Eurozone Macro Daily(Beta Mode)

PMIs Mixed, Stocks Slide

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Euro Stoxx 50 | 5,633.22 | -1.05% |

| DAX | 22,921.59 | -1.06% |

| CAC 40 | 7,908.74 | -0.67% |

| EUR/USD | 1.17 | -0.14% |

| EUR/GBP | 0.87 | -0.16% |

| EUR/JPY | 185.20 | -0.15% |

| Gold | 4,744.00 | -0.12% |

| Brent Crude | 97.13 | +2.51% |

| Bitcoin | 70,766.54 | -1.63% |

| German 2Y Bund | - | - |

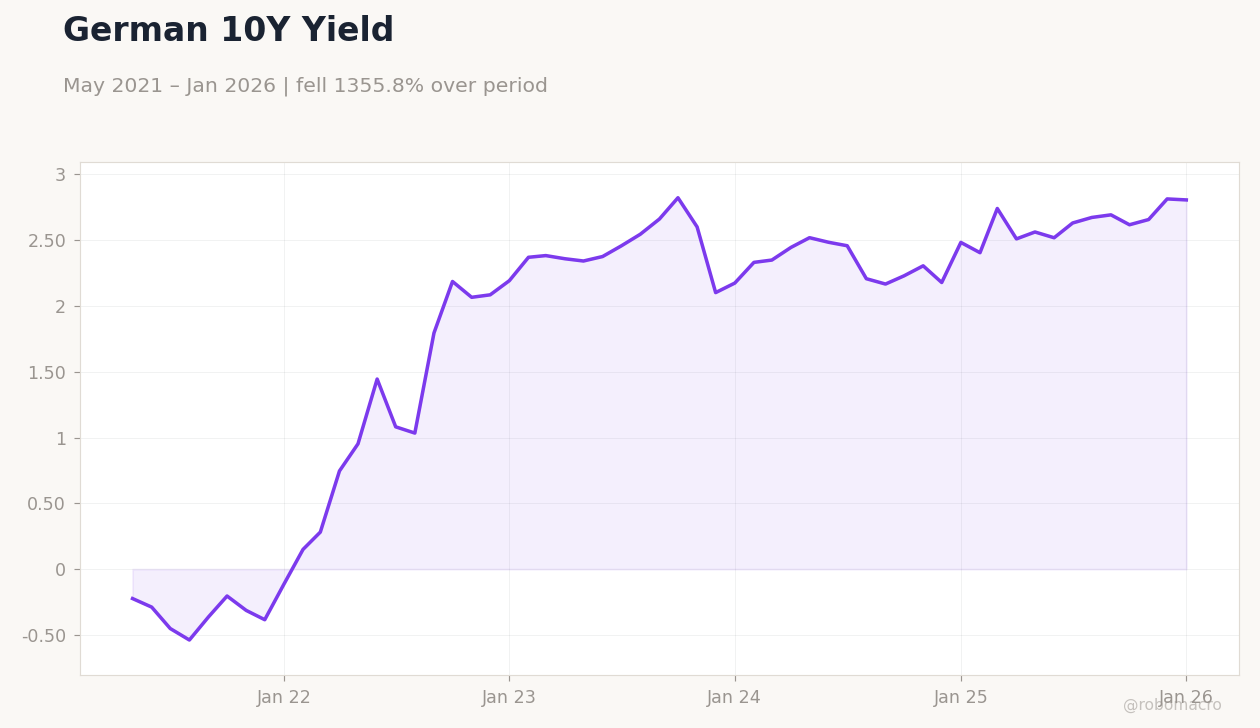

| German 10Y Bund | 2.81% | -0.27% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Unemployment Level Change | 3,600 | 10.30 | -22,900 |

| S&P Global Services PMI | 51.90 | 50.80 | 53.30 |

| S&P Global Services PMI | 52.30 | - | 48.80 |

| Factory Orders Month-over-Month | -11.10 | 2 | 0.90 |

| Trade Balance | -2,000m | -2,400m | -5,800m |

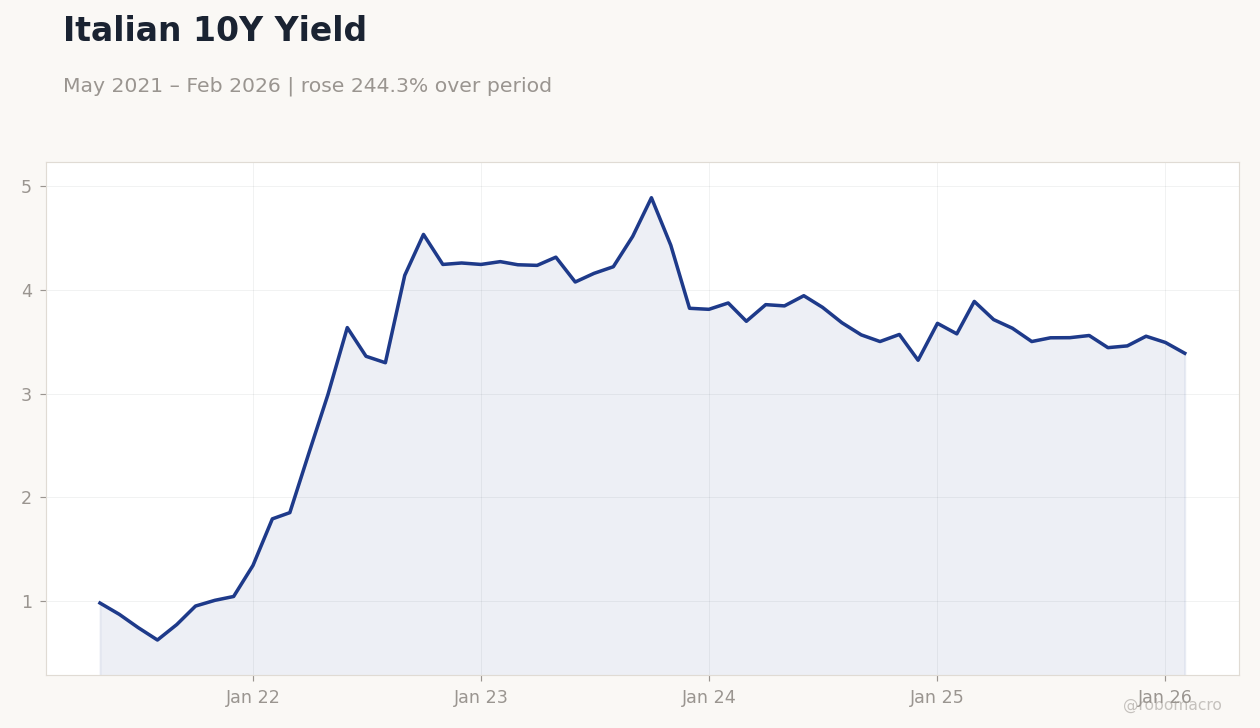

Italian 10Y Yield | Type: macro_line | Italian 10Y Yield (%): 3.388 (2026-02-01) | Range: 0.628–4.885 | Trend(6pt): 0.984,3.359,4.513,3.569,3.492,3.388

Italian 10Y Yield | Type: macro_line | Italian 10Y Yield (%): 3.388 (2026-02-01) | Range: 0.628–4.885 | Trend(6pt): 0.984,3.359,4.513,3.569,3.492,3.388

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Trade Balance | 21,200m | 18,500m | 22:00 |

| Exports Month-over-Month | -2.30 | - | 22:00 |

| Industrial Production Month-over-Month | -0.50 | 0.90 | 22:00 |

| Industrial Production Month-over-Month | -0.60 | 0.50 | 00:00 |

- Spanish jobs and services PMI beat expectations, signaling resilience in southern Eurozone economies amid broader slowdown.

- Italian PMI contraction and French trade deficit miss weighed on sentiment, contributing to equity declines.

- German factory orders underwhelmed, pressuring Bund yields lower as markets eye ECB policy path.

Yesterday's Recap

Spanish unemployment levels dropped sharply by 22,900, far better than the consensus expectation of a 10,300 rise, highlighting labor market strength despite economic headwinds. Spain's S&P Global Services PMI rose to 53.3, exceeding the consensus of 50.8 and indicating expansion in services activity. Italy's S&P Global Services PMI fell to 48.8 from 52.3 prior, signaling contraction and raising concerns over domestic demand weakness.

German factory orders increased 0.9% month-over-month, missing the consensus of 2% but improving from the previous -11.1% plunge. France's trade balance deteriorated to -5.8 billion euros, worse than the consensus forecast of -2.4 billion and prior -2 billion, underscoring export challenges. Eurozone equities declined, with the Euro Stoxx 50 down 1.05% to 5,633.22, the DAX falling 1.06% to 22,921.59, and the CAC 40 slipping 0.67% to 7,908.74, amid mixed data and global risk-off sentiment.

The euro weakened against major crosses, with EUR/USD down 0.14% to 1.17, while German 10-year Bund yields eased 0.27% to 2.81%, reflecting safe-haven flows.

The Day Ahead

Germany's trade balance data, due at 22:00 ET, is expected to show a surplus of 18.5 billion euros, down from 21.2 billion prior, potentially influencing euro sentiment if exports underperform. Accompanying German exports month-over-month lack a consensus but follow a prior -2.3% drop, with focus on global demand signals. German industrial production month-over-month, forecasted at 0.9% versus prior -0.5%, could bolster growth narratives if it beats estimates.

Italy's industrial production month-over-month, expected at 0.5% after -0.6% prior, will provide insights into manufacturing recovery amid weak PMI readings. These releases may drive volatility in Bund yields and DAX futures. No major ECB events are scheduled, keeping markets attuned to data for policy clues.

Other Economic Notes

BNP Paribas warns that weak Eurozone demand is offsetting supply constraints, risking a prolonged slowdown unless consumption rebounds. Commerzbank highlights intensifying oil shocks pressuring ECB inflation expectations, complicating the disinflation path. (cont...)