Eurozone Macro Daily(Beta Mode)

German Retail Holds, Dutch Inflation Spikes

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Euro Stoxx 50 | 6,084.16 | -0.39% |

| DAX | 25,118.76 | +0.46% |

| CAC 40 | 8,186.21 | -0.28% |

| EUR/USD | 1.16 | -0.16% |

| EUR/GBP | 0.86 | -0.11% |

| EUR/JPY | 185.61 | -0.07% |

| Gold | 4,474.40 | -0.33% |

| Brent Crude | 98.47 | +2.57% |

| Bitcoin | 67,101.95 | +0.60% |

| German 2Y Bund | - | - |

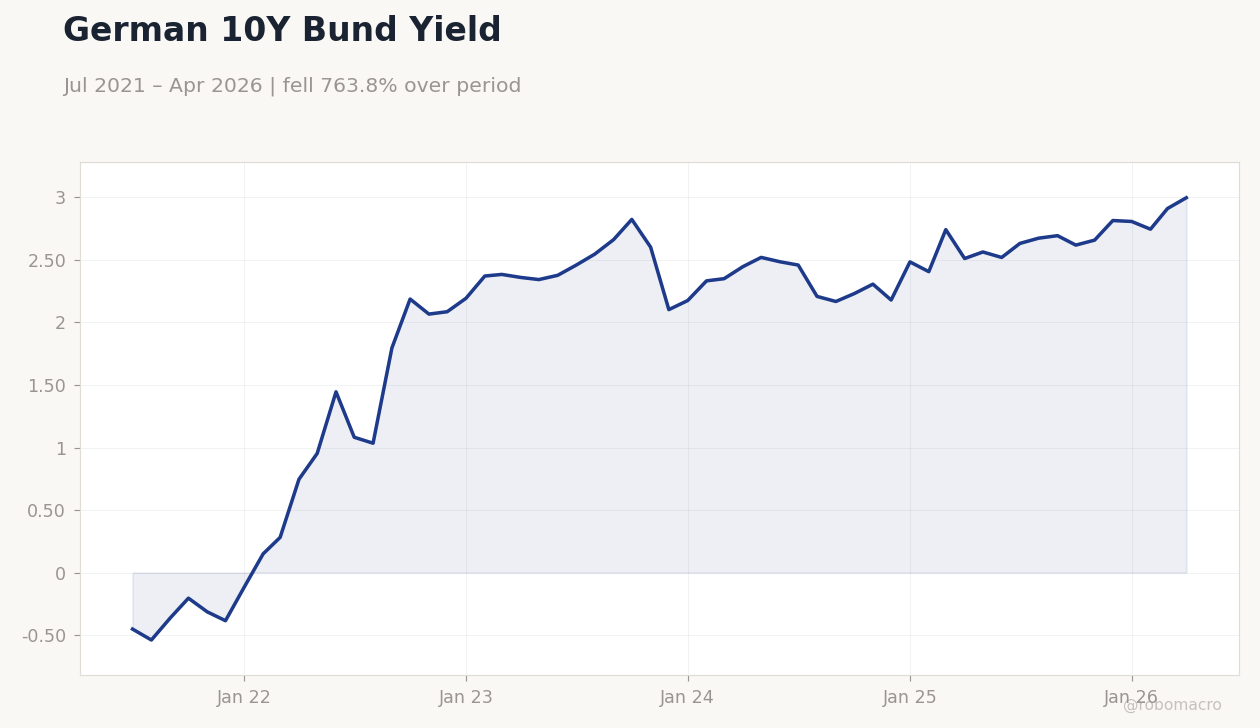

| German 10Y Bund | 3.00% | +2.97% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Retail Sales Month-over-Month | -0.30 | -0.40 | -0.30 |

| Retail Sales Year-over-Year | -0.20 | - | -0.30 |

| S&P Global Manufacturing PMI Index | 51.70 | 52 | 51.20 |

| S&P Global Manufacturing PMI Index | 52.10 | 52 | 52.90 |

| Inflation Rate Year-over-Year Preliminary | 2.80 | - | 3.50 |

| Unemployment Level Change | -62,700 | -56,800 | -36,300 |

German 10Y Bund Yield | Type: macro_line | Yield %: 2.996 (2026-04-01) | Range: -0.5386–2.996 | Trend(6pt): -0.4514,1.795,2.601,2.484,2.91,2.996

German 10Y Bund Yield | Type: macro_line | Yield %: 2.996 (2026-04-01) | Range: -0.5386–2.996 | Trend(6pt): -0.4514,1.795,2.601,2.484,2.91,2.996

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| S&P Global Services PMI | 47.90 | 48 | 23:15 |

| S&P Global Services PMI | 49.80 | - | 23:45 |

| Industrial Production Month-over-Month | 1 | -0.20 | 22:45 |

| Trade Balance | -6,900m | -6,500m | 22:45 |

| Retail Sales Month-over-Month | 0.80 | 0.20 | 01:00 |

- German retail sales beat expectations while Spanish manufacturing PMI fell to 51.2.

- Italian manufacturing PMI rose to 52.9; Dutch headline inflation jumped to 3.5% y/y.

- Euro Stoxx 50 fell 0.39% as German 10-year Bund yields climbed 2.97% to 3.00%.

Yesterday's Recap

German retail sales rose 0.1 percentage point above consensus at -0.3% m/m, with the y/y print at -0.3%. Spanish S&P Global manufacturing PMI declined to 51.2 from 51.7, missing forecasts. Italian manufacturing PMI exceeded expectations, printing 52.9 versus 52.0 consensus.

Dutch inflation accelerated sharply to 3.5% y/y. Spanish unemployment declined by only 36,300, softer than the 56,800 expected drop. Markets reflected mixed sentiment: DAX gained 0.46% while Euro Stoxx 50 slipped 0.39%.

EUR/USD eased 0.16% to 1.16 amid the data flow and Brent crude rose 2.57% to 98.47. The ECB Deposit Rate remains at 2.00%. Eurozone unemployment stands at 6.70%.

OECD lowered its German growth forecast again, citing the Middle East conflict’s drag on consumption and investment. The warning aligns with softer Spanish PMI and mixed retail prints across the bloc. Broader euro-area activity continues to show divergence between Germany and Italy.

The Day Ahead

Spanish and Italian services PMI releases are due this evening and will set the tone for services momentum. French industrial production and trade balance figures follow tomorrow, with consensus pointing to a 0.2% m/m contraction in output. Italian retail sales are scheduled for early Thursday and markets will watch for any follow-through from the manufacturing beat.

No ECB speakers are listed. Focus remains on whether the recent inflation uptick broadens beyond the Netherlands. Fiscal discussions in Brussels on joint defence procurement have yet to influence Bund curves materially.

Other Economic Notes

OECD lowered its German growth forecast again, citing the Middle East conflict’s drag on consumption and investment. The warning aligns with softer Spanish PMI and mixed retail prints across the bloc. Broader euro-area activity continues to show divergence between Germany and Italy.

Fiscal discussions in Brussels on joint defence procurement have yet to influence Bund curves materially.