Eurozone Macro Daily(Beta Mode)

German Data Disappoints, Stocks Dip

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Euro Stoxx 50 | 5,901.49 | -1.19% |

| DAX | 24,663.61 | -1.02% |

| CAC 40 | 8,097.69 | -1.27% |

| EUR/USD | 1.18 | +0.23% |

| EUR/GBP | 0.86 | -0.03% |

| EUR/JPY | 183.85 | -0.48% |

| Gold | 4,716.00 | +0.34% |

| Brent Crude | 101.85 | +1.79% |

| Bitcoin | 79,775.23 | -0.29% |

| German 2Y Bund | - | - |

| German 10Y Bund | 2.91% | +5.84% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| S&P Global Manufacturing PMI Index | 48.70 | 49.50 | 51.70 |

| S&P Global Manufacturing PMI Index | 51.30 | 51.90 | 52.10 |

| Unemployment Level Change | -22,900 | -18,600 | -62,700 |

| Industrial Production Month-over-Month | -0.90 | 0.50 | 1 |

| S&P Global Services PMI | 53.30 | 52 | 47.90 |

| S&P Global Services PMI | 48.80 | - | 49.80 |

| Retail Sales Month-over-Month | -0.10 | -0.40 | 0.80 |

| Factory Orders Month-over-Month | 1.40 | 1 | 5 |

| Trade Balance | -5,500m | -5,600m | -6,900m |

| Trade Balance | 19,800m | 18,900m | 14,300m |

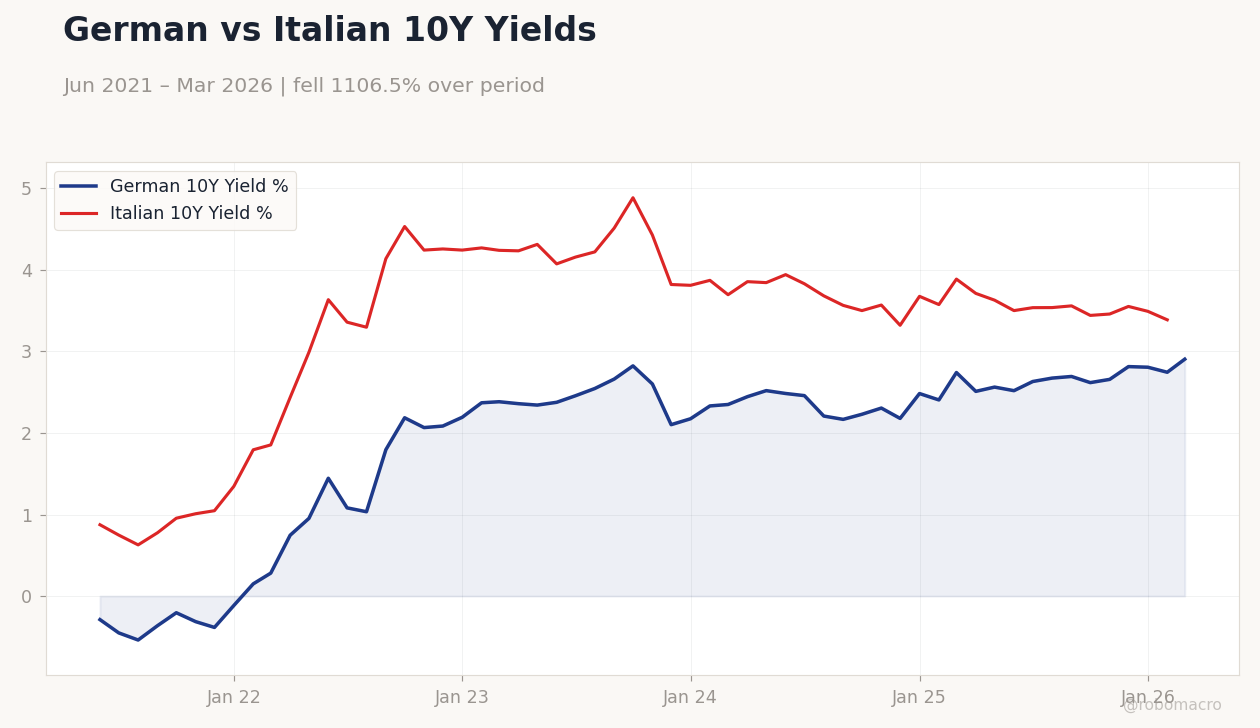

German vs Italian 10Y Yields | Type: macro_line | German 10Y Yield %: 2.905 (2026-03-01) | Range: -0.5386–2.905 | Trend(6pt): -0.2886,1.034,2.823,2.179,2.745,2.905 | Italian 10Y Yield %: 3.388 (2026-02-01) | Range: 0.628–4.885 | Trend(5pt): 0.875,3.297,4.885,3.321,3.388

German vs Italian 10Y Yields | Type: macro_line | German 10Y Yield %: 2.905 (2026-03-01) | Range: -0.5386–2.905 | Trend(6pt): -0.2886,1.034,2.823,2.179,2.745,2.905 | Italian 10Y Yield %: 3.388 (2026-02-01) | Range: 0.628–4.885 | Trend(5pt): 0.875,3.297,4.885,3.321,3.388

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- German trade and production missed forecasts, dragging equities lower.

- Spanish services PMI contracted sharply; Italian retail sales surprised positively.

- Mixed data underscores uneven Eurozone recovery amid global pressures.

Yesterday's Recap

Eurozone markets ended lower amid underwhelming German data. Germany's trade balance shrank to €14.3 billion in March, missing the €18.9 billion consensus, with exports up just 0.5% month-over-month and industrial production down 0.7% versus a 0.5% expected rise. French industrial production climbed 1% month-over-month, beating the 0.5% forecast, but the trade balance worsened to -€6.9 billion from -€5.5 billion.

Spanish unemployment dropped by 62,700, far exceeding the 18,600 decline consensus, yet the S&P Global Services PMI fell to 47.9, below the 52 estimate and indicating contraction. Italian retail sales grew 0.8% month-over-month, topping the -0.4% consensus, with the S&P Global Services PMI at 49.8. Earlier, Spanish and Italian manufacturing PMIs beat expectations at 51.7 and 52.1, respectively.

Equities slid: Euro Stoxx 50 down 1.19% to 5,901.49, DAX off 1.02% to 24,663.61, and CAC 40 lower 1.27% to 8,097.69. EUR/USD rose 0.23% to 1.18, EUR/GBP dipped 0.03% to 0.86, and EUR/JPY fell 0.48% to 183.85. German 10-year Bund yields increased to 2.91%, up 5.84 basis points.

Gold gained 0.34% to 4,716.00, Brent crude rose 1.79% to 101.85, and Bitcoin eased 0.29% to 79,775.23.

The Day Ahead

No significant Eurozone economic releases are scheduled for today or tomorrow, likely resulting in quieter trading. Markets may digest yesterday's mixed data and watch for external influences, such as U.S. market moves or commodity shifts.

EU finance ministers' ongoing fiscal discussions could yield updates, potentially affecting sentiment. Broader focus may turn to global news, including geopolitical developments, with limited ECB activity expected.

Other Economic Notes

Germany's projected €52 billion tax shortfall through 2030, tied to economic fallout from the Iran war, highlights manufacturing vulnerabilities amid trade tensions. French exports rose slightly to €52.5 billion in March, bolstering modest recovery signals and curbing ECB rate-cut speculation. Italy's retail sales resilience contrasts with Spain's services sector weakness, illustrating patchy growth across the bloc.

The ECB deposit rate stands at 2.00% as of May 8, 2026. <i>↓ p.2</i>