Eurozone Macro Daily(Beta Mode)

German Trade Beats, PMIs Mixed

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Euro Stoxx 50 | 5,896.29 | -0.29% |

| DAX | 24,080.63 | +5.06% |

| CAC 40 | 8,245.80 | -0.22% |

| EUR/USD | 1.17 | +0.31% |

| EUR/GBP | 0.87 | -0.18% |

| EUR/JPY | 184.96 | -0.28% |

| Gold | 4,787.80 | -0.09% |

| Brent Crude | 96.55 | +0.66% |

| Bitcoin | 72,057.95 | +1.31% |

| German 2Y Bund | - | - |

| German 10Y Bund | 2.81% | -0.27% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Unemployment Level Change | 3,600 | 10.30 | -22,900 |

| S&P Global Services PMI | 51.90 | 50.80 | 53.30 |

| S&P Global Services PMI | 52.30 | - | 48.80 |

| Factory Orders Month-over-Month | -11.10 | 2 | 0.90 |

| Trade Balance | -2,000m | -2,400m | -5,800m |

| Trade Balance | 20,300m | 18,500m | 19,800m |

| Exports Month-over-Month | -1.50 | - | 3.60 |

| Industrial Production Month-over-Month | 0 | 0.90 | -0.30 |

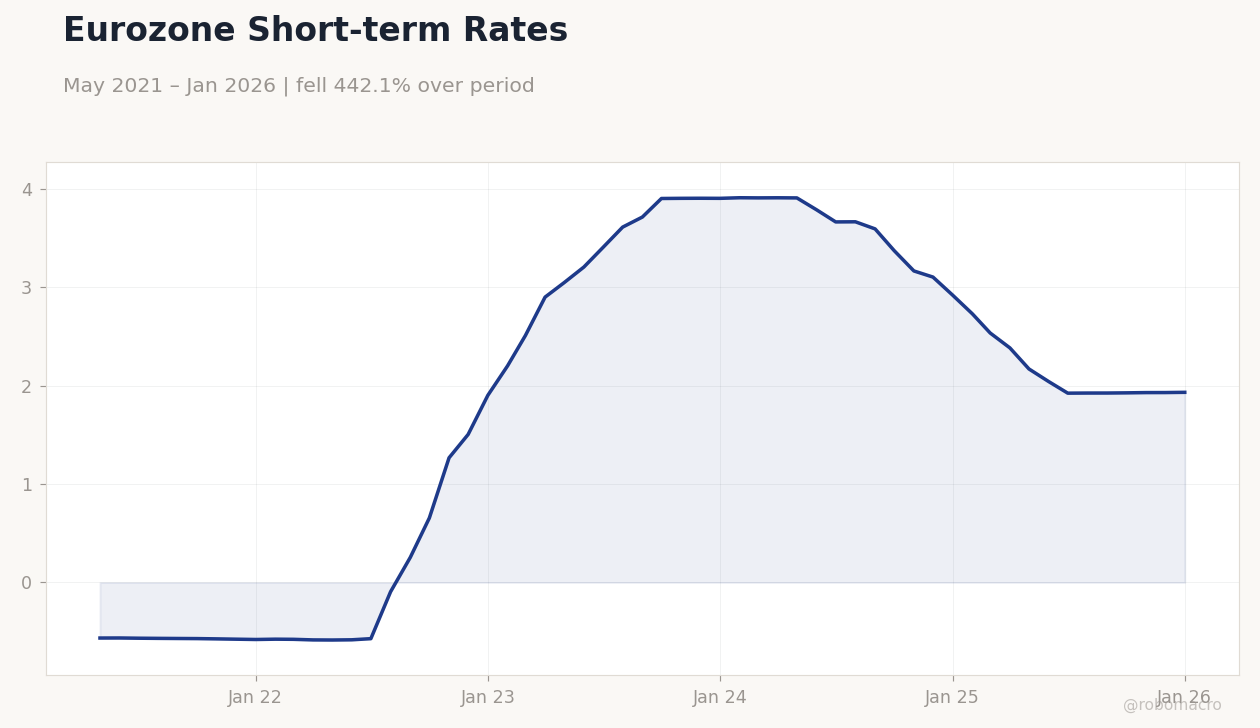

Eurozone Short-term Rates | Type: macro_line | Short-term Rate (%): 1.932 (2026-01-01) | Range: -0.5847–3.909 | Trend(5pt): -0.5647,-0.5711,3.713,3.165,1.932

Eurozone Short-term Rates | Type: macro_line | Short-term Rate (%): 1.932 (2026-01-01) | Range: -0.5847–3.909 | Trend(5pt): -0.5647,-0.5711,3.713,3.165,1.932

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Industrial Production Month-over-Month | -0.60 | 0.50 | 00:00 |

- Spanish unemployment fell sharply while services PMI beat expectations, signaling labor market resilience.

- Italian services PMI disappointed, contrasting with Germany's solid trade surplus and export growth.

- French trade deficit widened unexpectedly, and German industrial production missed forecasts amid mixed factory orders.

Yesterday's Recap

Eurozone markets showed divergence as the Euro Stoxx 50 dipped 0.29% to 5,896.29, while Germany's DAX surged 5.06% to 24,080.63 on strong trade data. Spain reported a sharp unemployment level change of -22,900, far better than the consensus of 10.3, and its S&P Global Services PMI rose to 53.3 against expectations of 50.8. Italy's S&P Global Services PMI fell to 48.8, below the previous 52.3, indicating contraction in services.

Germany's factory orders grew 0.9% month-over-month, missing the consensus of 2% after a prior -11.1%, but its trade balance expanded to €19.8 billion, beating forecasts of €18.5 billion, with exports up 3.6%. France's trade balance deteriorated to -€5.8 billion, worse than the expected -€2.4 billion. German industrial production declined 0.3% month-over-month, against consensus of 0.9%.

Overall, EUR/USD strengthened 0.31% to 1.17, reflecting euro resilience amid global risk sentiment.

The Day Ahead

Attention turns to Italy's industrial production data at 00:00 ET, with consensus expecting a 0.5% month-over-month rise after a prior -0.6%. This release could provide insights into the manufacturing sector's momentum in the Eurozone's third-largest economy. No other major Eurozone events are scheduled, allowing markets to digest yesterday's mixed data.

Traders will monitor any ECB commentary or peripheral news that might influence rate expectations. Broader focus may shift to global developments, including U.S. tensions with Europe.

Other Economic Notes

The OECD highlighted Germany's significant investment backlog, urging comprehensive reforms in municipalities, taxes, and labor, with AI potentially aiding productivity. Eurozone current-account surplus sharply declined in 2025, as per ECB data, signaling shifts in external balances amid trade tensions. House price rises in Ireland are projected to slow to 4% this year, reflecting buyer limits and broader affordability pressures across the region.