Eurozone Macro Daily(Beta Mode)

German PPI Beats as Trade Balances Slip

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Euro Stoxx 50 | 5,976.07 | +2.13% |

| DAX | 24,737.24 | +1.38% |

| CAC 40 | 8,117.42 | +1.70% |

| EUR/USD | 1.16 | +0.17% |

| EUR/GBP | 0.87 | -0.13% |

| EUR/JPY | 184.78 | +0.10% |

| Gold | 4,538.40 | +0.16% |

| Brent Crude | 105.74 | +0.69% |

| Bitcoin | 77,985.56 | +1.61% |

| German 2Y Bund | - | - |

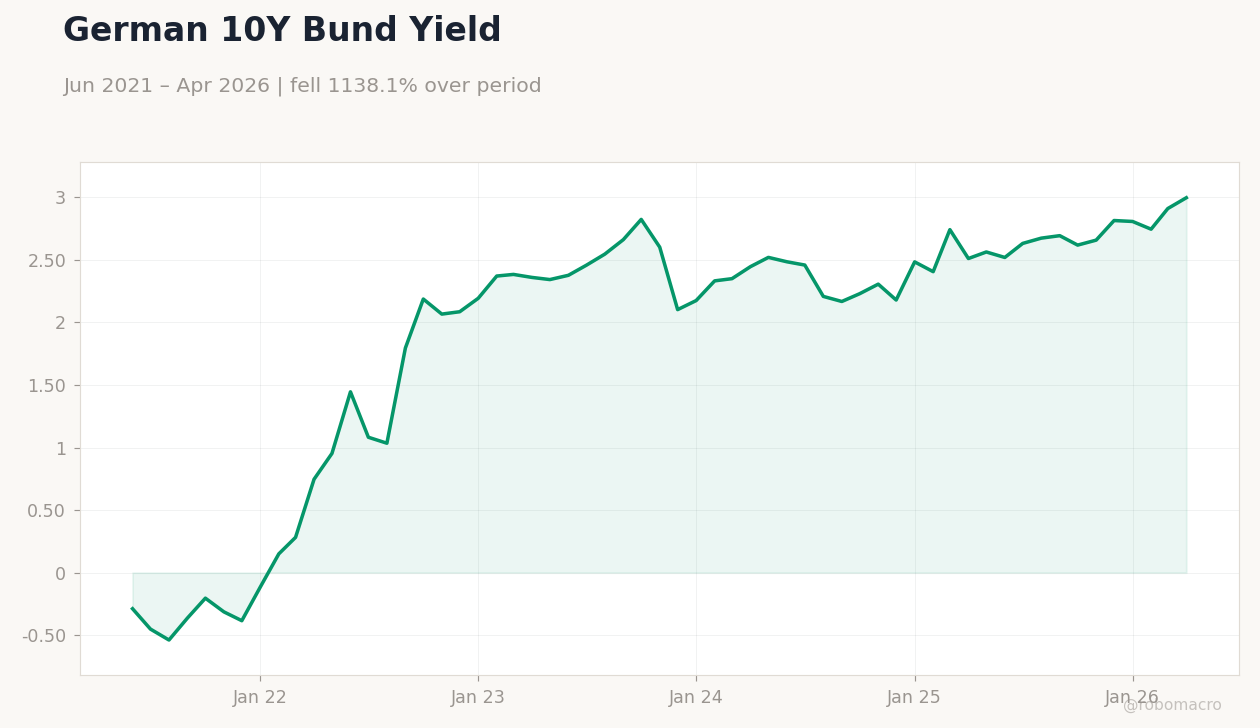

| German 10Y Bund | 3.00% | +2.97% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Trade Balance | 4,944m | 5,200m | 4,709m |

| Trade Balance | -3,300m | - | -4,400m |

| Producer Price Index Year-over-Year | -0.20 | 1.50 | 1.70 |

| Consumer Confidence Index | -44 | - | -46 |

| Headline Unemployment Rate | 4 | - | 3.90 |

German Business Confidence | Type: macro_line | Confidence Index: -18 (2026-04-01) | Range: -28–-0.8 | Trend(6pt): -1.7,-23.5,-15.2,-10.2,-11.2,-18

German Business Confidence | Type: macro_line | Confidence Index: -18 (2026-04-01) | Range: -28–-0.8 | Trend(6pt): -1.7,-23.5,-15.2,-10.2,-11.2,-18

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| S&P Global Composite PMI Flash | 47.60 | 47.70 | 23:15 |

| S&P Global Manufacturing PMI Flash | 52.80 | 52.20 | 23:15 |

| S&P Global Services PMI Flash | 46.50 | 46.60 | 23:15 |

| S&P Global Manufacturing PMI Flash | 51.40 | 51 | 23:30 |

| S&P Global Composite PMI Flash | 48.40 | 48.40 | 23:30 |

| S&P Global Services PMI Flash | 46.90 | 47 | 23:30 |

| GFK Consumer Confidence Index | -33.30 | -34 | 22:00 |

| Business Confidence Index | 100 | 100 | 22:45 |

| Ifo Business Climate | 84.40 | 84.20 | 00:00 |

- German producer prices rose 1.7% y/y, beating consensus, while Italian and Spanish trade balances deteriorated sharply.

- Euro Stoxx 50 gained 2.13% and DAX rose 1.38% as Bund yields climbed to 3.00%.

- ECB deposit rate holds at 2.00% with markets pricing limited near-term easing despite 6.70% eurozone unemployment.

Yesterday's Recap

Italian trade balance narrowed to €4.709 billion, missing consensus and highlighting softer external demand. Spanish trade deficit widened to €4.4 billion, underscoring persistent import pressures. German producer prices climbed 1.7% y/y versus 1.5% expected, signaling firmer pipeline costs.

Dutch consumer confidence fell to -46 while unemployment edged down to 3.9%, reflecting mixed labor-market signals. Euro Stoxx 50 advanced 2.13% to 5,976.07 and DAX gained 1.38% to 24,737.24. EUR/USD edged up 0.17% to 1.16 while the 10-year Bund yield rose to 3.00%.

Brent crude added 0.69% to $105.74 amid geopolitical supply concerns.

The Day Ahead

French S&P Global composite, manufacturing and services PMI flashes are due at 23:15 ET, with markets focused on any services softening. German manufacturing and composite PMI prints follow at 23:30 ET and will set the tone for industrial momentum. GfK consumer confidence and French business confidence indices release tomorrow evening, offering fresh reads on household and corporate sentiment.

The German Ifo business climate index at midnight will be the highest-impact release and is expected to edge lower to 84.2. No ECB speakers are scheduled, leaving data to drive positioning ahead of next week’s policy meeting.

Other Economic Notes

German industry posted record unfilled orders, the highest level since records began in 2015, concentrated in electrical equipment. A new study estimates 400,000 jobs have already disappeared due to China’s export surge, pressuring manufacturing regions. EU approval of nearly €300 million in German semiconductor support aims to bolster chip production capacity.

Banks are committing €750 million to scale the Wero digital payments platform as a European alternative to PayPal. Defence procurement reforms in Germany seek to accelerate spending from the expanded budget.