Eurozone Macro Daily(Beta Mode)

Oil Surges, Stocks Mixed

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Euro Stoxx 50 | 5,926.11 | +0.51% |

| DAX | 23,803.95 | -0.01% |

| CAC 40 | 8,259.60 | +0.17% |

| EUR/USD | 1.17 | -0.01% |

| EUR/GBP | 0.87 | +0.14% |

| EUR/JPY | 186.66 | +0.36% |

| Gold | 4,739.10 | -0.48% |

| Brent Crude | 102.19 | +7.34% |

| Bitcoin | 70,858.05 | -3.01% |

| German 2Y Bund | - | - |

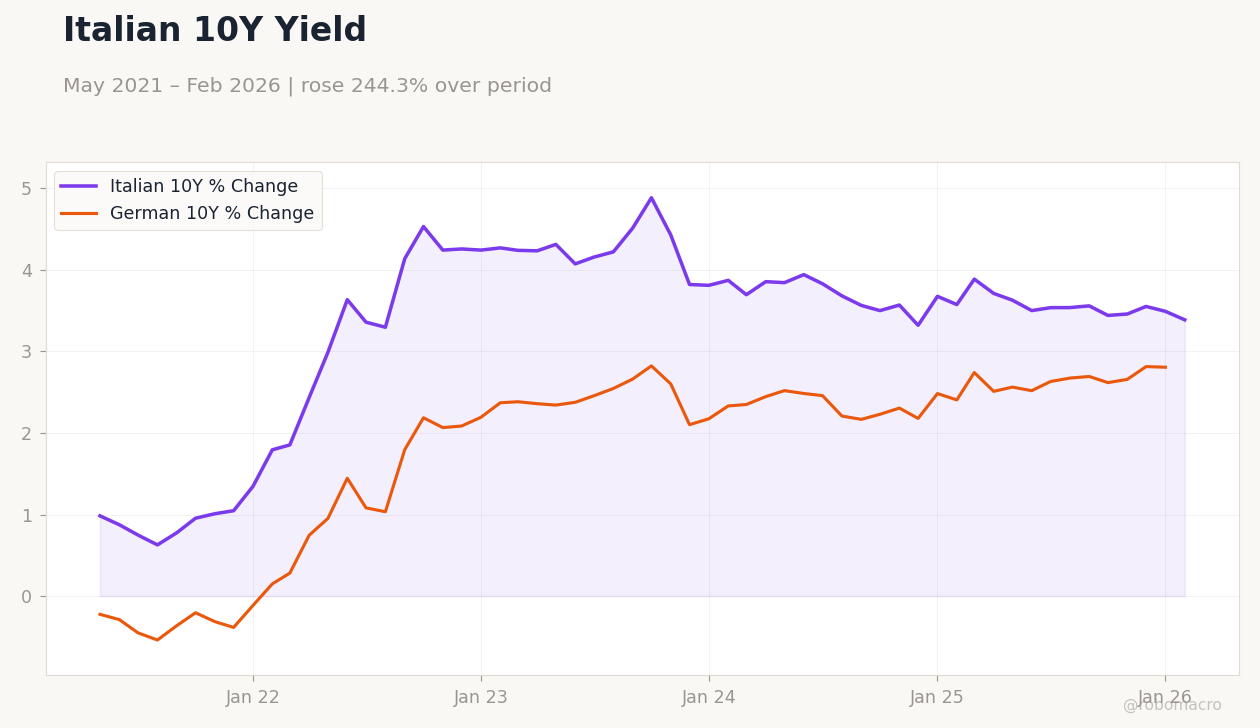

| German 10Y Bund | 2.81% | -0.27% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

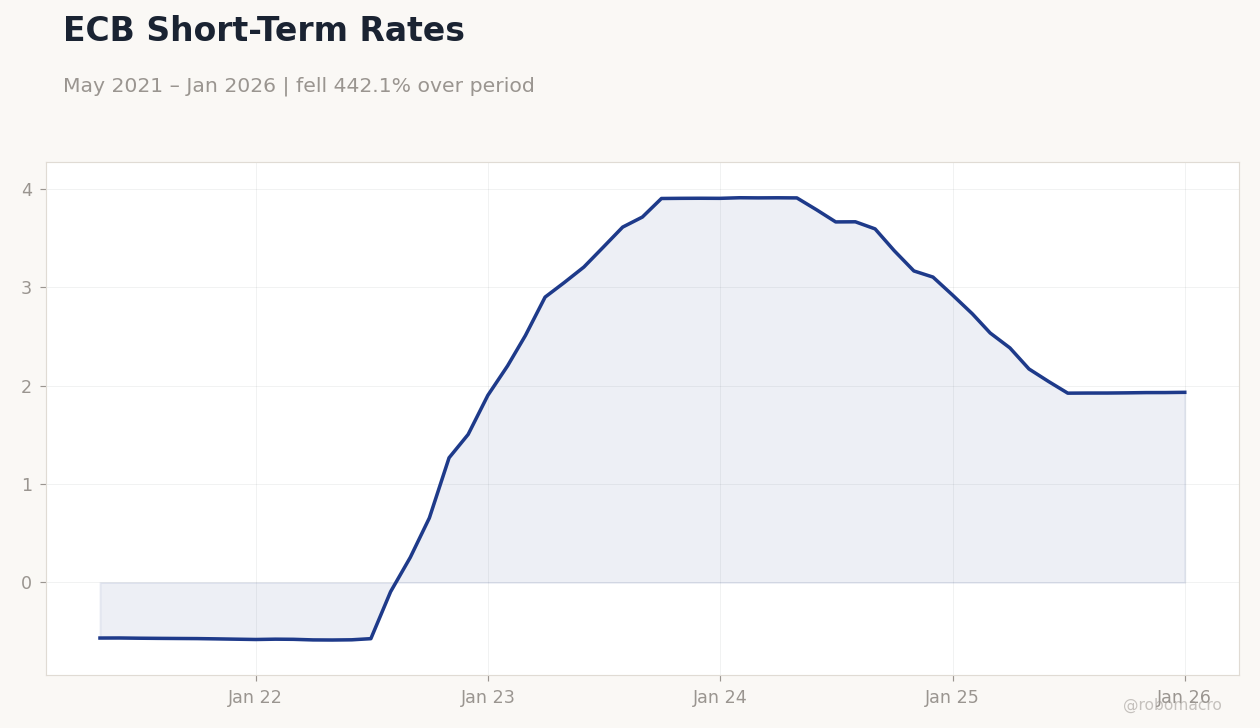

ECB Short-Term Rates | Type: macro_line | Short-Term Rate % Change: 1.932 (2026-01-01) | Range: -0.5847–3.909 | Trend(5pt): -0.5647,-0.5711,3.713,3.165,1.932

ECB Short-Term Rates | Type: macro_line | Short-Term Rate % Change: 1.932 (2026-01-01) | Range: -0.5847–3.909 | Trend(5pt): -0.5647,-0.5711,3.713,3.165,1.932

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Wholesale Prices Month-over-Month | 0.60 | - | 22:00 |

| Wholesale Prices Year-over-Year | 1.20 | - | 22:00 |

| Headline Unemployment Rate | 4.10 | - | 20:30 |

| Trade Balance | 1,089m | - | 00:00 |

- Brent crude jumped 7.34% amid Iran conflict tensions, boosting energy sectors.

- Euro Stoxx 50 rose 0.51%, while DAX dipped slightly on mixed earnings.

- ECB cut expectations firm as global risks mount, with EUR stable.

Yesterday's Recap

European markets showed mixed performance with the Euro Stoxx 50 climbing 0.51% to 5,926.11, driven by gains in French and German industrials amid softer global yields. The German DAX edged down 0.01% to 23,803.95, pressured by automotive weakness despite broader optimism. France's CAC 40 advanced 0.17% to 8,259.60, supported by luxury rebounds.

EUR/USD held steady at 1.17 with a minor 0.01% decline, while EUR/GBP gained 0.14% to 0.87 on sterling softness. EUR/JPY rose 0.36% to 186.66. Brent crude surged 7.34% to 102.19, reflecting Strait of Hormuz threats from ongoing Iran conflicts.

Gold dipped 0.48% to 4,739.10, and Bitcoin fell 3.01% to 70,858.05. No major Eurozone data releases occurred, allowing markets to focus on global geopolitics and commodity flows. German 10Y Bund yields fell 0.27% to 2.81%, signaling safe-haven demand.

The Day Ahead

Attention turns to Germany's wholesale prices data at 22:00 ET on April 13, with month-over-month expected to reflect input cost trends after prior 0.6% rise. Year-over-year German wholesale prices follow at the same time, building on the previous 1.2% increase amid energy volatility. Netherlands headline unemployment rate is slated for release on April 15 at 20:30 ET, anticipated to show labor market resilience from the prior 4.1%.

Italy's trade balance data arrives on April 17 at 00:00 ET, providing insights into export dynamics following the last 1.089 billion euro surplus. Markets will monitor these for inflation and growth signals ahead of broader ECB policy cues. No immediate high-impact events today, but geopolitical headlines could sway sentiment.

Tomorrow, April 14, features no scheduled events based on available data.

Other Economic Notes

Surging fuel prices from the Iran war are driving a spike in European EV demand, potentially establishing higher baseline interest as consumers adapt to energy shocks. Eurozone economies face vulnerability from ageing populations, exacerbating labor shortages and fiscal strains in countries like Germany and Italy. France's push for digital sovereignty, including shifts to Linux and public-private alliances, aims to reduce reliance on non-EU tech amid broader EU capital markets integration efforts.

(cont...)