Eurozone Macro Daily(Beta Mode)

Spanish Jobs Surge, PMIs Diverge

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Euro Stoxx 50 | 5,692.86 | -0.70% |

| DAX | 22,680.04 | +0.52% |

| CAC 40 | 7,962.39 | -0.24% |

| EUR/USD | 1.17 | +1.19% |

| EUR/GBP | 0.87 | -0.20% |

| EUR/JPY | 184.89 | +0.32% |

| Gold | 4,827.60 | +3.66% |

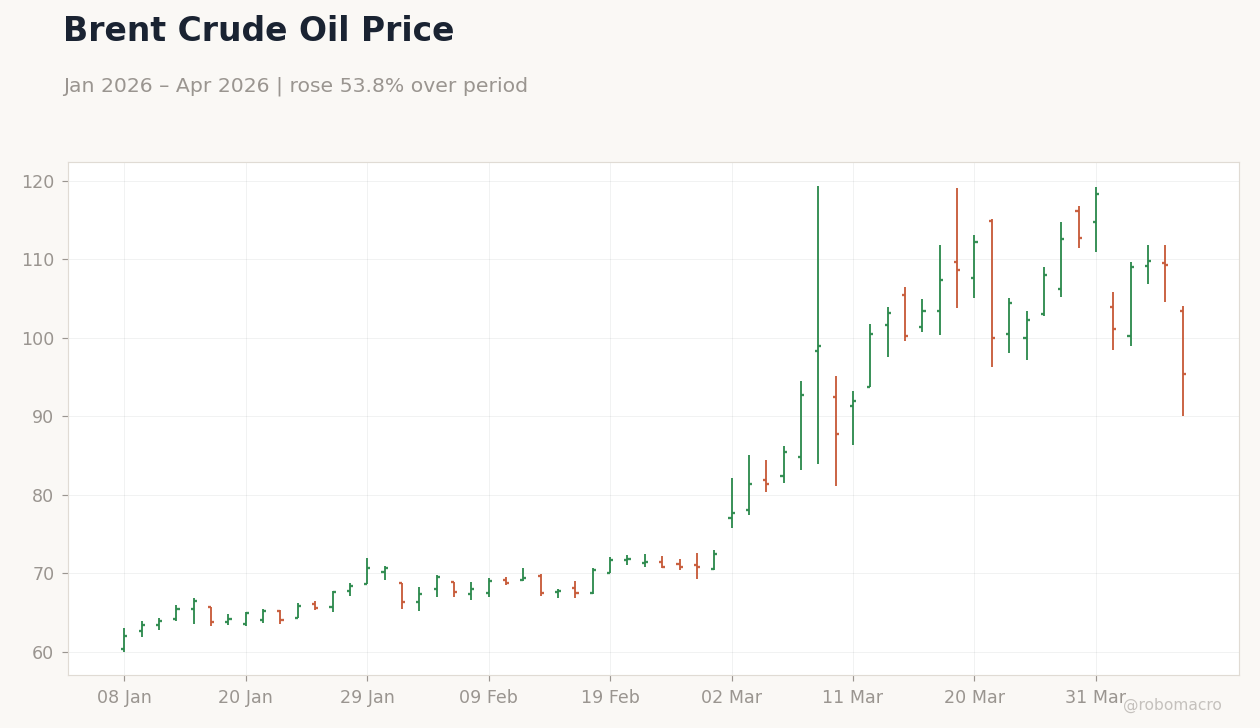

| Brent Crude | 95.73 | -12.39% |

| Bitcoin | 71,613.61 | +4.00% |

| German 2Y Bund | - | - |

| German 10Y Bund | 2.81% | -0.27% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Unemployment Level Change | 3,600 | 10.30 | -22,900 |

| S&P Global Services PMI | 51.90 | 50.80 | 53.30 |

| S&P Global Services PMI | 52.30 | - | 48.80 |

German 10Y Yield | Type: macro_line | 10Y Yield (%): 2.807 (2026-01-01) | Range: -0.5386–2.823 | Trend(5pt): -0.2235,1.082,2.661,2.306,2.807 | Italian 10Y Yield (%): 3.388 (2026-02-01) | Range: 0.628–4.885 | Trend(6pt): 0.984,3.359,4.513,3.569,3.492,3.388

German 10Y Yield | Type: macro_line | 10Y Yield (%): 2.807 (2026-01-01) | Range: -0.5386–2.823 | Trend(5pt): -0.2235,1.082,2.661,2.306,2.807 | Italian 10Y Yield (%): 3.388 (2026-02-01) | Range: 0.628–4.885 | Trend(6pt): 0.984,3.359,4.513,3.569,3.492,3.388

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Factory Orders Month-over-Month | -11.10 | 2 | 22:00 |

| Trade Balance | -1,800m | 2,300m | 22:45 |

| Trade Balance | 21,200m | 18,500m | 22:00 |

| Exports Month-over-Month | -2.30 | - | 22:00 |

| Industrial Production Month-over-Month | -0.50 | 0.90 | 22:00 |

| Industrial Production Month-over-Month | -0.60 | 0.50 | 00:00 |

- Spanish unemployment fell sharply to -22,900, beating consensus of 10.3 and previous 3,600.

- Spanish Services PMI rose to 53.3, exceeding consensus 50.8 and prior 51.9, signaling expansion.

- Italian Services PMI dropped to 48.8 from 52.3, indicating contraction amid Eurozone slowdown.

Yesterday's Recap

Eurozone markets displayed mixed results yesterday, with the Euro Stoxx 50 falling 0.70% to 5,692.86 due to risk-off sentiment, while the DAX gained 0.52% to 22,680.04 driven by tech advances. The CAC 40 dipped 0.24% to 7,962.39, dragged by utilities. Key data included Spain's unemployment level change at -22,900, significantly better than the consensus 10.3 and previous 3,600, reflecting strong labor market momentum.

Spain's S&P Global Services PMI climbed to 53.3, surpassing the consensus 50.8 and prior 51.9, highlighting services sector growth. In contrast, Italy's S&P Global Services PMI declined to 48.8 from 52.3, with no consensus available, pointing to contraction. Currency moves saw EUR/USD up 1.19% to 1.17 on dollar softness, EUR/GBP down 0.20% to 0.87, and EUR/JPY up 0.32% to 184.89.

German 10Y Bund yields fell 0.27% to 2.81%. The releases underscored regional divergences, with Spanish resilience countering Italian softness, though equities stayed cautious overall.

The Day Ahead

Focus shifts to German indicators today, beginning with Factory Orders month-over-month at 22:00 ET, expected at 2% following -11.1% previously. France's Trade Balance at 22:45 ET is projected at €2.3 billion, improving from -€1.8 billion prior. Germany's Trade Balance at 22:00 ET is forecasted at €18.5 billion, down from €21.2 billion, with Exports month-over-month (previous -2.3%, no consensus) and Industrial Production month-over-month at 0.9% from -0.5%.

Italy's Industrial Production month-over-month closes at 00:00 ET, anticipated at 0.5% after -0.6%. Positive German outcomes could support the euro and stocks, while disappointments may heighten ECB rate cut bets. No ECB speakers are lined up, directing attention to data impacts.

Other Economic Notes

Energy dynamics remain volatile, as Germany's power prices turned deeply negative from a renewables surge and low demand, exposing supply mismatches. Fuel costs in Germany hit averages of 2.5 euros per liter for diesel. Fiscal debates intensify, with Germany resisting France's deficit proposals and Italy's Meloni highlighting US tariff risks.

(cont...)