Eurozone Macro Daily(Beta Mode)

Eurozone Trade Misses Cloud PMI Outlook

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Euro Stoxx 50 | 5,846.95 | -0.07% |

| DAX | 24,307.92 | +1.49% |

| CAC 40 | 7,966.70 | -0.19% |

| EUR/USD | 1.16 | -0.55% |

| EUR/GBP | 0.87 | -0.20% |

| EUR/JPY | 184.34 | -0.44% |

| Gold | 4,484.20 | -0.49% |

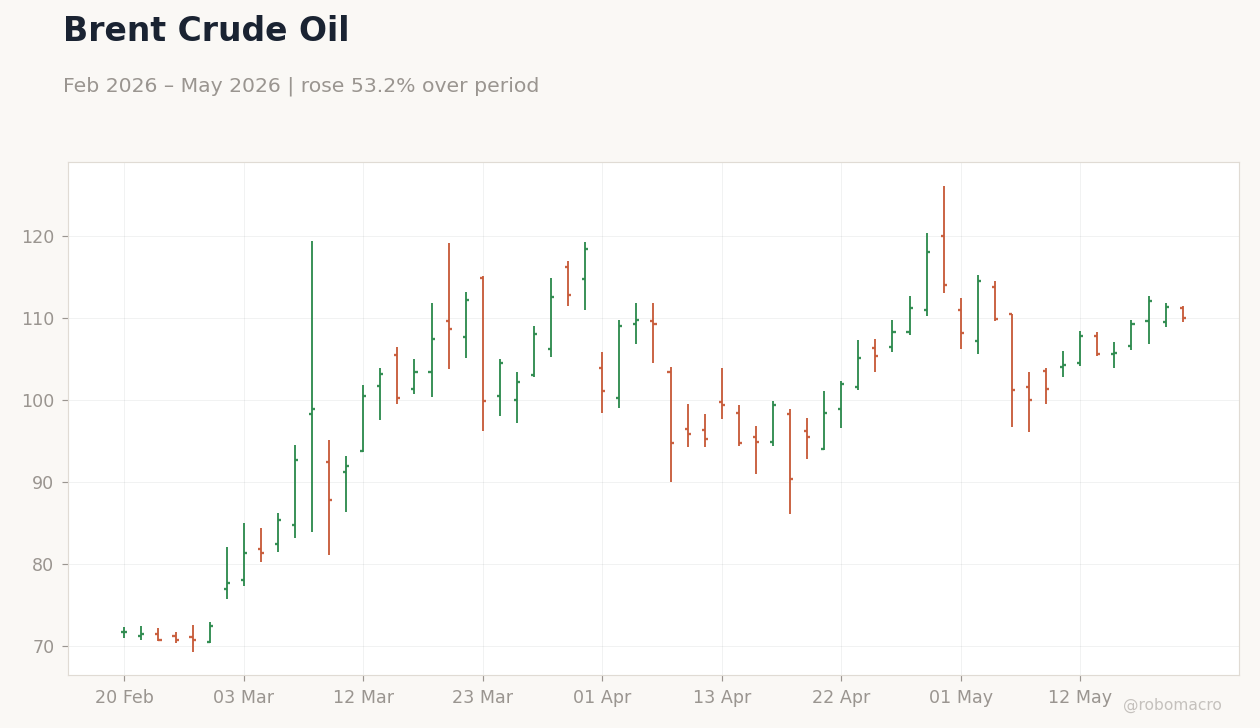

| Brent Crude | 109.99 | -1.16% |

| Bitcoin | 77,169.37 | +0.55% |

| German 2Y Bund | - | - |

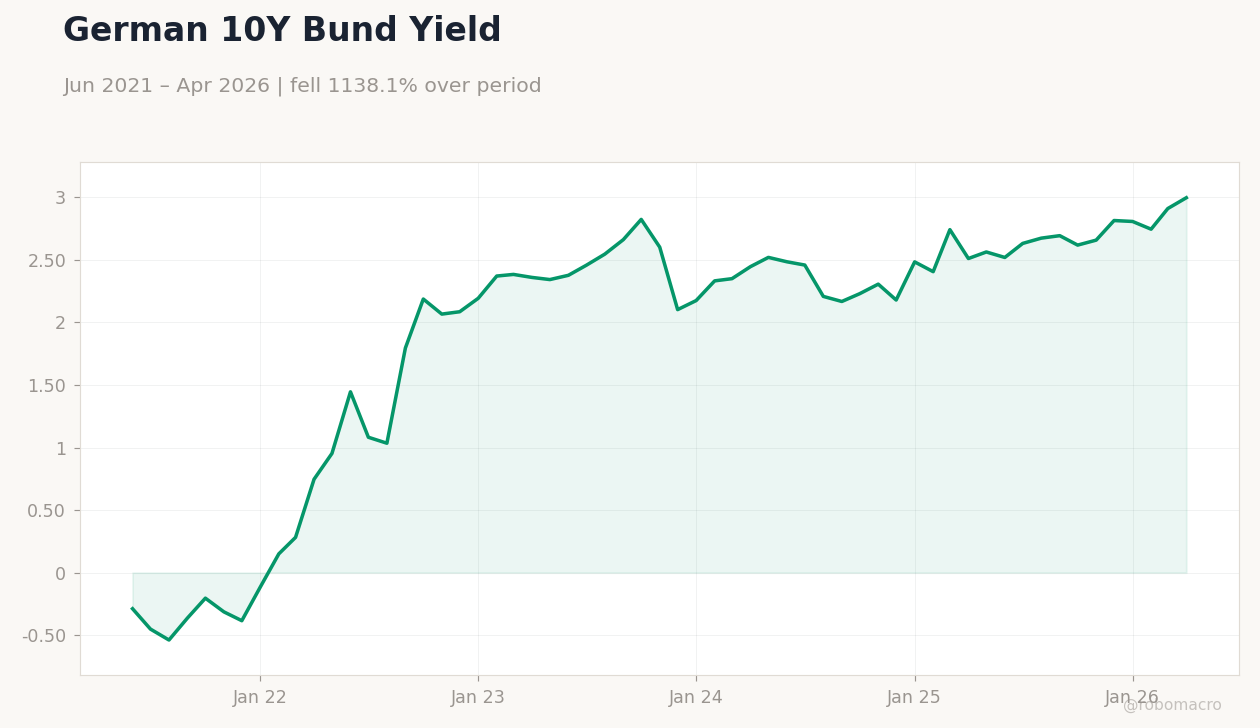

| German 10Y Bund | 3.00% | +2.97% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Trade Balance | 4,944m | 5,200m | 4,709m |

| Trade Balance | -3,300m | - | -4,400m |

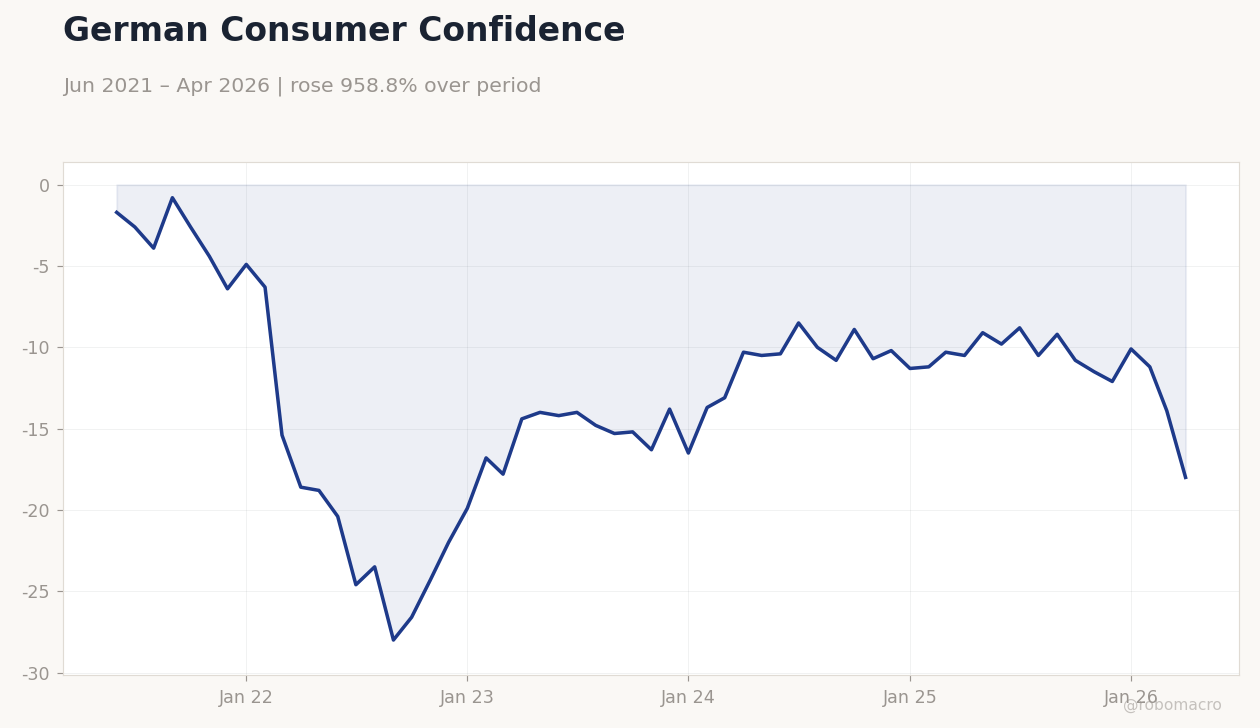

German Consumer Confidence | Type: macro_line | Index: -18 (2026-04-01) | Range: -28–-0.8 | Trend(6pt): -1.7,-23.5,-15.2,-10.2,-11.2,-18

German Consumer Confidence | Type: macro_line | Index: -18 (2026-04-01) | Range: -28–-0.8 | Trend(6pt): -1.7,-23.5,-15.2,-10.2,-11.2,-18

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Producer Price Index Year-over-Year | -0.20 | - | 22:00 |

| S&P Global Composite PMI Flash | 47.60 | 47.70 | 23:15 |

| S&P Global Manufacturing PMI Flash | 52.80 | 52.50 | 23:15 |

| S&P Global Services PMI Flash | 46.50 | 46.50 | 23:15 |

| S&P Global Manufacturing PMI Flash | 51.40 | 51 | 23:30 |

| S&P Global Composite PMI Flash | 48.40 | 48.40 | 23:30 |

| S&P Global Services PMI Flash | 46.90 | 47 | 23:30 |

| GFK Consumer Confidence Index | -33.30 | -34 | 22:00 |

| Business Confidence Index | 100 | 100 | 22:45 |

| Ifo Business Climate | 84.40 | 84.20 | 00:00 |

- Italian and Spanish trade balances missed expectations, signaling softer external demand.

- DAX rose 1.49% while Euro Stoxx 50 edged down 0.07% amid mixed equity flows.

- German 10-year Bund yield climbed to 3.00% as markets priced limited near-term ECB easing.

Yesterday's Recap

Italy posted a trade surplus of 4.709 billion euros, below the 5.2 billion consensus and prior 4.944 billion. Spain’s trade deficit widened to 4.4 billion euros from 3.3 billion previously. Euro Stoxx 50 closed at 5,846.95, down 0.07%, while the DAX advanced 1.49% to 24,307.92 and the CAC 40 slipped 0.19%.

EUR/USD fell 0.55% to 1.16 and EUR/JPY declined 0.44% to 184.34. German 10-year Bund yields rose 2.97% to 3.00%. Brent crude dropped 1.16% to 109.99 and gold eased 0.49%.

No major ECB speeches occurred.

The Day Ahead

Germany releases producer prices and flash PMIs at 23:30 ET, with manufacturing expected at 51.0. France follows with composite, manufacturing and services PMI flashes at 23:15 ET. GfK consumer confidence and Ifo business climate for Germany are due tomorrow, both carrying high market impact.

French business confidence is also scheduled. Markets will focus on any downside surprises that could lift June ECB cut odds. No Governing Council members are speaking.

Other Economic Notes

Eurozone unemployment stands at 6.70%. Softer external demand from Italy and Spain adds to evidence of cooling momentum in core economies. German PPI and Ifo prints will test whether domestic price pressures remain contained at the current 2.00% ECB deposit rate.

Equity outperformance in the DAX suggests selective buying in export names despite broader regional caution. Trade shortfalls may reinforce expectations that growth remains subdued through the summer. Analysts will watch whether services PMIs hold steady or join manufacturing in showing renewed weakness.

Any further softening could prompt renewed discussion of additional stimulus measures later in the year. Regional divergence remains visible, with Germany showing relative resilience while peripheral data disappoint.