Eurozone Macro Daily(Beta Mode)

German Retail Sales in Focus as PMIs Rise

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Euro Stoxx 50 | 6,050.54 | -0.08% |

| DAX | 25,104.70 | +0.05% |

| CAC 40 | 8,183.34 | -0.07% |

| EUR/USD | 1.17 | +0.01% |

| EUR/GBP | 0.87 | -0.11% |

| EUR/JPY | 185.79 | +0.11% |

| Gold | 4,553.50 | -0.15% |

| Brent Crude | 93.35 | +1.41% |

| Bitcoin | 73,254.64 | -0.68% |

| German 2Y Bund | - | - |

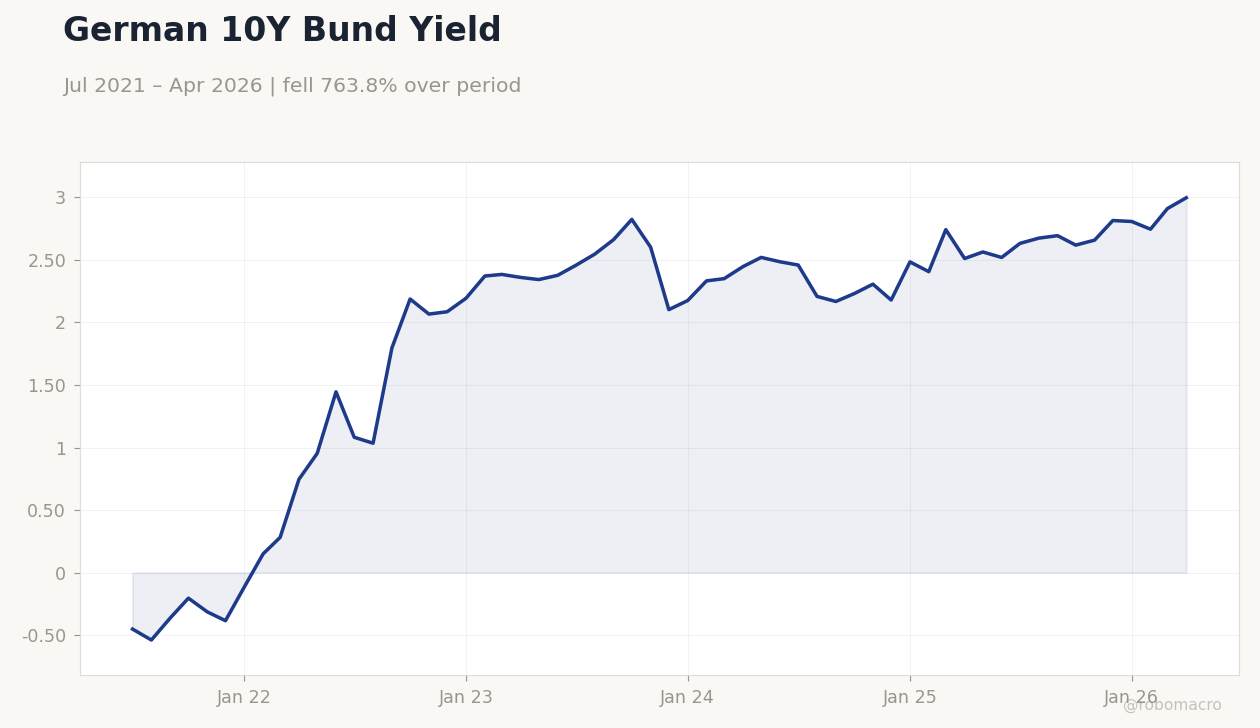

| German 10Y Bund | 3.00% | +2.97% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

German 10Y Bund Yield | Type: macro_line | Yield %: 2.996 (2026-04-01) | Range: -0.5386–2.996 | Trend(6pt): -0.4514,1.795,2.601,2.484,2.91,2.996

German 10Y Bund Yield | Type: macro_line | Yield %: 2.996 (2026-04-01) | Range: -0.5386–2.996 | Trend(6pt): -0.4514,1.795,2.601,2.484,2.91,2.996

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

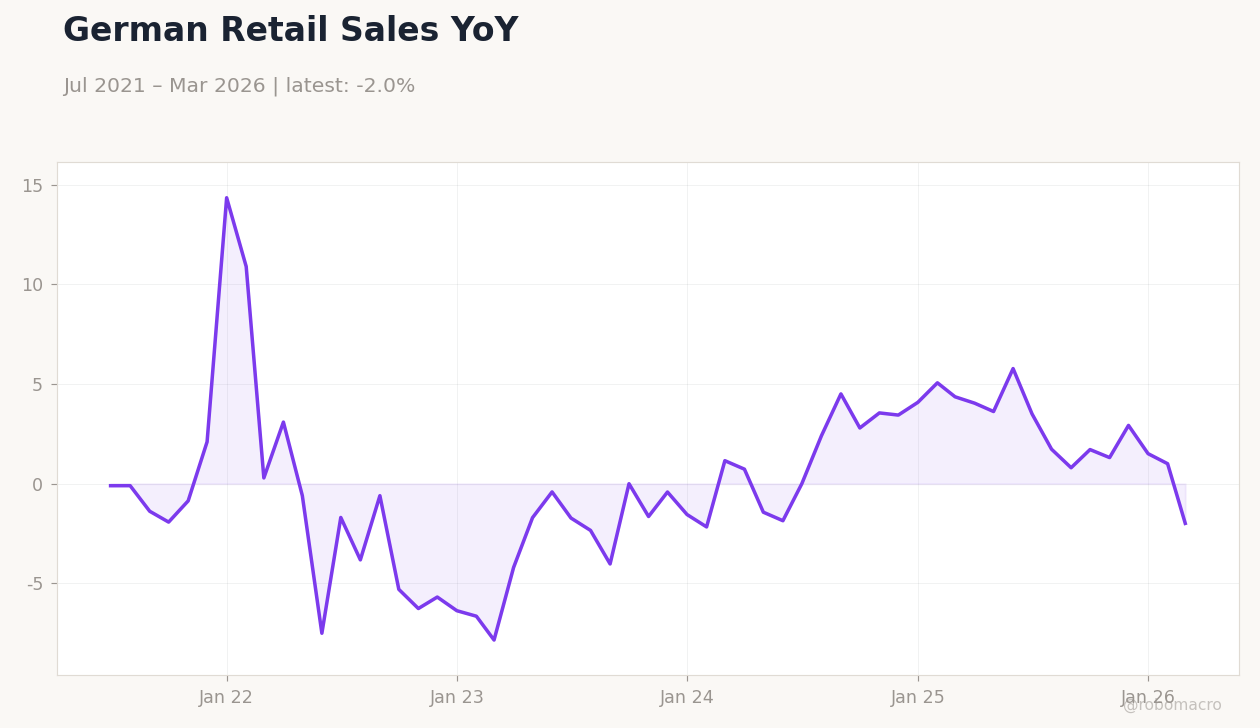

| Retail Sales Month-over-Month | -2 | -0.40 | 22:00 |

| Retail Sales Year-over-Year | -2 | - | 22:00 |

| S&P Global Manufacturing PMI Index | 51.70 | 52 | 23:15 |

| S&P Global Manufacturing PMI Index | 52.10 | 52 | 23:45 |

| Inflation Rate Year-over-Year Preliminary | 2.80 | - | 20:30 |

| Unemployment Level Change | -62,700 | - | 23:00 |

| S&P Global Services PMI | 47.90 | 48 | 23:15 |

| S&P Global Services PMI | 49.80 | - | 23:45 |

| Industrial Production Month-over-Month | 1 | -0.20 | 22:45 |

| Trade Balance | -6,900m | -6,500m | 22:45 |

- Bundesbank sees German Q2 stagnation amid Middle East risks

- French inflation accelerates while recession signals intensify

- Eurozone markets price ECB deposit rate steady at 2.00%

Yesterday's Recap

Equity indices closed mixed with Euro Stoxx 50 at 6,050.54, down 0.08 percent, while DAX edged 0.05 percent higher to 25,104.70 and CAC 40 slipped 0.07 percent. German 10-year Bund yields climbed 2.97 percent to 3.00 percent as investors digested fresh inflation concerns. Bundesbank warned Germany’s economy will likely stagnate in the second quarter given ongoing Middle East conflict spillovers.

French data releases showed sharper-than-expected contraction in exports and renewed price pressures, lifting the case for caution on growth. Italian and Spanish flash manufacturing PMIs printed near consensus levels without major surprises. EUR/USD held at 1.17 while EUR/GBP eased 0.11 percent.

No ECB speakers appeared and markets absorbed the absence of fresh policy signals.

The Day Ahead

Netherlands will release preliminary May inflation year-over-year, providing an early read on price trends outside the largest economies. Spain reports unemployment level change and final services PMI, both due after the close. Italy follows with its services PMI print, rounding out regional activity data.

French industrial production and trade balance figures arrive mid-week and will clarify whether the recent contraction broadens. Markets will watch for any deviation from consensus that could shift expectations around the 2.00 percent ECB deposit rate. No Governing Council members are scheduled to speak.

Other Economic Notes

EU finance ministers advanced a €45 billion joint defence-bond framework with limited immediate market reaction. French President Macron restated fiscal targets without announcing concrete measures. Broader Eurozone inflation prints from France, Italy and Spain remain elevated, sustaining debate over the timing of any policy adjustment.

Regional divergence persists as Germany faces stagnation risks while southern economies show mixed resilience.

Global Macro News

Brent crude rose 1.41 percent to $93.35 per barrel on supply concerns linked to Middle East tensions. Canada’s Ksi Lisims LNG project signed a 20-year supply agreement with Germany’s SEFE, bolstering European energy security. Japan will deploy troops to NATO’s Ukraine training mission based in Wiesbaden.

<i>↓ p.2</i>