Eurozone Macro Daily(Beta Mode)

ZEW Dives, Stocks Slide

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Euro Stoxx 50 | 5,930.25 | -0.88% |

| DAX | 24,270.87 | -0.60% |

| CAC 40 | 8,235.72 | -1.14% |

| EUR/USD | 1.18 | -0.26% |

| EUR/GBP | 0.87 | -0.20% |

| EUR/JPY | 187.01 | -0.10% |

| Gold | 4,785.50 | +1.85% |

| Brent Crude | 92.50 | -6.07% |

| Bitcoin | 78,020.10 | +2.18% |

| German 2Y Bund | - | - |

| German 10Y Bund | 2.91% | +5.84% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Producer Price Index Year-over-Year | -3.30 | - | -0.20 |

| Trade Balance | -4,000m | - | -3,300m |

| ZEW Economic Sentiment Index | -0.50 | -5 | -17.20 |

| Consumer Confidence Index | -30 | - | -44 |

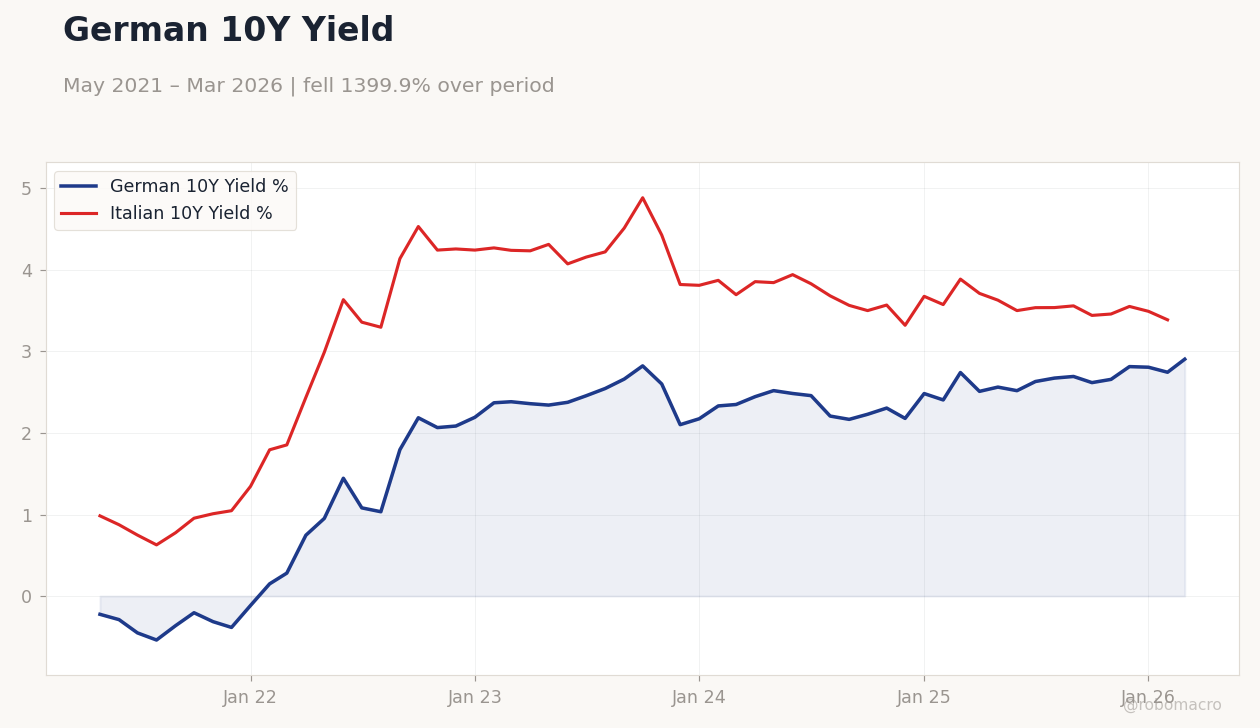

German 10Y Yield | Type: macro_line | German 10Y Yield %: 2.905 (2026-03-01) | Range: -0.5386–2.905 | Trend(6pt): -0.2235,1.082,2.661,2.306,2.807,2.905 | Italian 10Y Yield %: 3.388 (2026-02-01) | Range: 0.628–4.885 | Trend(6pt): 0.984,3.359,4.513,3.569,3.492,3.388

German 10Y Yield | Type: macro_line | German 10Y Yield %: 2.905 (2026-03-01) | Range: -0.5386–2.905 | Trend(6pt): -0.2235,1.082,2.661,2.306,2.807,2.905 | Italian 10Y Yield %: 3.388 (2026-02-01) | Range: 0.628–4.885 | Trend(6pt): 0.984,3.359,4.513,3.569,3.492,3.388

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Business Confidence Index | 99 | 99 | 22:45 |

| S&P Global Composite PMI Flash | 48.80 | 48.60 | 23:15 |

| S&P Global Manufacturing PMI Flash | 50 | 49.50 | 23:15 |

| S&P Global Services PMI Flash | 48.80 | 48.40 | 23:15 |

| S&P Global Manufacturing PMI Flash | 52.20 | 51.30 | 23:30 |

| S&P Global Composite PMI Flash | 51.90 | 51.10 | 23:30 |

| S&P Global Services PMI Flash | 50.90 | 50.30 | 23:30 |

| Consumer Confidence Index | 89 | 88 | 22:45 |

| Ifo Business Climate | 86.40 | 85.50 | 00:00 |

- German ZEW sentiment plunged to -17.2, signaling deepening economic pessimism amid geopolitical tensions.

- Markets declined with Euro Stoxx 50 down 0.88%, reflecting weak data and global angst.

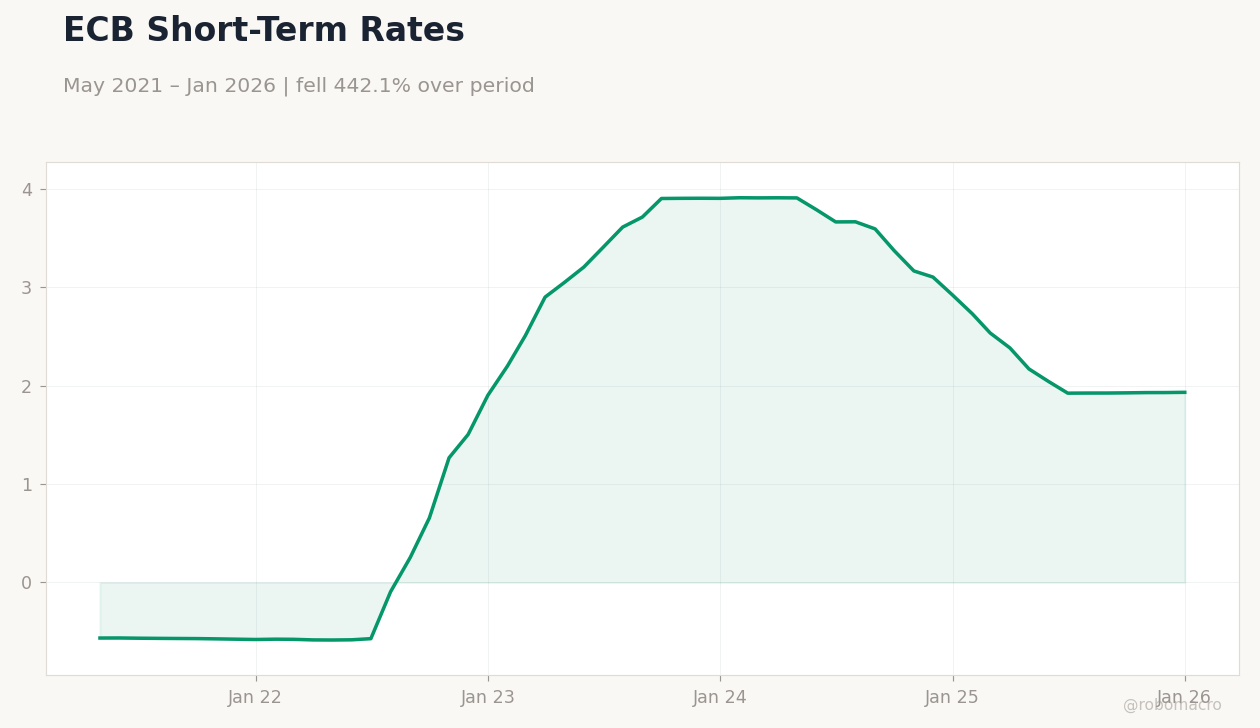

- ECB deposit rate holds at 2.00%, with focus on upcoming PMIs for rate path clues.

Yesterday's Recap

German producer prices improved year-over-year to -0.2% from -3.3%, indicating easing deflationary pressures in manufacturing. Spain's trade balance narrowed to -3.3 billion euros from -4 billion, boosted by stronger exports despite weak global demand. Germany's ZEW Economic Sentiment Index fell sharply to -17.2 from -0.5, missing consensus of -5 and highlighting concerns over energy disruptions and fiscal strains.

Netherlands consumer confidence dropped to -44 from -30, underscoring household worries about inflation and job security. Eurozone equities weakened, with Euro Stoxx 50 closing at 5,930.25 down 0.88%, DAX at 24,270.87 down 0.60%, and CAC 40 at 8,235.72 down 1.14%. EUR/USD slipped to 1.18 down 0.26%, while German 10-year Bund yields rose to 2.91% up 5.84%, driven by risk-off sentiment from Middle East developments.

Brent crude tumbled to 92.50 down 6.07%, pressuring energy-linked sectors in France and Italy.

The Day Ahead

French business confidence index is due at 22:45 ET, with consensus at 99 unchanged from previous, potentially signaling stable manufacturing sentiment. France's flash S&P Global PMIs follow at 23:15 ET, including composite at 48.6 consensus from 48.8, manufacturing at 49.5 from 50.0, and services at 48.4 from 48.8, which could highlight ongoing contraction risks. Germany's flash S&P Global PMIs are set for 23:30 ET, with manufacturing consensus at 51.3 from 52.2, composite at 51.1 from 51.9, and services at 50.3 from 50.9, key for gauging core Eurozone growth momentum.

French consumer confidence arrives at 22:45 ET on April 23, consensus 88 from 89, amid household spending concerns. Germany's Ifo Business Climate is slated for 00:00 ET on April 24, consensus 85.5 from 86.4, offering insights into business outlook.

Other Economic Notes

Broader Eurozone themes include persistent fiscal challenges, with France facing criticism for unsustainable deficits as highlighted by Dutch Finance Minister's remarks on borrowing. Geopolitical risks from the Middle East are exacerbating energy supply concerns, potentially delaying recovery in Germany and Italy. (cont...)