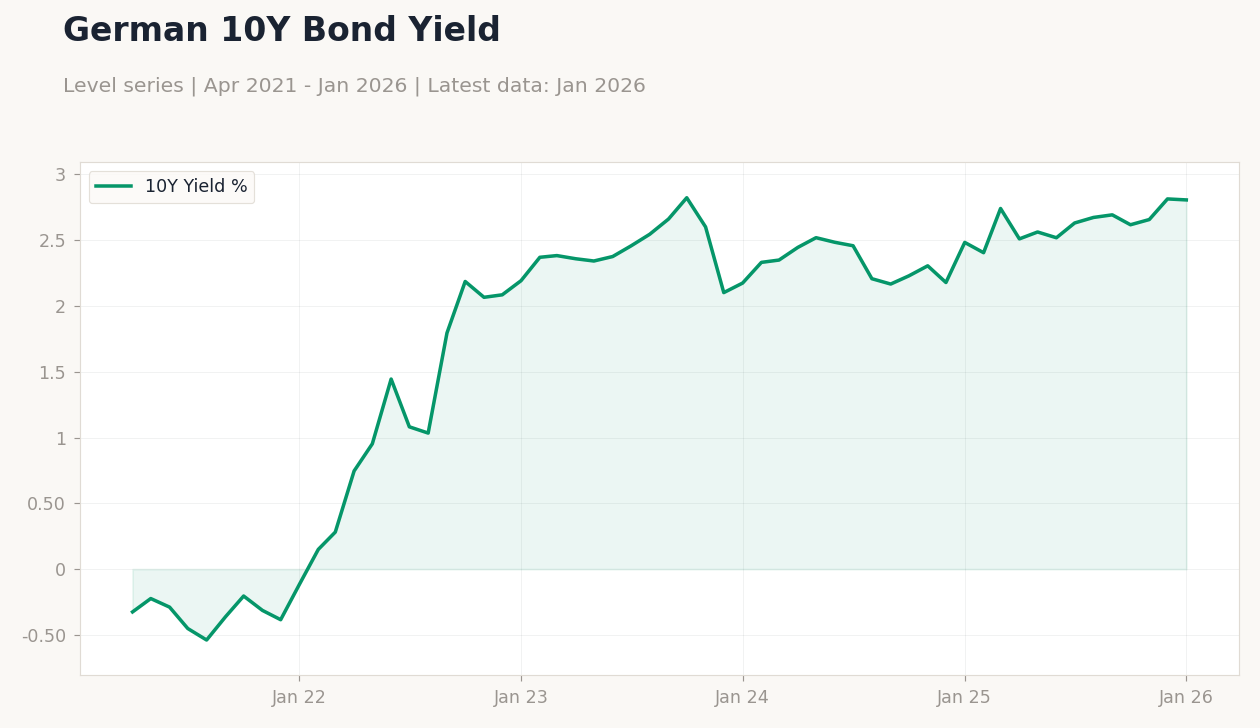

| German 10Y Bund | 2.81% | -0.27% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Consumer Confidence Index | -24 | - | -30 |

| Trade Balance | -5,570m | - | -4,000m |

| HCOB Composite PMI Flash | 49.90 | 49.30 | 48.30 |

| HCOB Manufacturing PMI Flash | 50.10 | 49.50 | 50.20 |

| HCOB Services PMI Flash | 49.60 | 49 | 48.30 |

| HCOB Manufacturing PMI Flash | 50.90 | 49.40 | - |

| S&P Global Manufacturing PMI Flash | 50.90 | 49.50 | 51.70 |

| HCOB Composite PMI Flash | 53.20 | 51.80 | - |

| HCOB Services PMI Flash | 53.50 | 52 | - |

| S&P Global Composite PMI Flash | 53.20 | 52 | 51.90 |

Eurozone Short-Term Rates | Type: macro_line | Short-Term Rate %: 1.932 (2026-01-01) | Range: -0.5847–3.909 | Trend(6pt): -0.5661,-0.5826,3.61,3.371,1.929,1.932

Eurozone Short-Term Rates | Type: macro_line | Short-Term Rate %: 1.932 (2026-01-01) | Range: -0.5847–3.909 | Trend(6pt): -0.5661,-0.5826,3.61,3.371,1.929,1.932

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Ifo Business Climate | 88.60 | 85.50 | 01:00 |

| GFK Consumer Confidence Index | -24.70 | -26.50 | 23:00 |

| Business Confidence Index | 102 | 100 | 23:45 |

| Consumer Confidence Index | 91 | 89 | 23:45 |

| Business Confidence Index | 88.50 | - | 01:00 |

| Consumer Confidence Index | 97.40 | - | 01:00 |

| Inflation Rate Month-over-Month Preliminary | 0.40 | - | 00:00 |

| Inflation Rate Year-over-Year Preliminary | 2.30 | 2.40 | 00:00 |

| Unemployment Benefit Claims | -26,900 | - | 03:00 |

- Eurozone PMIs weakened in March, with French composite at 48.3 missing consensus, signaling contraction, while German manufacturing beat at 51.7 amid mixed signals.

- Stocks rose modestly, DAX leading with 1.22% gain to 22,653.86, as weak data fueled ECB cut hopes; EUR/USD eased 0.05% to 1.16.

- Energy shocks and stagflation risks pressured sentiment, gold jumping 3.85% to 4,568.70 as safe haven, Brent crude down 4.96% to 99.31.

Yesterday's Recap

Eurozone markets delivered mixed results amid soft PMI readings heightening slowdown worries. France's HCOB Composite PMI Flash declined to 48.3, under consensus 49.3 and prior 49.9, pointing to contraction. French HCOB Manufacturing PMI Flash rose slightly to 50.2, topping consensus 49.5 from 50.1, but Services PMI Flash fell to 48.3 versus expected 49 from 49.6.

Germany's S&P Global Manufacturing PMI Flash climbed to 51.7, exceeding consensus 49.5 and previous 50.9, though S&P Global Composite PMI Flash dipped to 51.9 against consensus 52 from 53.2, with Services at 51.2 below anticipated 52.5 from 53.5. Netherlands Consumer Confidence Index deteriorated to -30.0 from -24.0, while Spain's Trade Balance narrowed to -4 billion euros from -5.57 billion. Equities advanced, Euro Stoxx 50 up 0.13% to 5,581.29, DAX up 1.22% to 22,653.86, CAC 40 up 0.23% to 7,743.92.

German 10Y Bund yield dropped 0.27% to 2.81%. EUR/USD fell 0.05% to 1.16, EUR/GBP declined 0.29% to 0.86, EUR/JPY increased 0.18% to 184.26.

The Day Ahead

Focus shifts to Germany's Ifo Business Climate at 01:00 ET, projected at 85.5 from prior 88.6, a vital sentiment indicator amid manufacturing challenges. Germany's GfK Consumer Confidence arrives at 23:00 ET, expected at -26.5 versus previous -24.7, possibly reflecting energy-related gloom. France's Business Confidence at 23:45 ET is forecast at 100 from 102, with Consumer Confidence at 89 from 91, both key for evaluating demand.

Italy's Business Confidence and Consumer Confidence at 01:00 ET will offer peripheral economy views. These data points may shape ECB rate outlooks, especially with stagflation concerns. No ECB speeches or decisions are planned, directing attention to releases.

Other Economic Notes

Eurozone faces growing stagflation risks as March PMIs eased alongside energy price strains from Middle East tensions. Germany's call for gas firms to diversify beyond US LNG highlights supply risks, potentially eased by robust French nuclear output stabilizing power markets. (cont...)