Eurozone Macro Daily(Beta Mode)

Eurozone PMIs Slump on War Fears

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Euro Stoxx 50 | 5,894.73 | -0.19% |

| DAX | 24,194.90 | -0.31% |

| CAC 40 | 8,227.32 | +0.87% |

| EUR/USD | 1.17 | -0.19% |

| EUR/GBP | 0.87 | +0.05% |

| EUR/JPY | 186.61 | -0.04% |

| Gold | 4,688.20 | -0.36% |

| Brent Crude | 105.60 | +0.50% |

| Bitcoin | 77,707.52 | -0.63% |

| German 2Y Bund | - | - |

| German 10Y Bund | 2.91% | +5.84% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Producer Price Index Year-over-Year | -3.30 | - | -0.20 |

| Trade Balance | -4,000m | - | -3,300m |

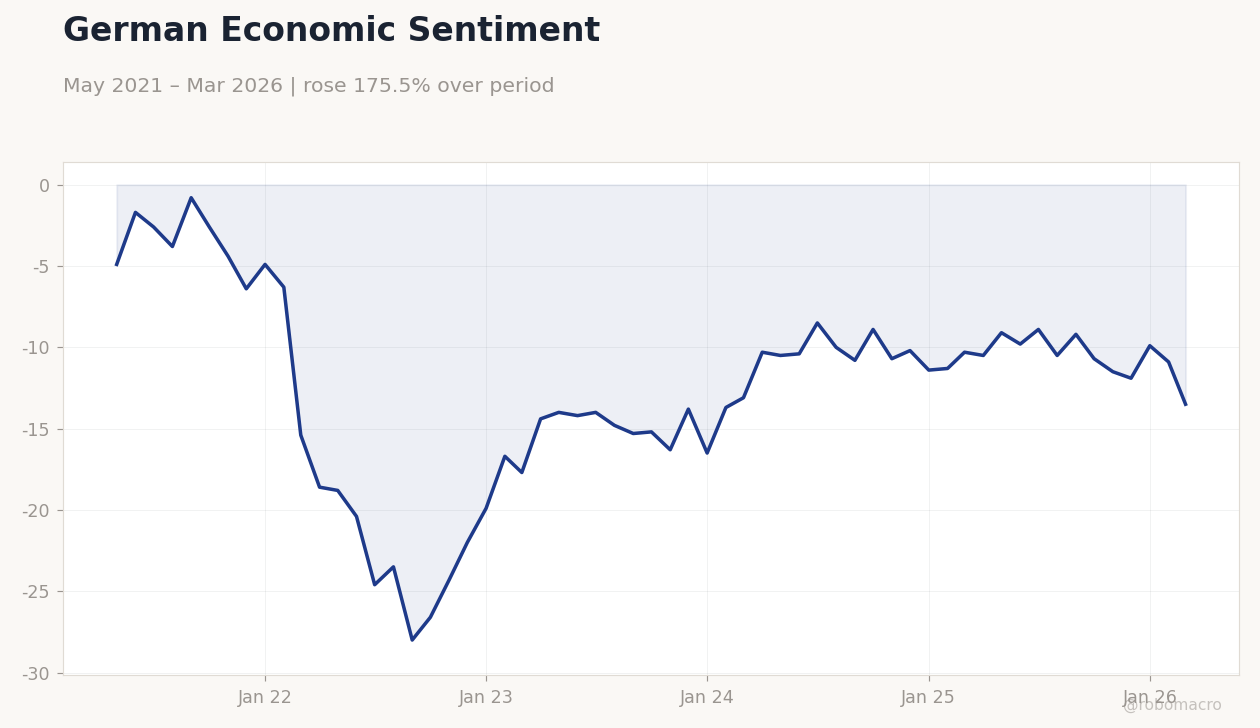

| ZEW Economic Sentiment Index | -0.50 | -5 | -17.20 |

| Consumer Confidence Index | -30 | - | -44 |

| Business Confidence Index | 99 | 99 | 100 |

| S&P Global Composite PMI Flash | 48.80 | 48.60 | 47.60 |

| S&P Global Manufacturing PMI Flash | 50 | 49.50 | 52.80 |

| S&P Global Services PMI Flash | 48.80 | 48.40 | 46.50 |

| S&P Global Manufacturing PMI Flash | 52.20 | 51.30 | 51.20 |

| S&P Global Composite PMI Flash | 51.90 | 51.10 | 48.30 |

German Economic Sentiment | Type: macro_line | Consumer Confidence: -13.5 (2026-03-01) | Range: -28–-0.8 | Trend(6pt): -4.9,-24.6,-15.3,-10.7,-9.9,-13.5

German Economic Sentiment | Type: macro_line | Consumer Confidence: -13.5 (2026-03-01) | Range: -28–-0.8 | Trend(6pt): -4.9,-24.6,-15.3,-10.7,-9.9,-13.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Consumer Confidence Index | 89 | 88 | 22:45 |

| Ifo Business Climate | 86.40 | 85.50 | 00:00 |

- Flash PMIs in France and Germany showed sharp contractions, signaling broader Eurozone slowdown amid Mideast tensions.

- German ZEW sentiment plunged to -17.2, far below expectations, while French business confidence edged up slightly.

- Markets mixed: CAC 40 rose 0.87%, but Euro Stoxx 50 and DAX dipped; Bund yields climbed 5.84%.

Yesterday's Recap

Eurozone markets ended mixed as weak economic data weighed on sentiment, with the Euro Stoxx 50 declining 0.19% to 5,894.73 and Germany's DAX falling 0.31% to 24,194.90, while France's CAC 40 bucked the trend with a 0.87% gain to 8,227.32. Germany's ZEW Economic Sentiment Index tumbled to -17.2, missing the consensus of -5 and prior -0.5, reflecting heightened pessimism amid geopolitical risks. French flash PMIs disappointed, with the composite at 47.6 versus 48.6 expected, manufacturing at 52.8 beating 49.5 but services at 46.5 below 48.4, pointing to service-sector weakness.

German flash PMIs also underperformed, showing composite at 48.3 against 51.1 consensus, manufacturing at 51.2 near 51.3, and services at 46.9 versus 50.3, underscoring a broader slowdown. Spain's trade balance improved to -€3.3 billion from -€4.0 billion prior, while the Netherlands' consumer confidence sank to -44.0 from -30.0. Germany's producer price index rose to -0.2% year-over-year from -3.3%, indicating easing deflationary pressures.

French business confidence ticked up to 100 from 99, slightly above expectations, providing a minor positive note amid the broader data gloom.

The Day Ahead

Attention turns to France's consumer confidence index at 22:45 ET, expected at 88 versus prior 89, which could signal ongoing household caution amid inflation and geopolitical strains. Germany's Ifo Business Climate index follows at 00:00 ET, forecasted at 85.5 from 86.4 prior, a key gauge of business sentiment that often influences ECB policy expectations. No major Eurozone-wide releases are scheduled, leaving markets to digest yesterday's PMI weakness and global developments.

Traders will monitor any ECB speaker comments, though none are officially slated, potentially amplifying focus on Bund yields and EUR crosses. Upcoming data could reinforce stagflation concerns if they miss estimates, pressuring equities lower.

Other Economic Notes

Broader Eurozone themes highlight rising stagflation risks, as Nomura warns of surging prices amid contracting activity, exacerbated by Mideast war effects on supply chains. (cont...)