Eurozone Macro Daily(Beta Mode)

Equities Rally as Bund Yields Climb

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Euro Stoxx 50 | 6,136.66 | +1.95% |

| DAX | 24,888.56 | +1.15% |

| CAC 40 | 8,258.26 | +1.76% |

| EUR/USD | 1.16 | -0.09% |

| EUR/GBP | 0.86 | -0.07% |

| EUR/JPY | 184.90 | -0.08% |

| Gold | 4,527.60 | +0.15% |

| Brent Crude | 95.54 | -7.73% |

| Bitcoin | 76,825.08 | -0.20% |

| German 2Y Bund | - | - |

| German 10Y Bund | 3.00% | +2.97% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

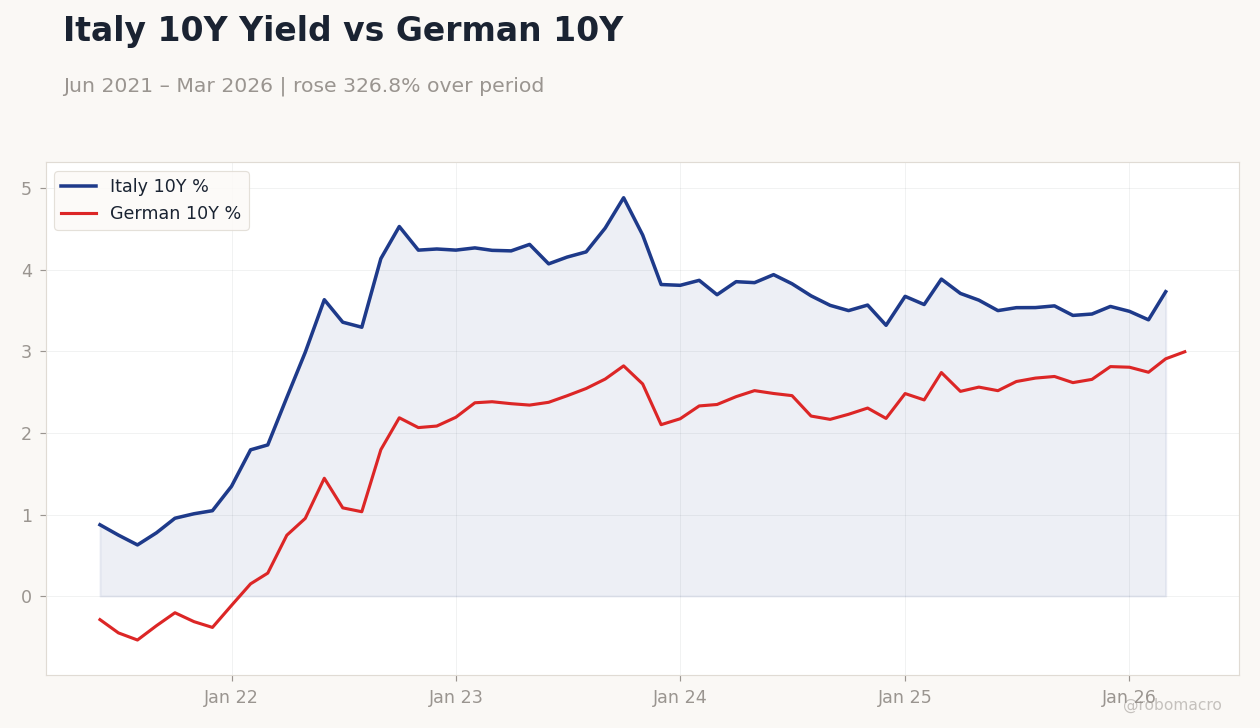

Italy 10Y Yield vs German 10Y | Type: macro_line | Italy 10Y %: 3.733 (2026-03-01) | Range: 0.6276–4.885 | Trend(6pt): 0.8746,3.297,4.885,3.321,3.388,3.733 | German 10Y %: 2.996 (2026-04-01) | Range: -0.5386–2.996 | Trend(6pt): -0.2886,1.034,2.823,2.179,2.745,2.996

Italy 10Y Yield vs German 10Y | Type: macro_line | Italy 10Y %: 3.733 (2026-03-01) | Range: 0.6276–4.885 | Trend(6pt): 0.8746,3.297,4.885,3.321,3.388,3.733 | German 10Y %: 2.996 (2026-04-01) | Range: -0.5386–2.996 | Trend(6pt): -0.2886,1.034,2.823,2.179,2.745,2.996

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Consumer Confidence Index | 84 | 85 | 22:45 |

| Unemployment Benefit Claims | 35,600 | - | 02:00 |

| Business Confidence Index | 87.90 | - | 00:00 |

| Consumer Confidence Index | 90.80 | - | 00:00 |

| Business Confidence Index | -5 | - | 02:00 |

| Inflation Rate Year-over-Year Preliminary | 2.20 | - | 22:45 |

| Inflation Rate Month-over-Month Preliminary | 1 | 0.20 | 22:45 |

| Inflation Rate Month-over-Month Preliminary | 0.40 | - | 23:00 |

| Inflation Rate Year-over-Year Preliminary | 3.20 | 3.40 | 23:00 |

| Headline Unemployment Rate | 6.40 | 6.40 | 23:55 |

- Euro Stoxx 50 rose 1.95% while German 10-year Bund yields jumped 2.97% to 3.00%.

- Bundesbank flagged German Q2 stagnation and price pressures linked to Iran conflict.

- ECB deposit rate holds at 2.00% with focus on inflation persistence.

Yesterday's Recap

European equities posted strong gains with the Euro Stoxx 50 closing at 6,136.66 after a 1.95% advance, the DAX rising 1.15% to 24,888.56 and the CAC 40 adding 1.76% to 8,258.26. German 10-year Bund yields surged to 3.00%, up nearly 3% on the day, while EUR/USD eased 0.09% to 1.16. Brent crude fell sharply by 7.73% to 95.54 amid shifting supply signals.

The Bundesbank warned that Germany faces Q2 stagnation and rising prices because of the Iran war, highlighting downside risks to growth. No major Eurozone data releases occurred on 25 May, leaving markets to digest the Bundesbank assessment and global commodity moves. French and Italian equities followed the regional uptrend while cross rates such as EUR/GBP and EUR/JPY posted modest declines.

Gold edged higher to 4,527.60 and Bitcoin eased to 76,825.08.

The Day Ahead

French consumer confidence is due at 22:45 ET today with consensus at 85. German headline unemployment rate and unemployed persons level are scheduled for 23:55 ET on 28 May, with the jobless rate expected to stay at 6.4%. French preliminary inflation prints follow at 22:45 ET on the same day, covering both year-over-year and month-over-month readings.

Italian business and consumer confidence indices release at midnight ET on 28 May, while Spanish business confidence and inflation data appear shortly after. Italian unemployment and inflation figures close the week on 29 May. Markets will watch the German labor print and French inflation closely for any shift in ECB rate expectations.

Other Economic Notes

France-led EU members are pressing for stricter controls on Chinese imports to protect domestic industry. EU plans for a strategic stockpile of critical minerals aim to reduce reliance on China for rare earths and related inputs. Broader fiscal discussions among EU finance ministers signal tighter conditionality on green spending under the next MFF framework.

These measures reflect ongoing efforts to balance competitiveness with supply-chain security across member states. The Bundesbank’s warning of stagnation and higher prices adds to the complex backdrop facing policymakers.