Eurozone Macro Daily(Beta Mode)

Bundesbank Upbeat on Growth, Prices Surge

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Euro Stoxx 50 | 5,933.28 | -0.12% |

| DAX | 24,066.70 | +0.09% |

| CAC 40 | 8,262.70 | -0.14% |

| EUR/USD | 1.18 | -0.21% |

| EUR/GBP | 0.87 | +0.21% |

| EUR/JPY | 187.88 | +0.20% |

| Gold | 4,819.50 | +0.71% |

| Brent Crude | 98.04 | -1.36% |

| Bitcoin | 74,760.71 | -0.06% |

| German 2Y Bund | - | - |

| German 10Y Bund | 2.91% | +5.84% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Wholesale Prices Month-over-Month | 0.60 | 0.40 | 2.70 |

| Wholesale Prices Year-over-Year | 1.20 | - | 4.10 |

| Headline Unemployment Rate | 4.10 | - | 4 |

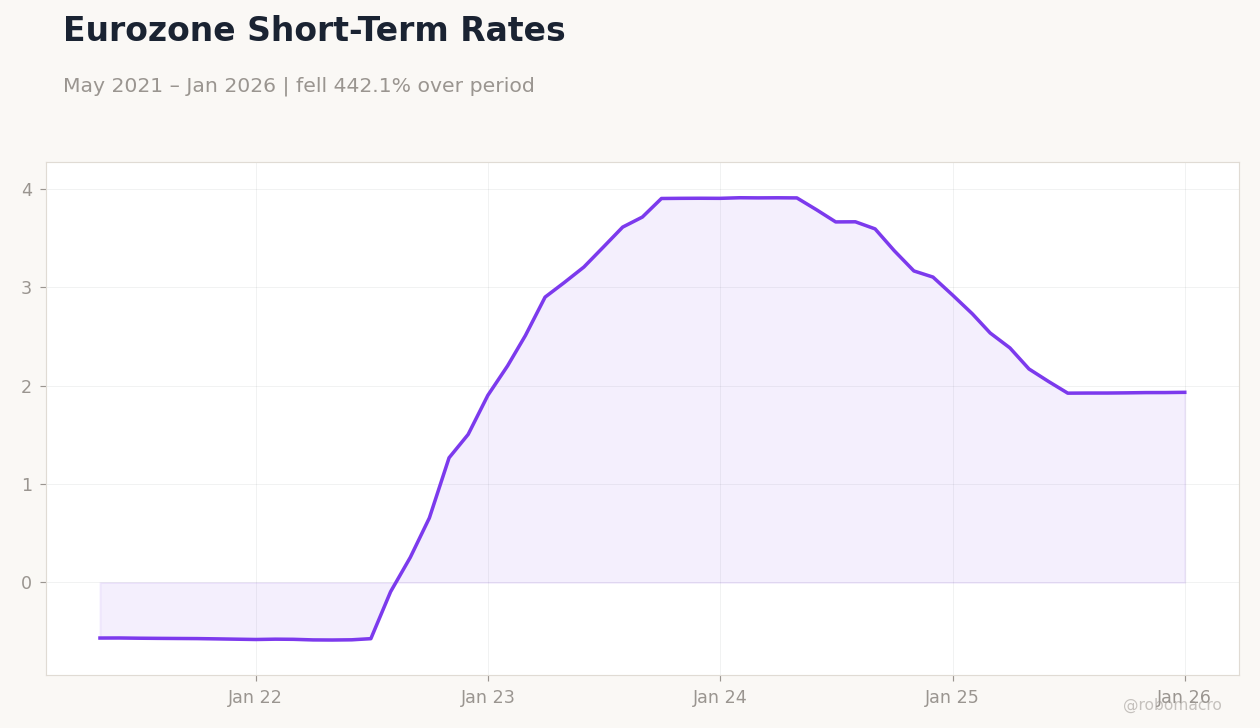

German 10Y Yield | Type: macro_line | German 10Y Yield: 2.905 (2026-03-01) | Range: -0.5386–2.905 | Trend(6pt): -0.2235,1.082,2.661,2.306,2.807,2.905

German 10Y Yield | Type: macro_line | German 10Y Yield: 2.905 (2026-03-01) | Range: -0.5386–2.905 | Trend(6pt): -0.2235,1.082,2.661,2.306,2.807,2.905

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Trade Balance | 1,089m | 3,830m | 00:00 |

- German wholesale prices unexpectedly surged, signaling persistent inflationary pressures amid Bundesbank's recession avoidance outlook.

- Netherlands unemployment dipped slightly, reflecting labor market resilience in the periphery.

- Mixed equity moves with Bund yields rising, as markets digest ECB hike signals and global tensions.

Yesterday's Recap

German wholesale prices rose 2.7% month-over-month, far exceeding the 0.4% consensus and 0.6% prior, while year-over-year figures climbed to 4.1% from 1.2%, highlighting renewed input cost pressures in Europe's largest economy. Netherlands headline unemployment eased to 4% from 4.1%, indicating steady job market conditions despite broader slowdown fears. Euro Stoxx 50 dipped 0.12% to 5,933.28, weighed by tech weakness, while Germany's DAX edged up 0.09% to 24,066.70 on industrial gains.

France's CAC 40 fell 0.14% to 8,262.70 amid energy sector drags. EUR/USD slipped 0.21% to 1.18, pressured by dollar strength, but EUR/GBP rose 0.21% to 0.87 and EUR/JPY gained 0.20% to 187.88. German 10-year Bund yields rose to 2.91%, up 5.84% from prior levels, reflecting hawkish repricing on inflation data.

Brent crude dropped 1.36% to 98.04, easing some energy cost concerns, while gold climbed 0.71% to 4,819.50 as a safe haven. Bitcoin edged down 0.06% to 74,760.71.

The Day Ahead

Italy's trade balance for February is due at 00:00 ET, with consensus expecting a surplus of €3.83 billion versus the prior €1.089 billion, potentially signaling export recovery amid global demand shifts. Markets will watch for implications on Italy's current account and broader Eurozone trade dynamics. No major ECB events are scheduled, leaving focus on data-driven sentiment.

Peripheral bond spreads may tighten if the release beats expectations, supporting EUR crosses. Expect light trading volumes ahead of the weekend, with attention on any geopolitical updates from the Middle East.

Other Economic Notes

Bundesbank President emphasized Germany's likelihood of avoiding recession despite oil shocks, bolstering confidence in core Eurozone growth. Falling fuel prices in Germany, down for the third day, could alleviate consumer pressures and support discretionary spending. EU fiscal debates intensify as Germany pushes for stricter debt rules, pressuring high-deficit nations like Italy.

Germany approved €3.8 billion in power-cost support for industry, aiding energy-intensive sectors. (cont...)